ECON1010 Lecture Notes - Financial Statement, Working Capital, Bank Reconciliation

Lecture 6 - Working Capital

Friday, 30 March 2018

12:00 PM

<<L06 Lecture Working Capital (2).pptx>>

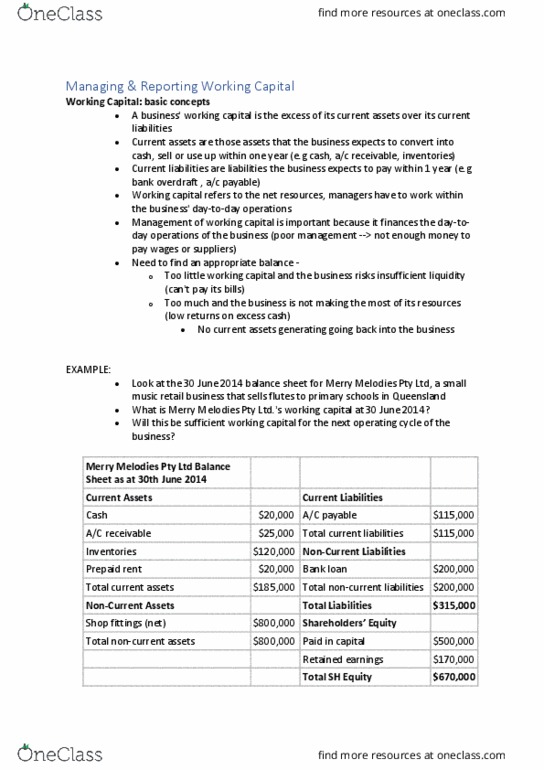

• A business' working capital is the excess of its current assets over its current liabilities

• Current assets are those that the business expects to turn into cash, sell or use up within one

year (e.g. cash, accounts receivable, inventories)

• Current liabilities are liabilities the business expects to pay within one year (e.g. bank

overdraft, accounts payable)

• Working capital refers to the net resources managers have to work with in the business' day-

to-day operations

• Management of working capital is important because it finances the day-to-day operations of

the business

• Need to find an appropriate balance:

o Too little working capital and the business risks insuffiient liquidity an’t pay its ills

o Too much and the business is not making the most of its resources (low returns on

excess cash)

• Example in recording and slide show about sufficiency of working capital

• Managers develop an internal control structure to ensure the operating activities are

performed in accordance with objectives

• Internal controls are the policies and procedures that direct how employees should perform a

business' activities

Internal controls for the most common working capital items:

• Cash

o This is money on hand, bank deposits in cheque and savings accounts, cheques, and

credit/debit card invoices receipts received from customers but not yet deposited

o A cheque is a written order directing a bank to pay out money to a designated payee

o The bank will take the money from a payers account and spend some days clearing the

cheque, if there are not sufficient funds the cheque is dishonoured

o Online banking

o Cash receipts must be properly recorded and protected from theft or loss

o All cash payments should require authorisation and be supported by appropriate source

documents

o All payments should be recorded and there should be 'cancelling' so payments are not

made twice

o A business' bank independently keep track of the cash balance and reports these in a

bank statement

o A business records cash transactions in its accounting system to keep track of its own

cash balance

o A bank reconciliation is comparing bank records with business records and identifying

any differences

o RECONCILIATION EXAMPLE IN RECORDING

o Cheques can be used for most transactions but can be inconvenient for small items

o A petty cash fund is a specified amount of money under the control of one employee

that is used for making small cash payments for the business

• Accounts receivable

o Potential credit customers complete a credit application and are subject to a credit

check

o Individual credit customer balances owed are monitored and followed up

o Total accounts receivable balance should be monitored in case adjustments are needed

• Inventory

find more resources at oneclass.com

find more resources at oneclass.com