FIN111 Lecture Notes - Lecture 5: Critical Thinking, Time Deposit, Compound Annual Growth Rate

Week 5 – The Time Value of Money

Time Value of Money

• How does a manager determine the value of a series of future cash flows, whether

paying for an asset or evaluating a project?

• What is the value of the stream of future cash flows today?

• We refer to this value as the time value of money (TVM)

Consuming Today or Tomorrow

• TVM is based on the belief that people prefer to consume goods today rather than

wait to consume similar goods tomorrow

- Positive time preference

• Money has a time value because a dollar today is worth more than a dollar

tomorrow

• Todays dollar a e iested to ear iterest or spet

Generalizations

• Value of a dollar invested (positive interest rate) grows over time

- The further in the future you receive a dollar, the less it is worth today

• Rate of interest determines trade-off between spending today versus saving

- The higher the interest rate the more likely you will invest funds

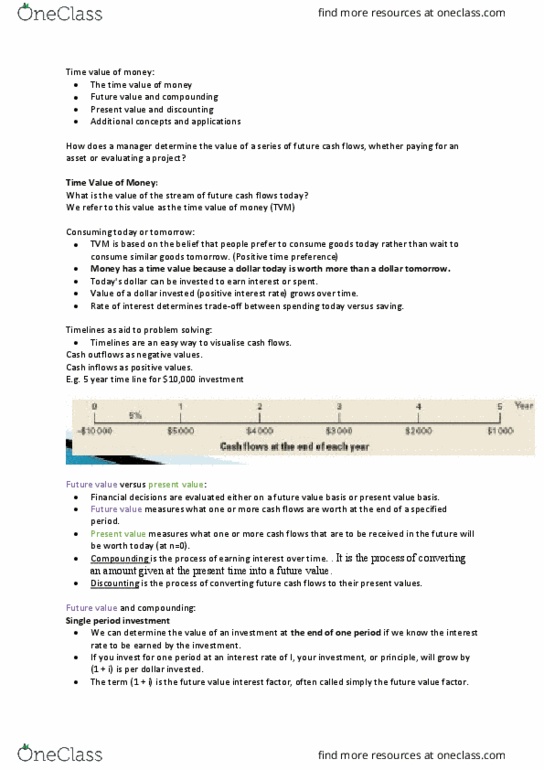

Timelines as Aids to Problem Solving

• Timelines are an easy way to visualize cash flows associated with investment

decisions → starts at 0 and shows the cash flows as they occur over time

- 0 is often the current point in time (today)

- Cash outflows as negative values

- Cash inflows as positive values

Future Value vs Present Value

• Financial decisions are evaluated either on a future value basis or present value basis

• Future value measures what one or more cash flows are worth at the end of a

specified period.

• Present value measures what one or more cash flows that are to be received in the

future will be worth today (at n=0).

• Discounting is the process of converting future cash flows to their present values

Definitions

• Principal amount is the amount invested

• Simple interest → amount of interest paid on the original principal amount.

• Interest on interest → interest earned on the reinvestment of previous interest

payments

• Compounding → process of earning interest over time.

• Compound interest → both simple interest and interest on interest

find more resources at oneclass.com

find more resources at oneclass.com

Future Value and Compounding

• The future value of an investment is what the investment will be worth after earning

interest for one or more time periods

• Compounding → converting the initial amount into future values

Single Period Investment

• We can determine the value of an investment at the end of one period if we know

the interest rate to be earned by the investment

• If you invest for one period at an interest rate of i, your investment, or principle, will

grow by (1 + i) per dollar invested

• The term (1+ i) is the future value interest factor, often called simply the future value

interest factor

Two-period Investment

• A two-period investment is simply two single-period investments back-to-back

• After the first period, interest accrues on original investment (principle) and interest

earned in preceding periods

• The principle is the amount of money on which interest is paid

• Simple interest is the amount of interest paid on the original principle amount only

• Compounding interest consists of both simple interest and interest-on-interest

Example:

If you put $100 in a bank savings account that pays interest at 10% a year. How much money will you have in one

year?

FV = Principal + Interest earned

= $100(1 + 0.10)

= $110

Example:

Suppose you want to put your new amount of $110 back in the bank for another year at 10% interest.

How much money will you have at the end of the second year (FV2)?

- Multiply the new principal amount by the future value factor (1 + i)

FV2 = FV1 x (1 + i)

= 100(1 + 0.10)2 * the power of 2 means 2 years

= $121

find more resources at oneclass.com

find more resources at oneclass.com

The Future Value Equation

• General equation to find the future value after any number of periods

• The term (1 + i)n is the future value factor.

FVn = PV x (1 + i)n

where:

• FVn = future value of investment at the end of period n

• PV = original principle (P0) or present value

• i = the rate of interest per period

• n = the number of periods

• (1 + i)n = the future value factor

What is the total compound interest?

Total compound interest = total simple interest + total interest on interest

• To find the total simple interest you find the simple interest for the first year then

multiply it for the amount of years

• To find the simple interest (SI):

SI = P0 x i

where:

• i = the simple interest for the period

• P0 = the initial principal amount

Example:

Suppose you decide to leave your $100 in the bank at 10% interest for 5 years. How much would you have at the

end of 5 years?

FV5 = $100(1 + 0.10)5

= $161.05

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Week 5 the time value of money. Consuming today or tomorrow: tvm is based on the belief that people prefer to consume goods today rather than wait to consume similar goods tomorrow. Positive time preference: money has a time value because a dollar today is worth more than a dollar tomorrow, today(cid:859)s dollar (cid:272)a(cid:374) (cid:271)e i(cid:374)(cid:448)ested to ear(cid:374) i(cid:374)terest or spe(cid:374)t. Generalizations: value of a dollar invested (positive interest rate) grows over time. The further in the future you receive a dollar, the less it is worth today: rate of interest determines trade-off between spending today versus saving. The higher the interest rate the more likely you will invest funds. Timelines as aids to problem solving: timelines are an easy way to visualize cash flows associated with investment decisions starts at 0 and shows the cash flows as they occur over time. 0 is often the current point in time (today)