BUSS1040 Lecture 2: Lecture 2 (ch7&8) - Firm behaviour (production, costs and supply)

8 Oct 2018

School

Department

Course

Professor

Document Summary

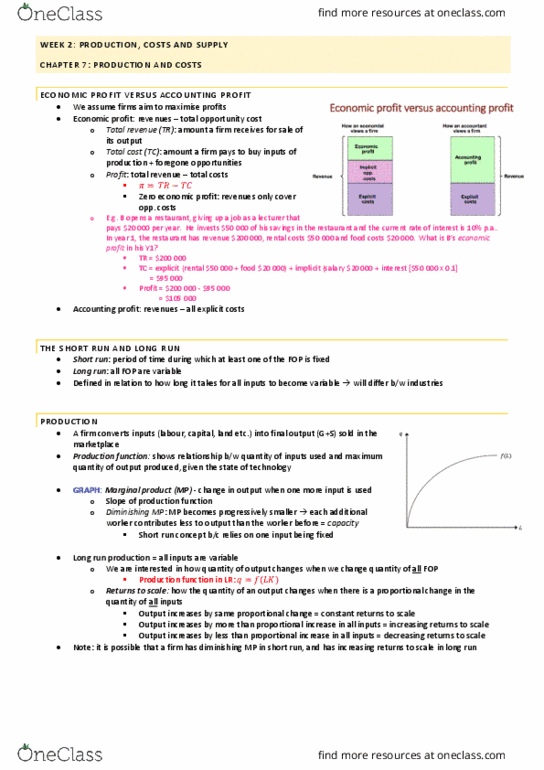

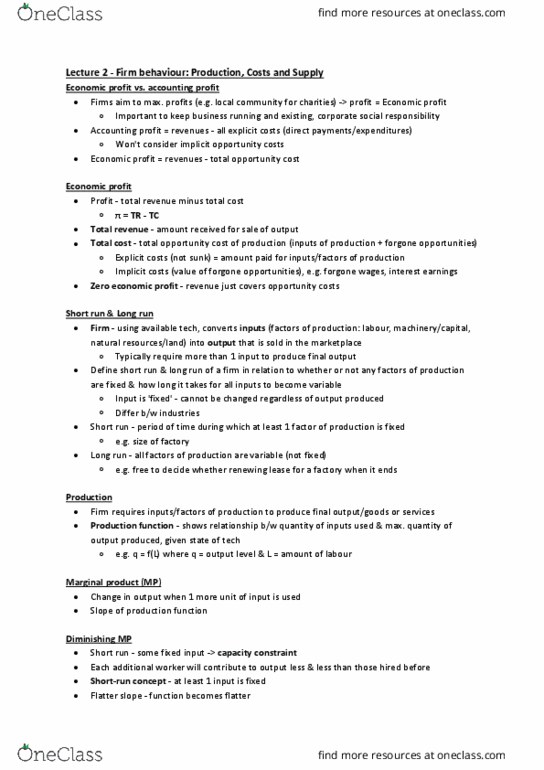

Lecture 2 (ch7&8) - firm behaviour (production, costs and supply) Tr (total revenue) = amount firm receives for the sale of its output. Tc (total cost) = the amount firm pays to buy the inputs of profit + oc. Zero economic profit = revenue just cover oc. Firm = uses inputs to create outputs sold in the marketplace. We define the short run and the long run of a firm in relation to whether or not any of the factors of production (inputs) are fixed. A(cid:374) i(cid:374)put is (cid:858)fi(cid:454)ed(cid:859) = if it (cid:272)a(cid:374)(cid:374)ot (cid:271)e (cid:272)ha(cid:374)ged (cid:396)ega(cid:396)dless of the output p(cid:396)odu(cid:272)ed. Short run = period of time during which at least one of the factors of production is fixed (size of a factory might not be able to changed) A firm requires inputs or factors of production (labour, capital, land, etc. ) in order to produce its final output (i. e. goods or services).