ACCT3321 Lecture Notes - Lecture 9: Income Statement, Revenue Recognition, Conceptual Framework

CHAPTER 15

Revenue

Scope of AASB 15

- The determination of when revenue is recognised

- An established principle about the nature, amount, timing and uncertainty of

revenue and cash flows arising from a contract that an entity shall apply to report

useful information to users of financial information

- Requires revenue to be recognised when an entity satisfies a performance obligation

by transferring promised goods or services to a customer

- An asset is transferred when the customer obtains control of that asset

- A change was released and reports must use this rule as at 1/1/18

Definition of income and revenue

- P 3 – 4

- Conceptual framework

oProfit is frequently used as a measure of performance or as the basis for

other measures, such as return on investment or earnings per share

-Income

oIncreases in economic benefits during the accounting period in the form of

inflows or enhancements of assets or decreases of liabilities that result in an

increase in equity, other than those relating to contributions from equity

participants

-Revenue

oRevenue arises in the course of the ordinary activities of an entity and is

referred to by a variety of different names including sales, fees, interest,

dividends, royalties and rent

oGains represent income

-Ordinary activities and gross inflows

oOrdinary is interpreted as relating to their core business operations

oRevenue is a gross concept, whereas gains tend to be net

find more resources at oneclass.com

find more resources at oneclass.com

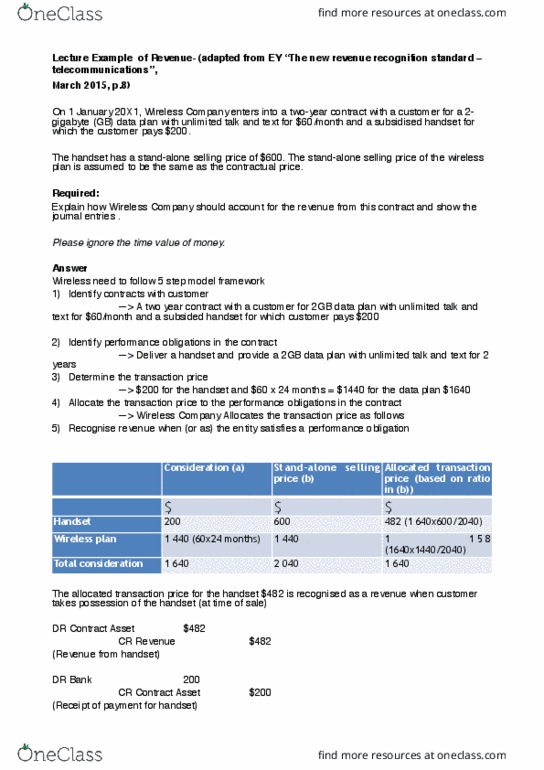

Steps in recognising revenue – in power point

1. Identify the contract or contracts with the customer

oOnly identify when the contract is approved… or transferred

oIdentify the payment terms

oRecognise the commercial substance

oThe expected consideration

2. Identify the performance obligations in the contract

oIs a promise to the customer to transfer either:

A distinct good or service

A series of distinct goods or services that are substantially the same

and that have the same pattern of transfer to the customer

oCriteria must be met:

The customer can benefit from the good or service on its own or in

conjunction with other readily available resources

The entity’s promise to transfer the good or service to the customer is

separately identifiable in the contract

oE.g. p 6

3. Determine the transaction price

oThe amount of consideration to which the entity expects to be entitled in

exchange for transferring promised goods or services to a customer,

excluding amounts collected on behalf of third parties [e.g. GST]

oVariable consideration

May include fixed or variable payments or both

When variable arises, the entity estimates the transaction price by

using either the expected value or the most likely amount

Expected = the sum of probability-weighted amounts in a

range of possible consideration amounts

Most likely = the one most likely to be the outcome in the

contract

oDeferred consideration

An entity shall adjust the consideration amount for the effects of time

value of money

E.g. p 8

oExchange or swaps

E.g. p 9

4. Allocate the transaction price to the performance obligation

oNecessary because the revenue might be recognised at different times for

the various performance obligations

oThe transaction price to be allocated to the performance obligations in the

contract by reference to their relative stand-alone selling prices [the price at

which an entity would sell a promised good or service separately to a

customer]

Adjusted market assessment approach – an entity could evaluate the

market in which it sells goods or services and estimate the price that a

customer in that market would be willing to pay for those goods or

services

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

An established principle about the nature, amount, timing and uncertainty of revenue and cash flows arising from a contract that an entity shall apply to report useful information to users of financial information. Requires revenue to be recognised when an entity satisfies a performance obligation by transferring promised goods or services to a customer. An asset is transferred when the customer obtains control of that asset. A change was released and reports must use this rule as at 1/1/18. Conceptual framework: profit is frequently used as a measure of performance or as the basis for other measures, such as return on investment or earnings per share. Income: increases in economic benefits during the accounting period in the form of inflows or enhancements of assets or decreases of liabilities that result in an increase in equity, other than those relating to contributions from equity participants.