ACCT-256 Lecture Notes - Lecture 3: Accounting Information System, Financial Statement, Trial Balance

Document Summary

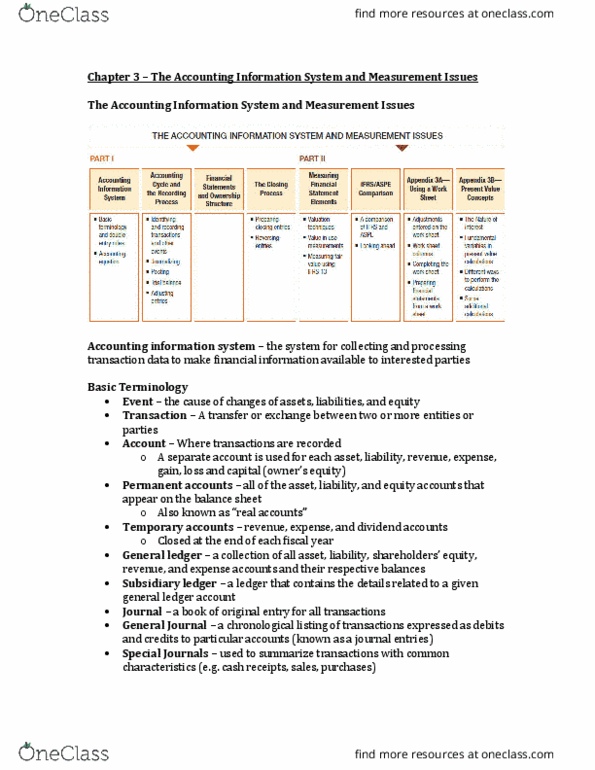

Chapter 3 the accounting information system: the accounting process can be described as a set of procedures used in identifying, recording, classifying, and interpreting transactions and other events relating to a business enterprise. In understanding the accounting process it is important for an individual to be aware of the basic terminology employed in the process. The basic terminology includes events, transactions, permanent accounts, temporary accounts, ledger, journal, posting, trial balance, adjusting entries, financial statements, closing entries, and reversing entries. These terms refer to the various activities that make up the accounting cycle. These individual terms are defined in the following review of the steps in the cycle. Once a transaction or other event has been identified as satisfying the criteria for recognition and measurement, it must be recorded in the accounts (step two). Double-entry accounting refers to the process used in recording.