MGCR 211 Lecture Notes - Lecture 16: Historical Cost, 7 World Trade Center, No Entry

9 Nov 2016

School

Department

Course

Professor

Document Summary

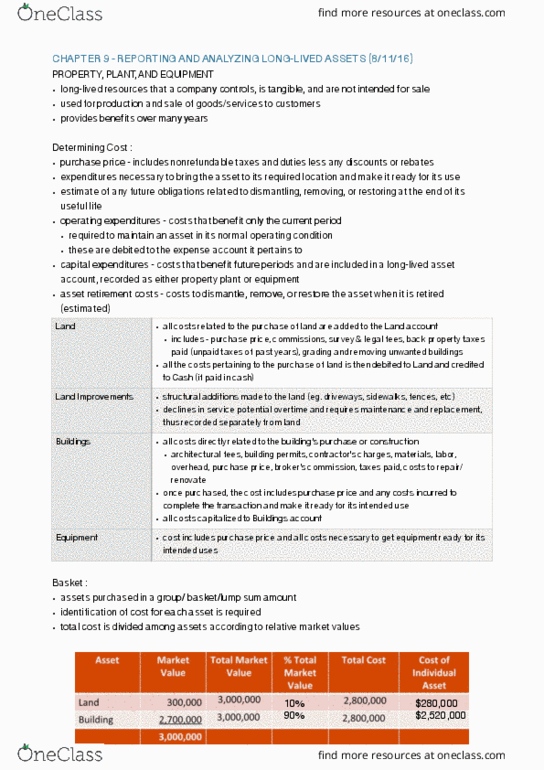

Used until replaced with a new asset: can have residual/resale value. Tangible: aka fixed, ppe, plant, capital- are long lived assets used in operations (land, buildings, equipment, machinery) Intangible: are rights or economic benefits not physical in nature (patents, trademarks, goodwill) The cost of any asset = the sum of all the costs incurred to bring the asset to its intended use. Recorded at cost, which includes: purchase price, including non-refundable taxes and duties, less discounts or rebates, expenditures necessary to bring asset to its intended location and make it ready for its intended use. Generally one time expense (ex: transportation, painting: estimated cost of future obligations to dismantle, remove or restore the asset at the end of its useful life. Note: annual recurring costs are generally not a part of the cost of pp&e. These items have their own accounts: annual license fee, annual insurance expense.