COMMERCE 2AB3 Lecture 21: W18_Comm 2AB3_Lecture Notes_Variance Analysis Part (I)

25 Apr 2018

School

Department

Course

Professor

Document Summary

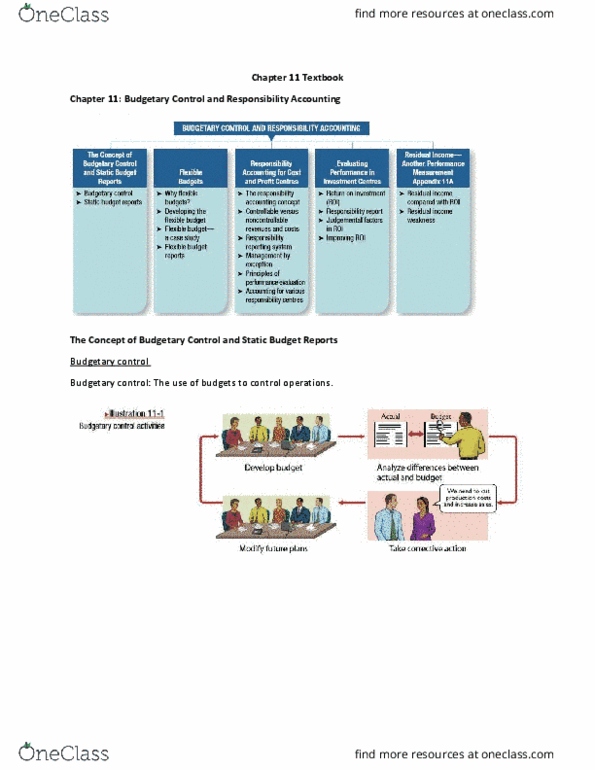

Budgetary control is a management control system that utilizes budgets which are developed based on standard costs to monitor and control costs in a given accounting period. Such control takes place by comparing the actual results with budgeted (planned) performance in order to identify deviations (variances) from the plan and take corrective actions, if needed. Budgetary control involves the following steps: developing standard costing system, developing budgets, analyzing the differences between actual and budgeted results, taking corrective action. Standard-costing system is a costing approach that assigns standard costs to production to help managers control costs and to evaluate the performance. The system has three components: standard costs (i. e. , predetermined costs), actual costs, and the difference between the two figures (termed a variance). Standard costs are carefully predetermined costs that a company should spend on each element of input factors (i. e. , dm, dl, and moh) to produce one unit of output. Thus, standard costs = (sq x sp).