COMMERCE 4AD3 Lecture Notes - Lecture 1: International Financial Reporting Standards, Financial Statement

24 Jan 2019

School

Department

Course

Professor

Chapter 1 – Intro to Auditing

The Essentials of Auditing, Public Practice, and Professional Responsibilities

• Auditing is the verification of information by someone other than the one

providing that information

o Audit financial statements – which summarize the entity’s transactions

and business events over a period

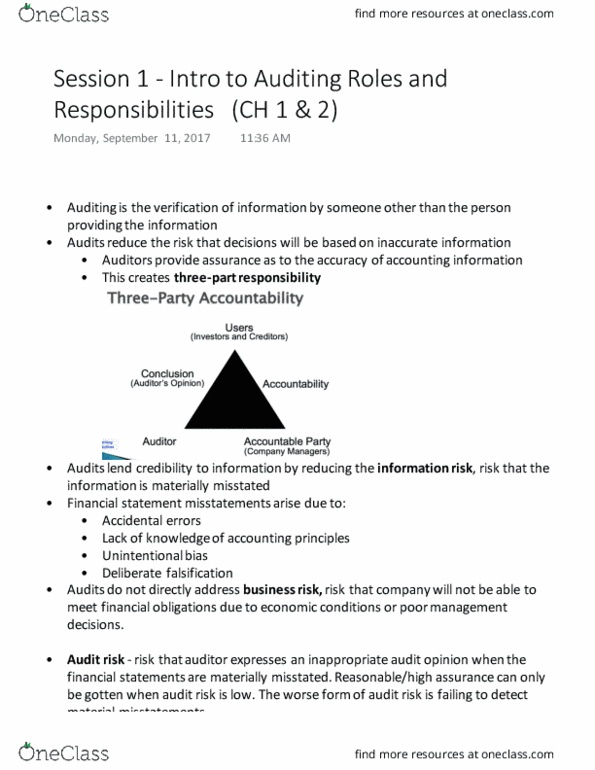

• Important because many economic activities are set up as three-party

accountability arrangements

o One party has to rely on the actions and information provided by another

party, who may not share same interests

• There is a risk, information risk, that financial statement information will not be

a full, true, and fair representation of the transactions and events that occurred

and hence will not be reliable for economic decision making

o Unreliable statements mean that they are so full of errors and omissions

that the information risk is sufficiently high to mislead users of the

statements – unethical reporting

o Risk can be reduced by having another party, independent auditor, verify

how well the information reflects the underlying realities of the entity’s

operations

• How does an independent auditor reduce information risk?

o Auditors expected to be competent in their area of specialty and put the

interests f public users of their services ahead of their own interests

o The profession issues standards for quality control in accounting firms,

education and qualification of members who will provide public

accounting services such as audits, and ethical conduct codes

o Auditor issue standards and guidelines for how to perform an

examination that will give the auditor reasonable assurance that financial

statements are fairly presented, and for how to communicate the

conclusions drawn to others

• Reasonable assurance describes a mental attitude that the auditor gains from the

conclusions drawn from audit examination findings

o Opinion on statements given in the Auditor’s Report

o This opinion provides a high level of assurance to the user that the

auditor believes that the information risk is low and has evidence to

support that belief

• Financial accountability information is not the same thing as auditing it

Introduction: The Concept of Auditing

• Auditing is critical to the proper functioning of capital markets and if audits are

perceived to fail, then capital markets can do the same

• Role of auditing is so critical that references can be made to audit societies

• Audit Societies – the term coined by Michael Power for societies in which there

is extensive examination by auditors of economic and other politically important

activities

o They are monitored to ensure market efficiency

o Auditors also monitor the effectiveness and efficiency of government