ECON 1B03 Lecture Notes - Lecture 12: Marginal Revenue, Demand Curve, Perfect Competition

31 Mar 2016

School

Department

Course

Professor

46

ECON 1B03 Full Course Notes

Verified Note

46 documents

Document Summary

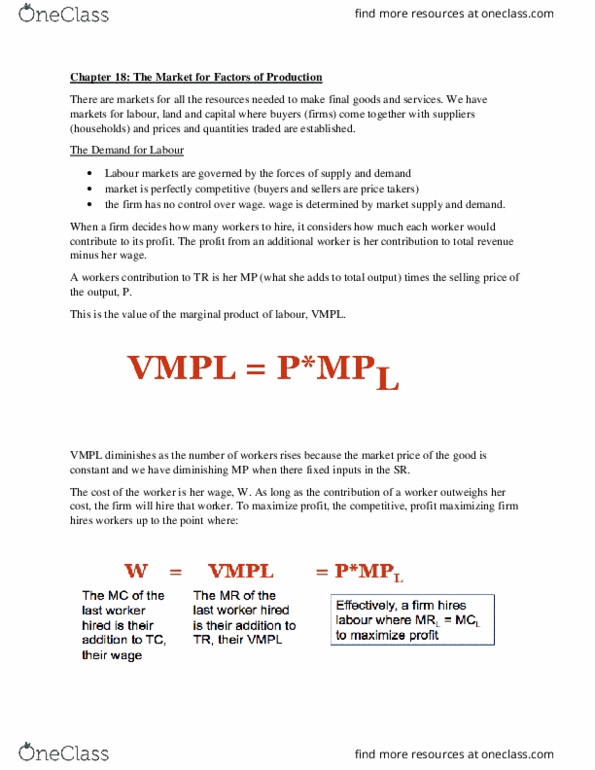

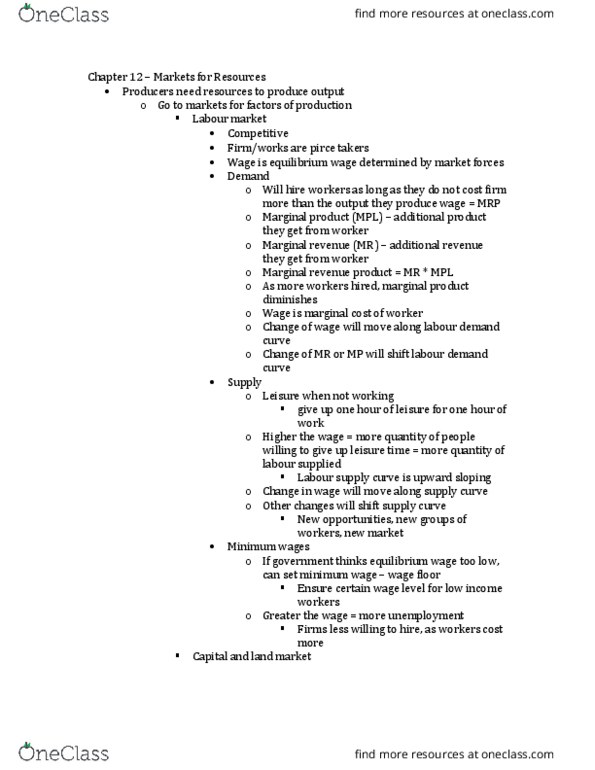

The markets for the factors of production (resources) If output is sold where p = mr, then mrp = p. If a worker adds 50 units to total output which sell for each, she adds to tr. Mrp diminishes because mp diminishes when there are fixed inputs. The cost of the worker is her wage, w. To maximize profit, firms hire workers where. A change in w: a movement along the labour demand curve. Since d = mrp = p * mp(l) if price increases, demand increases, shifts right if price decreases, demand decreases, shifts left: 2. Changes in supply of other factors (cid:1) (cid:1) (cid:1) if something changes the mp(l), the curve will shift. Advances that increase the mp(l), they"ll shift the demand curve to the right. We don"t mean advances meant to replace labour. The opportunity cost of leisure is an hours" wage.