COMM 319 Lecture Notes - Lecture 15: Property Income, Federal Charter Of 1291, Inter Vivos

20 Dec 2016

School

Department

Course

Professor

Document Summary

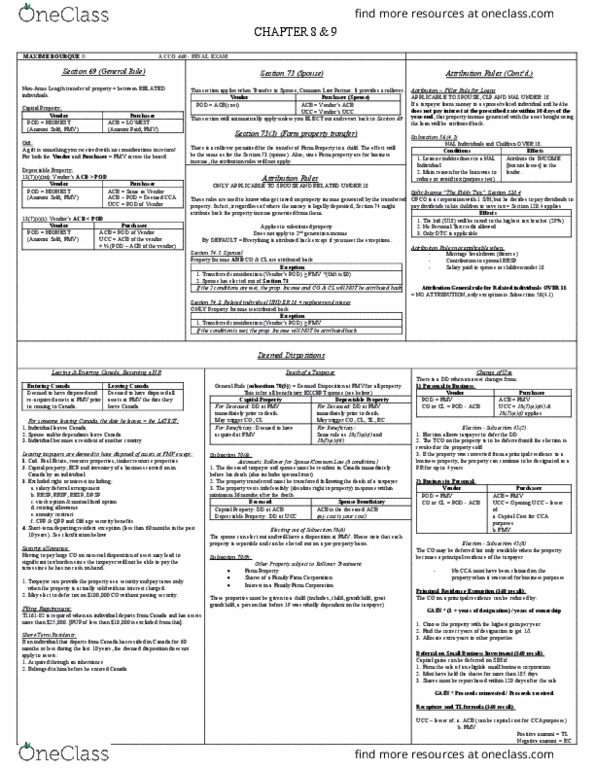

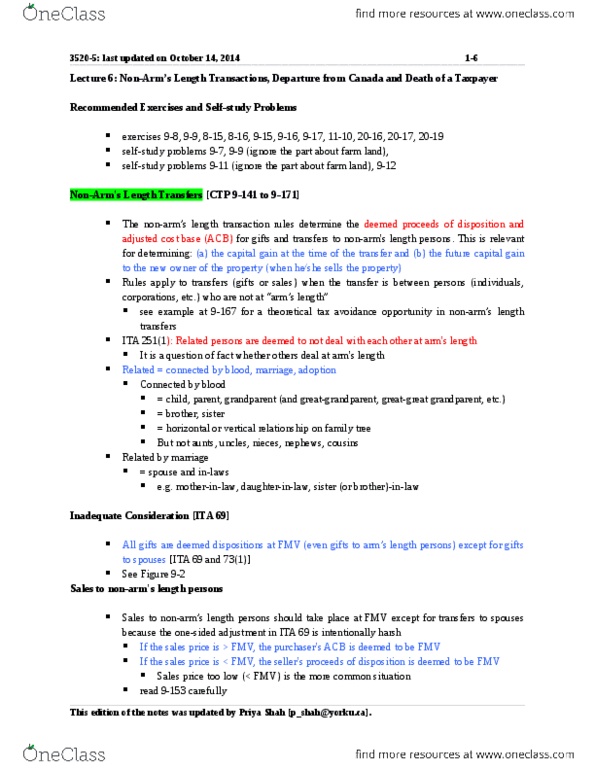

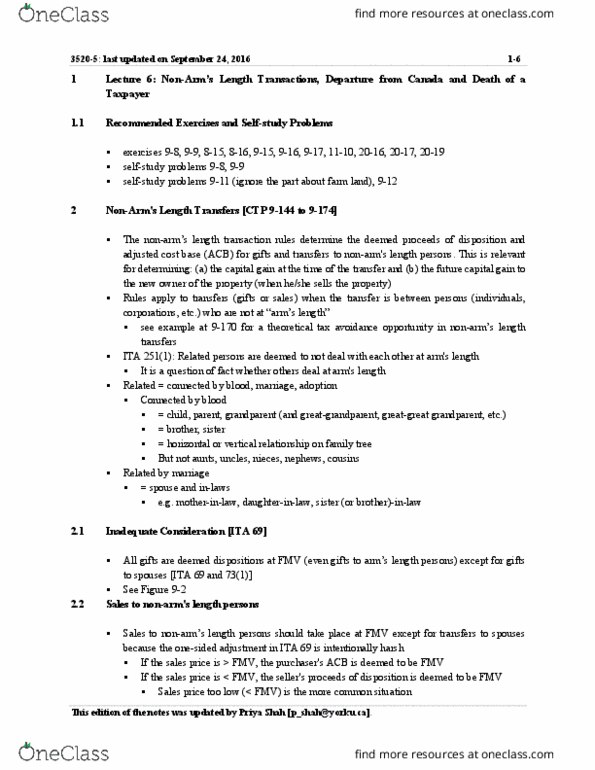

When an individual leaves canada he is deemed to have disposed of all his property at fmv 128. 1(4)(b: real property - building and land situated in canada, capital property used in a business in canada, including ecp. Exceptions to 128. 1(4)(b: rrsp"s, rpp"s, dpsp"s & rhosp"s. Inventory of a business carried on in canada. ********** 1 to 3 is taxed only when actually sold ************ S 69(1)(a): where a t/p acquires anything from a non-arm"s length person for more than fmv, he is deemed to have acquired it at fmv. S 69(1)(b): where a t/p has disposed of anything: 1) to a non-arm"s length person for pod < than fmv. 2) by way of gift, inter vivos to any person (arm"s length or not). The t/p will be deemed to have received pod = to fmv. The purchaser in situation 1) will have an acb = to the amount paid, and acb = to fmv in situation 2).