BUS 251 Lecture Notes - Lecture 2: Retained Earnings, Trial Balance, Accounts Payable

21 Feb 2017

School

Department

Course

Professor

Document Summary

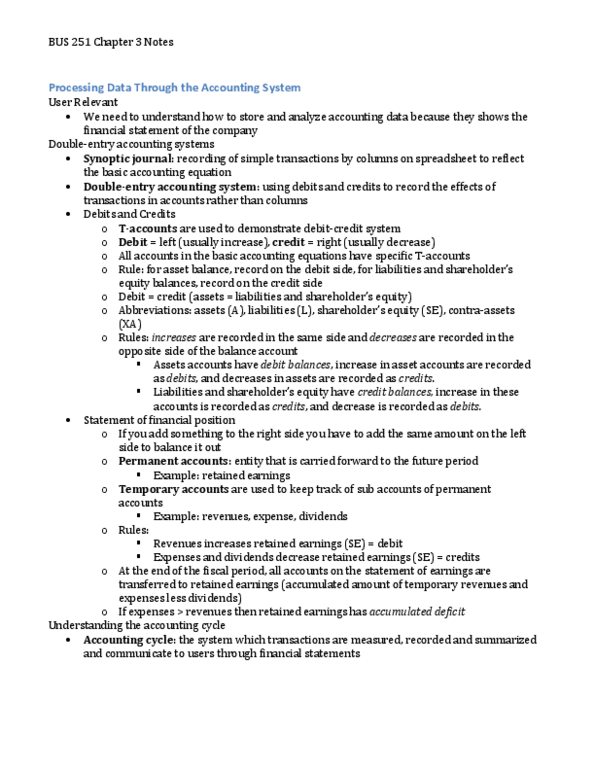

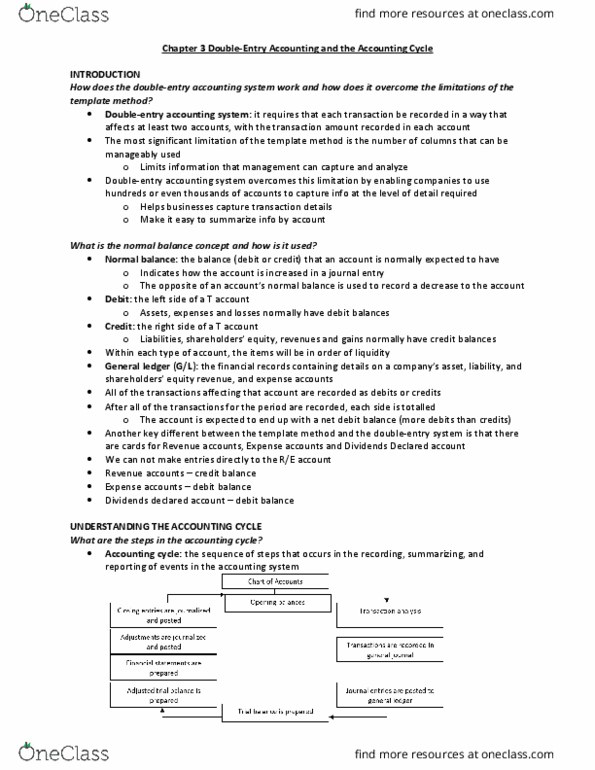

Double entry bookkeeping: replace the accounting equation with a t account. Every account (cash, accounts payable, loans, etc. ) will have its own t account. T accounts represent debits and credits on two columns and generates a balance at the end. Name of account on top of t table. When an asset increases, debit goes up (+) Assets will almost always have a debit balance, whereas liability/equity will almost always have a credit balance. Revenue (cr) vs. expenses/dividends (dr) follow the same rule as assets. Chart of accounts > opening balance > transactions or events > transaction analysis. Journal entries > posting to g/l > trial balance > adjusting balance > adjusted trial balance > preparation of financial statements > closing entries. Chart of accounts can be further categorized into permanent accounts or temporary accounts. Permanent accounts: statement of financial position accounts such as assets, liability and shareholder"s equity. Have balances that carry over from one period to the next (ex.