BUS 251 Lecture Notes - Lecture 5: Combined Gas And Steam, Current Asset, Gross Margin

5 Mar 2017

School

Department

Course

Professor

Document Summary

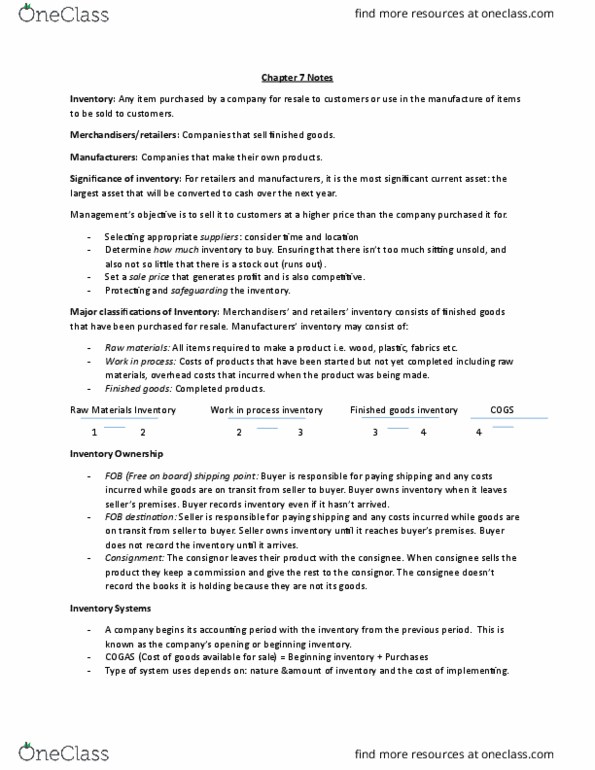

Periodic system: cogas ei = cogs (assumes that whatever good is not remaining in ending inventory is sold; cannot quantify theft) Purpose: allocating goods available for sale to either sold goods or unsold goods. Inventory = any item purchased by a company for resale to customer or use in manufacture of items to be sold. Merchandisers or retailers = companies that sell finished goods as inventory. Significance of inventory often the most significant current asset and the largest asset to be converted into cash within next year. Management"s objective = sell inventory at higher price than it was purchased. Determining necessary inventory levels and avoiding stock outs. Qualitative question: why would someone want to buy too much inventory? supplier has extra so get discount; supplier might run out; seasonal. Manufacturers" inventory = raw materials, work in process (wip), finished goods. Choosing periodic system: perpetual systems have high cost high benefit; periodic systems have low cost low benefit.