ECON 103 Lecture Notes - Lecture 9: Knitting Machine, Variable Cost, Sunk Costs

48 views12 pages

24 May 2017

School

Department

Course

Professor

Document Summary

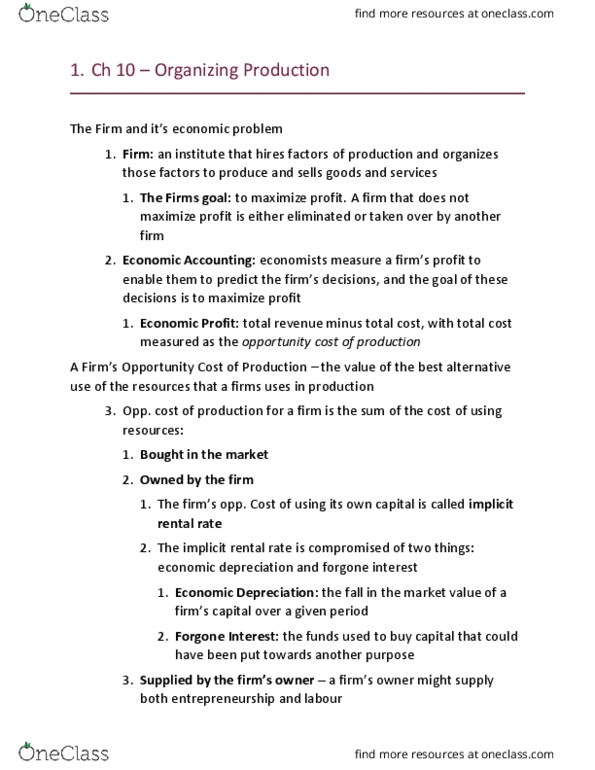

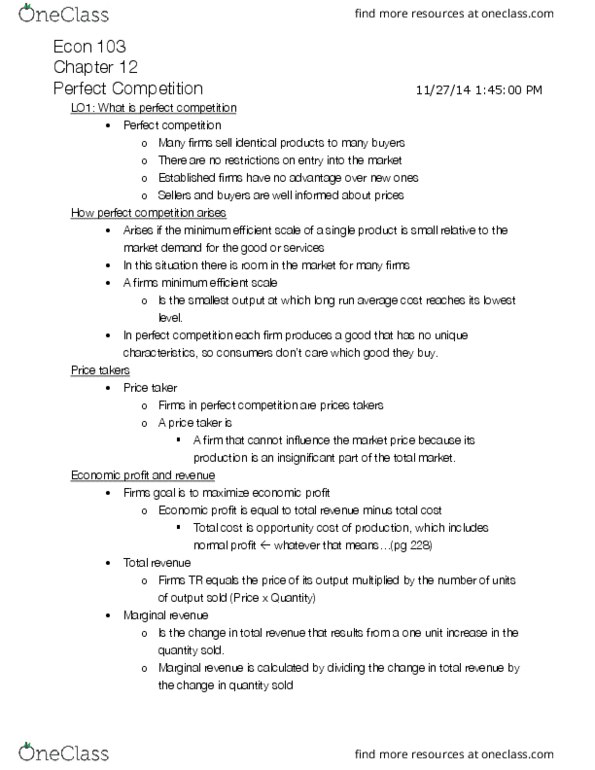

Firm can change its output in short run by changing the quantity of labor it employs. The long run: long run, a time frame in which the quantites of all factors of production can be varied. Is the maximum output that a given quantity of labor can produce: as more labor is employed, total product increases (not always more later) Each increase in employment increases the tp (total product: marginal product. Eg from 2 workers can make 10 sweaters, and 3 workers can make 13. The marginal product is 3: average product tells us how productive workers are on average, ap=tp/q, average product increases at first, and then decreases. Product curves: product curves are the relationship between employment and tp, mp and ap, shows how tp, ap and mp change and employment changes, shape of all product curves are similar due to two features. Increasing marginal returns initially: diminishing marginal returns eventually (both are below)

Get access

Grade+

$40 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

10 Verified Answers

Class+

$30 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

7 Verified Answers