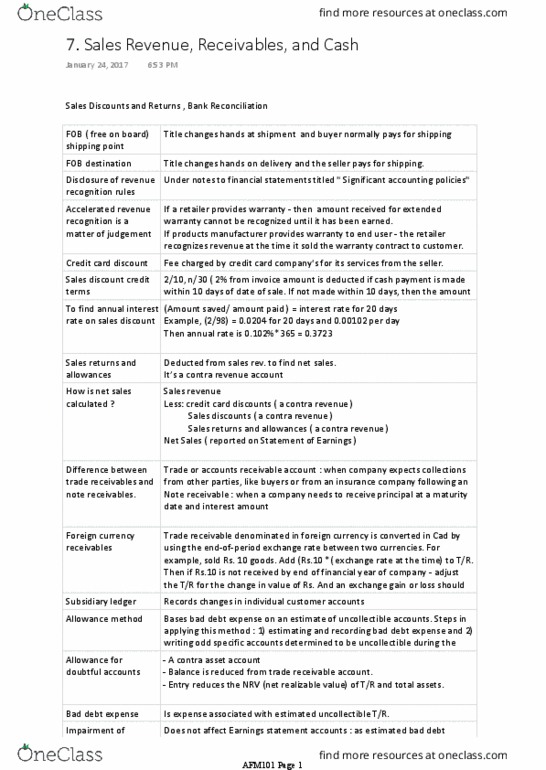

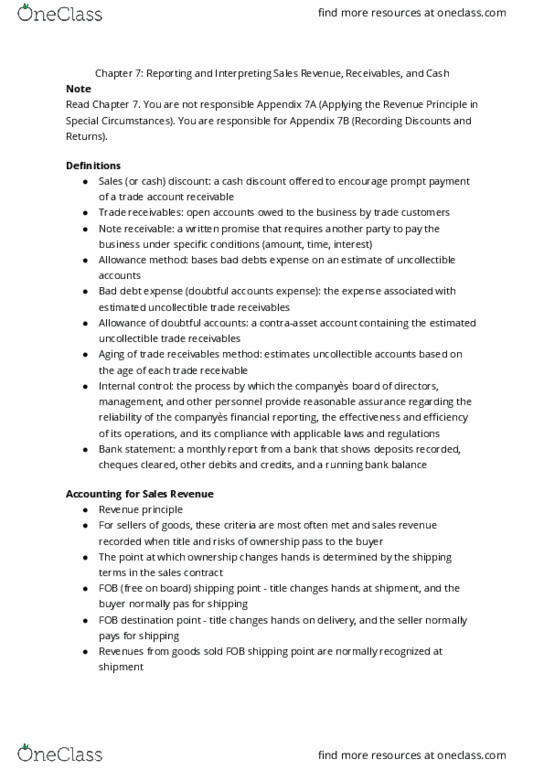

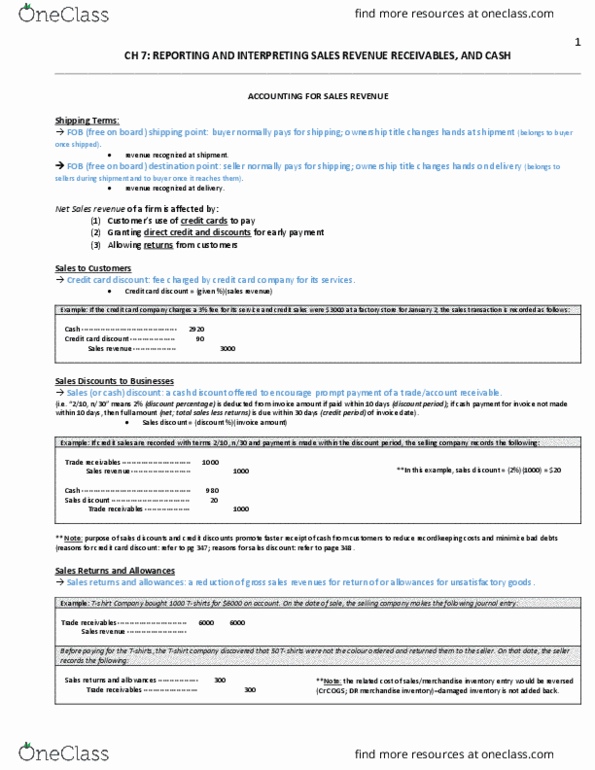

American Meter Company closes its books and prepares financial statements at the end of each month. American uses the perpetual inventory system. The company completed the following transactions during August, 2017:

Aug 1 Issued check no. 682 for August rent of $1,000

2. Issued check no. 683 to pay salaries of $1,240, which includes salary payable of $930 from July 31 (ignore payroll deductions).

2. Issued invoice no. 503 for sale on account to R. T. Loeb, $600. Americanâs cost of this merchandise was $190.

3. Purchased inventory on credit terms of 1/15, n/60 from Grant, Inc., $1,400

4. Received net amount of cash on account from Fullam Company, $2,156, within the discount period. The invoice, dated July 26 with terms of 2/10, net 30, was in the amount of $2,200.

4. Sold inventory for cash, $330 (cost, $104)

5. Received from Park-Hee, Inc. merchandise that had been sold earlier for $550 (cost, $174)

5. Issued check no. 684 to purchase supplies for cash, $780

6. Collected interest revenue of $1,100

7. Issued invoice no. 504 for sale on account to K. D. Skipper, $2,400 (cost, $759)

8. Issued check no. 685 to pay Federal Company $2,600 of the amount owed at July 31. This payment occurred after the discount period.

11. Issued check no. 686 to pay Grant, Inc. the net amount owed from August 3

12. Received cash from R. T. Loeb in full settlement of her account receivable from August 2

16. Issued check no. 687 to pay salary expense of $1,240

19. Received half the July 31 amount receivable from K. D. Skipperâafter the end of the discount period

19. Purchased inventory for cash $850, issuing check no. 688

22. Purchased furniture on credit terms of 3/15, n/60 from Beaver Corporation, $510

23. Sold inventory on account to Fullam Company, issuing invoice no. 505 for $9,966 (cost, $3,152)

25. Issued check no. 689 to pay utilities, $432

26. Purchased supplies on credit terms 2/10, n/30 from Federal Company, $180

30. Returned damaged inventory to company from whom American made the cash purchase on August 19, receiving cash of $850

30. Granted a sales allowance of $175 to K. D. Skipper

31. Purchased inventory on credit terms 1/10, n/30 from Suncrest Supply, $8,330

31. Issued check no. 690 to Lester Mednick, owner of the business, for personal withdrawal, $1,700

The chart of accounts with account balances as of July 31, 2017 are as follows:

General Ledger

101 Cash $ 8,650 401 Sales Revenue

102 Accounts Receivable 19,560 402 Sales Discounts

104 Interest Receivable 403 Sales Returns & Allowances

105 Merchandise Inventory 41,800 410 Interest Revenue

109 Supplies 2,150 501 Cost of Goods Sold

117 Prepaid Insurance 2,200 510 Salary Expense

140 Note Receivable, Long-Term 11,000 513 Rent Expense

160 Furniture 37,270 514 Depreciation Expense

161 Accumulated Depreciation 10,550 516 Insurance Expense

201 Accounts Payable 13,410 517 Utilities Expense

204 Salary Payable 930 519 Supplies Expense

207 Interest Payable 320 523 Interest Expense

220 Note Payable, Long-Term 42,000

301 Lester Mednick, Capital 55,420

302 Lester Mednick, Withdrawals

400 Income Summary

Accounts Receivable Subsidiary Ledger:

Fullam Company, $3,200

R T. Loeb, 0

Park-Hee Inc., 7,590

K.D. Skipper, 8,770

Accounts Payable Subsidiary Ledger:

Beaver Corporation $ 0

Federal Company 13,410

Grant, Inc, 0

Suncrest Supply 0

Prepare a Trial Balance in the Trial Balance Columns of a Worksheet (Trial Balance, Adjustments, Adjusted Trial Balance, Income Statement, and Balance Sheet headings).

Check figure: Trial Balance before any adjusting entries should total $142,516

The 2 questions before this was the following.

Journalize the August transactions in the general journal (page 9). Do not include the explanations. American makes all credit sales on terms of 2/10, n/30 unless otherwise indicated. I have posted the beginning balances to the general ledgers and subsidiary ledgers for you.

Post daily to the general ledger. Also post to the accounts receivable subsidiary ledger and the accounts payable subsidiary ledger when appropriate. On August 31 post to the general ledger.

I'm unsure if what I get form the previous answers will also help do this quesiton.