ADM 2341 Lecture Notes - Lecture 9: Budget, Accounts Receivable, Accounts Payable

Document Summary

Get access

Related Documents

Related Questions

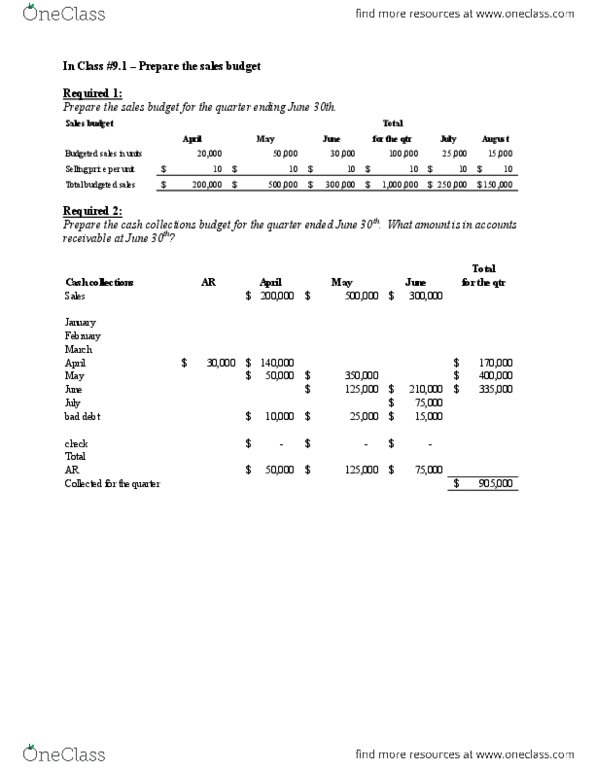

Crydon, Inc., manufactures an advanced swim fin for scubadivers. Management is now preparing detailed budgets for the thirdquarter, July through September, and has assembled the followinginformation to assist in preparing the budget: |

| a. | The Marketing Department hasestimated sales as follows for the remainder of the year (in pairsof swim fins): |

| The selling price of the swimfins is $15 per pair. |

| July | 5,200 | October | 3,200 |

| August | 6,200 | November | 2,200 |

| September | 4,200 | December | 2,200 |

| b. | All sales are on account. Basedon past experience, sales are expected to be collected in thefollowing pattern: |

| 44% | in the month ofsale |

| 47% | in the monthfollowing sale |

| 9% | uncollectible |

| The beginning accountsreceivable balance (excluding uncollectible amounts) on July 1 willbe $134,000. |

| c. | The company maintains finished goods inventories equal to 12% ofthe following monthâs sales. The inventory of finished goods onJuly 1 will be 624 pairs. |

| d. | Each pair of swim fins requires 5 pounds of geico compound. Toprevent shortages, the company would like the inventory of geicocompound on hand at the end of each month to be equal to 20% of thefollowing monthâs production needs. The inventory of geico compoundon hand on July 1 will be 5,320 pounds. |

| e. | Geico compound costs $3.00 per pound. Crydon pays for 59% of itspurchases in the month of purchase; the remainder is paid for inthe following month. The accounts payable balance for geicocompound purchases will be $11,100 on July 1. |

| Required: |

| 1a. | Prepare a sales budget, by month and in total, for the thirdquarter. July august september quarter budgeted sales(pair) Selling price per pair total budgeted sales |

| 1b. | Prepare a schedule of expected cash collections, by month and intotal, for the third quarter. |

Accounts receivable, beginning balance

July sales

August sales

September sales

Total cash collections

| 2. | Prepare a production budget for each of the months July throughOctober. July august september octomber budgeted sales (pairs) total needed required productions |

| 3a. | Prepare a direct materials budget for geico compound, by monthand in total, for the third quarter. (Do not roundintermediate calculations.) July august september quarter |

| required production pairs raw material needed per pair productions needs total needs raw material to be purchased cost of raw material to be pur |

| 3b. | Prepare a schedule of expected cash disbursements for geicocompound, by month and in total, for the third quarter. (Donot round intermediate calculations.) July ausust september quarter |

accounts payable, beginning balance

july purchases

august purchases

september purchases

total cash disburments

| Susquehanna Corp. is a manufacturer of earrings. You have been hired as a new management trainee of the company. In the past, the company has done very little in budgeting and at certain times of the year has experienced a shortage of cash. Since you are well trained in budgeting, you have decided to prepare a master budget for the upcoming year. You have gathered the beginning balance sheet and the necessary assumptions for you to create the budget. The company has an agreement with a bank that allows the company to borrow in increments of $10,000 at the beginning of each quarter. The interest is 2% per quarter and for simplicity we will assume that interest is not compounded. At the end of the quarter, the company will pay the bank all of the accumulated interest for the quarter on the loan and as much of the loan as possible (in increments of $10,000), while still retaining at least $40,000 in cash. Insurance for the whole year will be paid in January. Prepare the master budget for the year 2017. | |||||||||||||

| 0 | |||||||||||||

| Earrings Corp. | Earrings Corp. | ||||||||||||

| Balance Sheet | Budgeting Assumptions | ||||||||||||

| December 31, 2016 | |||||||||||||

| 2017 | 2018 | ||||||||||||

| Assets | Sales Budget Assumptions | Same for all quarters | Quarter 1 | Quarter 2 | Quarter 3 | Quarter 4 | Quarter 1 | Quarter 2 | |||||

| Current assets: | Budgeted sales in pairs of earrings | 105,000 | 50,000 | 60,000 | 100,000 | 135,000 | 65,000 | ||||||

| Cash | $ 48,000 | Selling price per pair | $ 23.50 | ||||||||||

| Accounts receivable | 224,000 | Percentage of sales collected in the quarter of sale | 60% | ||||||||||

| Raw materials inventory (240,000 grams of silver) | 120,000 | Percentage of sales collected in the quarter after sale | 40% | ||||||||||

| Finished goods inventory (48,000 pairs of earrings) | 480,000 | ||||||||||||

| Total current assets | $ 872,000 | Production Budget Assumptions | |||||||||||

| Plant and equipment: | Percentage of next quarter's sales needed in ending finished goods inventory | 40% | |||||||||||

| Land | 50,000 | ||||||||||||

| Buildings and equipment | 650,000 | Direct Materials Budget Assumptions | |||||||||||

| Accumulated depreciation | (330,000) | Grams of silver per pair of earring | 10 | ||||||||||

| Total Plant and equipment, net | 370,000 | Cost per gram of silver | $ 0.50 | ||||||||||

| Total assets | $ 1,242,000 | Percentage of next quarter's production needs in ending inventory | 20% | ||||||||||

| Percentage of purchases paid in the quarter of purchase | 55% | ||||||||||||

| Liabilities and Stockholders' Equity | Percentage of purchases paid in the quarter after purchase | 45% | |||||||||||

| Current liabilities: | |||||||||||||

| Accounts payable | $ 93,000 | Direct Labor Budget Assumptions | |||||||||||

| Stockholders' equity: | Direct labor-hours required per pair | 0.20 | |||||||||||

| Common stock | $ 700,000 | Direct labor cost per hour | $ 12.00 | ||||||||||

| Retained earnings | 449,000 | ||||||||||||

| Total stockholders' equity | 1,149,000 | Manufacturing Overhead Budget Assumptions | |||||||||||

| Total liabilities and stockholders' equity | $ 1,242,000 | Variable manufacturing overhead per direct labor-hour | $ 1.50 | ||||||||||

| Fixed manufacturing overhead excluding depreciation per quarter | $ 145,950 | ||||||||||||

| Depreciation on factory assets per quarter | $ 25,000 | $ 30,000 | $ 32,000 | $ 33,000 | |||||||||

| Selling and Administrative Expense Budget Assumptions | |||||||||||||

| Variable selling and administrative expense per pair | $ 2.80 | ||||||||||||

| Fixed selling and administrative expense: | |||||||||||||

| Advertising expense per quarter | $ 270,000 | ||||||||||||

| Executive salaries per quarter | $ 105,000 | ||||||||||||

| Insurance expense per quarter | $ 48,000 | (the whole year's insurance will be paid in January) | |||||||||||

| Rent expense per quarter | $ 240,000 | ||||||||||||

| Depreciation on non-factory assets per quarter | $ 14,000 | $ 16,000 | $ 17,000 | $ 18,000 | |||||||||

| Cash Budget Assumptions | |||||||||||||

| Minimum cash balance | $ 40,000 | ||||||||||||

| Equipment purchases | $ 20,000 | $ 40,000 | $ 15,000 | $ 10,000 | |||||||||

| Dividends per quarter | $ 15,000 | ||||||||||||

| Interest rate per quarter | 2% | ||||||||||||

| Loans can be made and repaid in increments of $10,000 | |||||||||||||

| Earrings Corp. | |||||||||||||

| Master Budget | |||||||||||||

| For the Year Ended December 31, 2017 | |||||||||||||

| Sales Budget | Quarter | ||||||||||||

| 1 | 2 | 3 | 4 | Year | |||||||||

| Budgeted unit sales (in pairs) | ? | ? | ? | ? | ? | ||||||||

| Selling price per unit | ? | ? | ? | ? | ? | ||||||||

| Total sales | ? | ? | ? | ? | ? | ||||||||

| Schedule of Expected Cash Collections | |||||||||||||

| Beginning accounts receivable | ? | ? | |||||||||||

| First quarter sales | ? | ? | ? | ||||||||||

| Second quarter sales | ? | ? | ? | ||||||||||

| Third quarter sales | ? | ? | ? | ||||||||||

| Fourth quarter sales | ? | ? | |||||||||||

| Total cash collections | ? | ? | ? | ? | ? | ||||||||

| Production Budget | Quarter | ||||||||||||

| 1 | 2 | 3 | 4 | Year | |||||||||

| Budgeted unit sales | ? | ? | ? | ? | ? | ||||||||

| Add: Desired units of ending finished goods inventory | ? | ? | ? | ? | ? | ||||||||

| Total needs | ? | ? | ? | ? | ? | ||||||||

| Less: Units of beginning finshed goods inventory | ? | ? | ? | ? | ? | ||||||||

| Required production in units | ? | ? | ? | ? | ? | ||||||||

| Direct Materials Budget | Quarter | ||||||||||||

| 1 | 2 | 3 | 4 | Year | |||||||||

| Required production in pairs | ? | ? | ? | ? | ? | ||||||||

| Units of raw materials needed per pair | ? | ? | ? | ? | ? | ||||||||

| Units of raw materials needed to meet production | ? | ? | ? | ? | ? | ||||||||

| Add desired units of ending raw materials inventory | ? | ? | ? | 214,000 | ? | ||||||||

| Total units of raw materials needed | ? | ? | ? | ? | ? | ||||||||

| Less units of beginning raw materials inventory | ? | ? | ? | ? | ? | ||||||||

| Units of raw materias to be purchased | ? | ? | ? | ? | ? | ||||||||

| Cost of raw materials per pound | ? | ? | ? | ? | ? | ||||||||

| Cost of raw materials to be purchased | ? | ? | ? | ? | ? | ||||||||

| Schedule of Expected Cash Disbursements for Purchases of Materials | |||||||||||||

| Beginning accounts payable | ? | ? | |||||||||||

| First quarter purchases | ? | ? | ? | ||||||||||

| Second quarter purchases | ? | ? | ? | ||||||||||

| Third quarter purchases | ? | ? | ? | ||||||||||

| Forth quarter purchases | ? | ? | |||||||||||

| Total cash disbursements for materials | ? | ? | ? | ? | ? | ||||||||

| Direct Labor Budget | Quarter | ||||||||||||

| 1 | 2 | 3 | 4 | Year | |||||||||

| Required production in pairs | ? | ? | ? | ? | ? | ||||||||

| Direct labor-hours per pair | ? | ? | ? | ? | ? | ||||||||

| Total direct labor-hours needed | ? | ? | ? | ? | ? | ||||||||

| Direct labor cost per hour | ? | ? | ? | ? | ? | ||||||||

| Total direct labor cost | ? | ? | ? | ? | ? | ||||||||

| Manufacturing Overhead Budget | Quarter | ||||||||||||

| 1 | 2 | 3 | 4 | Year | |||||||||

| Budgeted direct labor-hours | ? | ? | ? | ? | ? | ||||||||

| Variable manufacturing overhead rate | ? | ? | ? | ? | ? | ||||||||

| Variable manufacturing overhead | ? | ? | ? | ? | ? | ||||||||

| Fixed manufacturing overhead | ? | ? | ? | ? | ? | ||||||||

| Total manufacturing overhead | ? | ? | ? | ? | ? | ||||||||

| Less depreciation on factory assets | ? | ? | ? | ? | ? | ||||||||

| Cash disbursements for manufacturing overhead | ? | ? | ? | ? | ? | ||||||||

| Total manufacturing overhead | ? | ||||||||||||

| Budgeted direct labor-hours | ? | ||||||||||||

| Predetermined overhead rate for the year 2017 | ? | ||||||||||||

| Ending Finished Goods Inventory Budget (absorption costing basis) | |||||||||||||

| Item | Quantity | Cost | Total | ||||||||||

| Production cost per case: | |||||||||||||

| Direct materials | ? | grams | ? | per gram | ? | ||||||||

| Direct labor | ? | hours | ? | per hour | ? | ||||||||

| Manufacturing overhead | ? | hours | ? | per hour | ? | ||||||||

| Unit product cost | ? | ||||||||||||

| Budgeted finished goods inventory: | |||||||||||||

| Ending finished goods inventory in cases | ? | ||||||||||||

| Unit product cost | ? | ||||||||||||

| Ending finished goods inventory in dollars | ? | ||||||||||||

| Selling and Administrative Expense Budget | Quarter | ||||||||||||

| 1 | 2 | 3 | 4 | Year | |||||||||

| Budgeted unit sales | ? | ? | ? | ? | ? | ||||||||

| Variable selling and administrative expense per pair | ? | ? | ? | ? | ? | ||||||||

| Total variable selling and administrative expense | ? | ? | ? | ? | ? | ||||||||

| Fixed selling and administrative expense per quarter: | |||||||||||||

| Advertising | ? | ? | ? | ? | ? | ||||||||

| Executive salaries | ? | ? | ? | ? | ? | ||||||||

| Insurance | ? | ? | ? | ? | ? | ||||||||

| Rent | ? | ? | ? | ? | ? | ||||||||

| Depreciation on non-factory assets | ? | ? | ? | ? | ? | ||||||||

| Total fixed selling and administrative expense | ? | ? | ? | ? | ? | ||||||||

| Total selling and administrative expense | ? | ? | ? | ? | ? | ||||||||

| Adjustment for prepaid insurance | #VALUE! | #VALUE! | #VALUE! | #VALUE! | #VALUE! | ||||||||

| Less depreciation on non-factory assets | ? | ? | ? | ? | ? | ||||||||

| Cash disbursements for selling and administrative expense | ? | ? | ? | ? | ? | ||||||||

| Cash Budget | Quarter | ||||||||||||

| 1 | 2 | 3 | 4 | Year | |||||||||

| Beginning cash balance | ? | ? | ? | ? | ? | ||||||||

| Add cash receipts: | |||||||||||||

| Collections from customers | ? | ? | ? | ? | ? | ||||||||

| Total cash available | ? | ? | ? | ? | ? | ||||||||

| Less cash disbursements: | |||||||||||||

| Direct materials | ? | ? | ? | ? | ? | ||||||||

| Direct labor | ? | ? | ? | ? | ? | ||||||||

| Manufacturing overhead | ? | ? | ? | ? | ? | ||||||||

| Selling and administrative | ? | ? | ? | ? | ? | ||||||||

| Equipment purchases | ? | ? | ? | ? | ? | ||||||||

| Dividends | ? | ? | ? | ? | ? | ||||||||

| Total cash disbursements | ? | ? | ? | ? | ? | ||||||||

| Excess (deficiency) of cash available over disbursements | ? | ? | ? | ? | ? | ||||||||

| Financing: | |||||||||||||

| Borrowings (at the beginnings of quarters) | $ 50,000.00 | $ - | ? | ||||||||||

| Repayments (at end of the year) | $ - | ? | ? | ||||||||||

| Interest | $ (1,000.00) | ? | ? | ||||||||||

| Total financing | $ 49,000.00 | ? | ? | ? | ? | ||||||||

| Ending cash balance | ? | ? | ? | ? | ? | ||||||||

| [The following informationapplies to the questions displayed below.] |

Beech Corporation is a merchandising company that is preparing amaster budget for the third quarter of the calendar year. Thecompanyâs balance sheet as of June 30th is shown below: |

| Beech Corporation Balance Sheet June 30 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Assets | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash | $ 81,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accountsreceivable | 132,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Inventory | 56,250 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Plant and equipment,net of depreciation | 214,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total assets | $ 483,250 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Liabilities and Stockholdersâ Equity | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accountspayable | $ 75,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Common stock | 346,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Retainedearnings | 62,250 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total liabilitiesand stockholdersâ equity | $ 483,250 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| alue: Required information

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||