ADM 2341 Lecture Notes - Lecture 12: Sunk Costs, Variable Cost, Filigree

18 Dec 2015

School

Department

Course

Professor

Document Summary

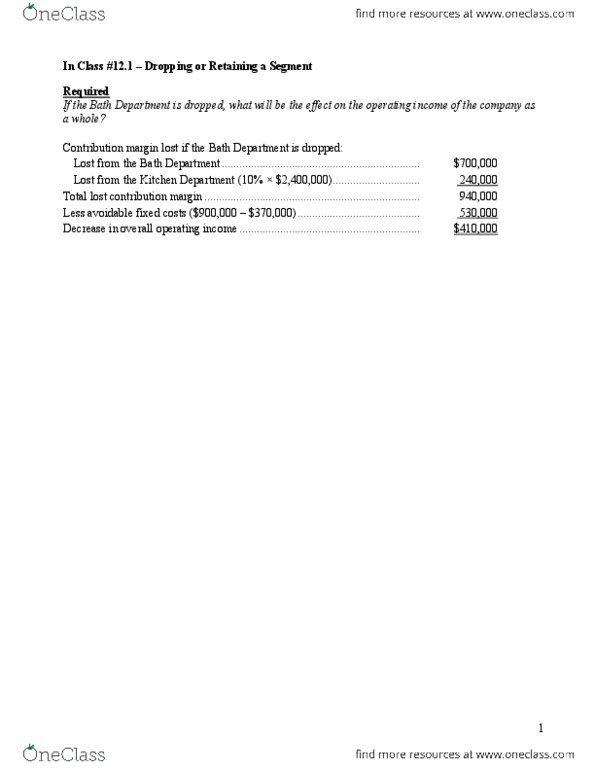

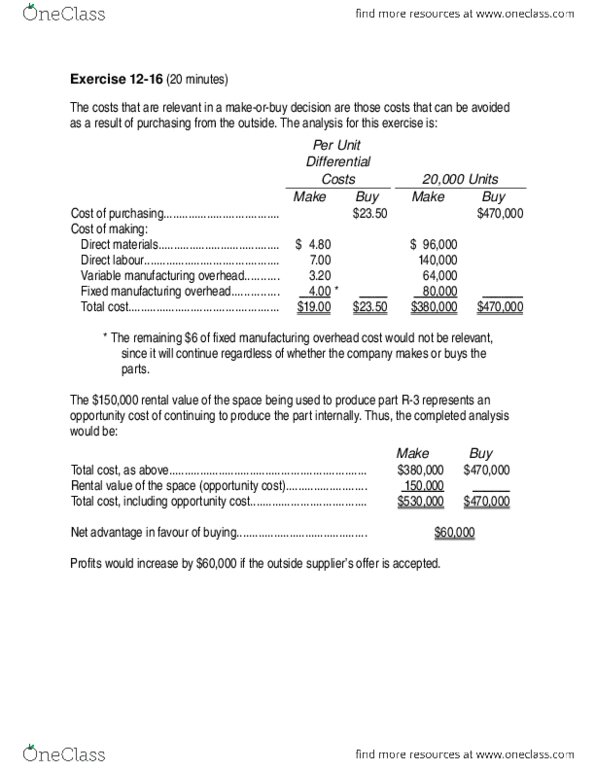

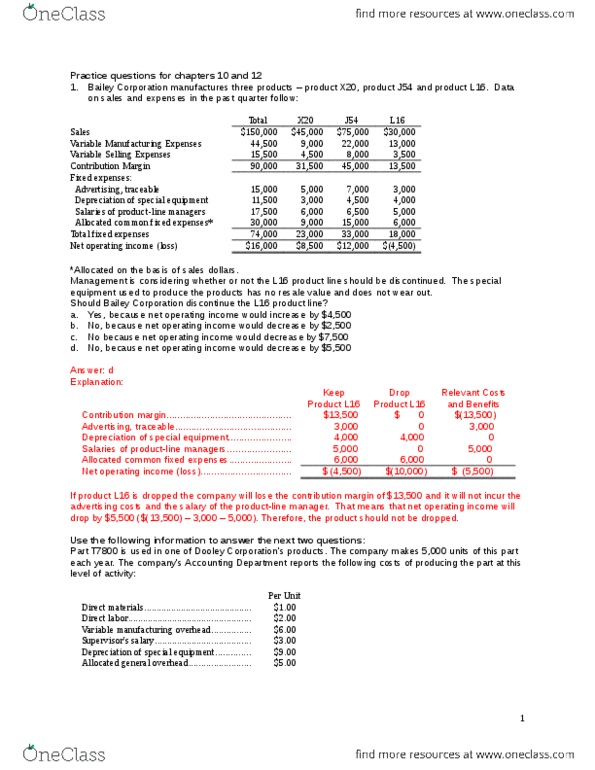

Difference in favour of continuing to make the parts 1only the supervisory salaries can be avoided if the switches are purchased. The remaining book value of the special equipment is a sunk cost; hence, the ( x 75%) per unit depreciation expense is not relevant to this decision. Based on these data, the company should reject the offer and should continue to produce the parts internally. Opportunity cost segment margin forgone on a potential new product line Difference in favour of purchasing from the outside supplier Thus, the company should accept the offer and purchase the parts from the outside supplier. Only the incremental costs and benefits are relevant. In particular, only the variable manufacturing overhead and the cost of the special tool are relevant overhead costs in this situation. The other manufacturing overhead costs are fixed and are not affected by the decision.