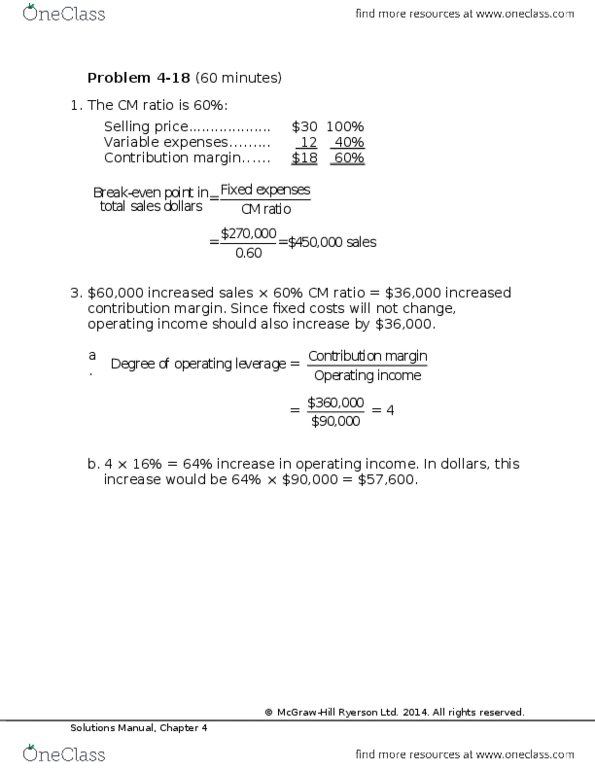

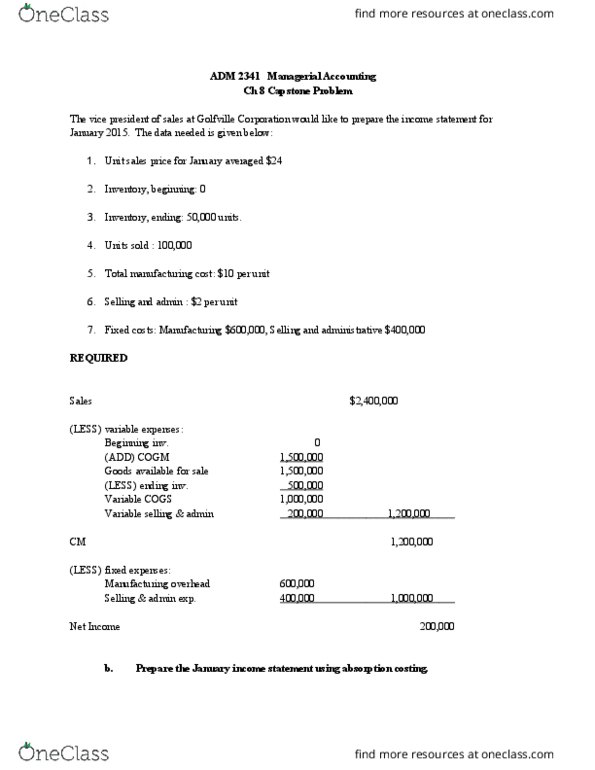

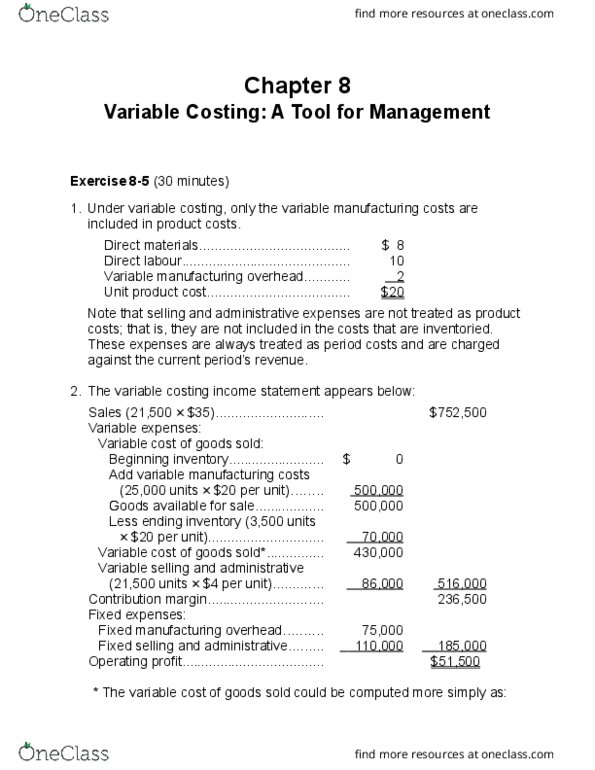

ADM 2341 Lecture Notes - Lecture 7: Earnings Before Interest And Taxes, Operating Leverage

Document Summary

Get access

Related Documents

Related Questions

| Basic information | |||

| Exhibit 1 Hallstead Jewelers | |||

| Income Statements for YearsEnded January 31 (thousands of dollars) | |||

| 2003 | 2004 | 2006 | |

| Sales | $9,000,000 | $8,000,000 | $11,000,000 |

| Cost of goods sold | 4,050,000 | 3,600,000 | 4,950,000 |

| Gross margin | $4,950,000 | $4,400,000 | $6,050,000 |

| Expenses | |||

| Selling expense | |||

| Salaries | 2,021,000 | 2,081,000 | 4,085,000 |

| Commissions | 450,000 | 400,000 | 550,000 |

| Advertising | 254,000 | 250,000 | 257,000 |

| Administrative expenses | 418,000 | 425,000 | 535,000 |

| Rent | 420,000 | 420,000 | 840,000 |

| Depreciation | 84,000 | 84,000 | 142,000 |

| Miscellaneous expenses | 53,000 | 93,000 | 122,000 |

| Total expenses | $3,700,000 | $3,753,000 | $6,531,000 |

| Net income | $1,250,000 | $647,000 | $(481,000) |

| Exhibit 2 Hallstead JewelersOperating Statistics | |||

| 2003 | 2004 | 2006 | |

| Sales space (square feet) | 10,000 | 10,000 | 15,000 |

| Sales per square foot | $900 | $800 | $733 |

| Sales tickets | 5,000 | 5,000 | 7,000 |

| Average sales ticket | $1,800 | $1,600 | $1,571 |

Assumptions:

Sales price per ticket = $1,572

Variable cost per unit = $786 (cost of goods sold of $707 +Sales commissions of $79)

Complete the table below:

Alternative #1 | Per unit | Total | Per unit | Total |

# of sales tickets | 7000 | |||

Selling price per ticket | $1,572 | $11,000,000 | ||

Variable cost per ticket | $786 | $5,500,000 | ||

Contribution margin per ticket | $786 | $5,500,000 | ||

Total fixed costs | 5,981,000 | |||

Net income | $(481,000) | |||

Change in net income if accept alternative | ||||

Breakeven point in units | 7,610 | |||

Review of Question #4 requirements. Increase advertisingby $20,000, increase sales revenue (volume) by 2%.

For each question, answer yes or no for each piece ofinformation listed.

Information | For this alternative only, is there a change in this item thataffects calculation of net income? Yes or No | For this alternative only, is there a change in this item thateffects the calculation of the new breakeven point? Yes or No |

Selling price per unit | ||

Variable cost per unit | ||

Total fixed costs | ||

Net income | ||

Sales volume |

Complete the table below:

Alternative #3 | Per unit | Total | Per unit | Total |

# of sales tickets | 7000 | |||

Selling price per ticket | $1,572 | $11,000,000 | ||

Variable cost per ticket | $786 | $5,500,000 | ||

Contribution margin per ticket | $786 | $5,500,000 | ||

Total fixed costs | 5,981,000 | |||

Net income | $(481,000) | |||

Change in net income if accept alternative | ||||

Breakeven point in units | 7,610 | |||

Alternatives | Change in Net Income | New Breakeven point in units | Change in Breakeven point in units |

#1 Decrease SP, Increase sales volume | |||

#2 Eliminate sales commissions | Increases by $550,000 | 6,914 | Decreases by 696 |

#3 increase Fixed costs by $20,000 to get increase of 2% salesrevenue (volume) |

Phoenix Companyâs 2017 master budget included the following fixed budget report. It is based on an expected production and sales volume of 15,000 units.

| PHOENIX COMPANY Fixed Budget Report For Year Ended December 31, 2017 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Sales | $ | 3,150,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cost of goods sold | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Direct materials | $ | 945,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Direct labor | 225,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Machinery repairs (variable cost) | 45,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| DepreciationâPlant equipment (straight-line) | 300,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Utilities ($45,000 is variable) | 195,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Plant management salaries | 200,000 | 1,910,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Gross profit | 1,240,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Selling expenses | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Packaging | 90,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shipping | 105,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Sales salary (fixed annual amount) | 235,000 | 430,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| General and administrative expenses | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Advertising expense | 125,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Salaries | 230,000 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Entertainment expense | 85,000 | 440,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Income from operations | $ | 370,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

The companyâs business conditions are improving. One possible result is a sales volume of 18,000 units. The company president is confident that this volume is within the relevant range of existing capacity. How much would operating income increase over the 2017 budgeted amount of $370,000 if this level is reached without increasing capacity?

| |||||||||||||||||||||||||||||||||||

An unfavorable change in business is remotely possible; in this case, production and sales volume for 2017 could fall to 12,000 units. How much income (or loss) from operations would occur if sales volume falls to this level? (Enter any loss with minus sign.)

| |||||||||||||||||||||||||

1. Robbieâs Ribs has the following sales and costinformation:

Average number of pounds sold per year - 39,750

Average selling price per pound of ribs - $11.50

Variable expenses per pound:

Raw material - $3.70

Variable labor and overhead - $3.20

Annual fixed costs:

Production expenses - $37,300

Selling & Administrative expenses $15,186

The companyâs tax rate is 30%. The companyâs costs have slowlybeen rising and profits rapidly falling. Robbie Shaw, companypresident, has asked your help in answering the followingquestions:

What is the contribution margin per pound of ribs? Thecontribution margin ratio?

What is the break-even point in pounds of ribs? In dollars?

How much revenue must be generated to produce $39,749 of pretaxincome? How many pounds of ribs would this level of revenuerepresent?

How much revenue must be generated to produce $24,500 after-taxincome? How many pounds of ribs would this represent?

2. The following is financial information relative to twocompanies in the same industry:

| Category | Alpha | Omega |

|---|---|---|

| Sales | $10,000,000 | $10,000,000 |

| Variable Cost | 5,000,000 | 2,000,000 |

| Contribution Margin | 5,000,000 | 8,000,000 |

| Fixed Costs | 3,000,000 | 6,000,000 |

| Operating Income | $2,000,000 | $2,000,000 |

Calculate the operating leverage for each firm.

If sales increased 10% for each firm, the variable cost per unitdid not change, and the fixed costs did not change, what would bethe change in operating income?

If sales decreased 20% for each firm, the variable cost per unitdid not change, and the fixed costs did not change, what would bethe change in operating income?

Discuss the nuances of operating leverage and its relation torisk.

3. WaterSports USA sells three types of wake boards. Informationrelative to sales in units and dollars are given in the tablebelow:

| Sales Category | Wakeman | Jumper | Novice | Total |

|---|---|---|---|---|

| Sales in Units | 1,000 | 5,000 | 2,000 | 8,000 |

| Price per Unit | $200 | $150 | $100 | |

| Variable cost per Unit | $150 | $100 | $50 |

Fixed costs are projected to be $100,000. Carry all calculationsto four decimal places.

Compute the contribution margin per unit.

Compute the weighted contribution margin.

Compute the break-even in total units.

Compute the break-even per product.

Discuss briefly the usefulness of the computation in thebusiness world.