RSM222H1 Lecture Notes - Lecture 9: Total Absorption Costing, Continual Improvement Process

2 Apr 2017

School

Department

Course

Professor

Document Summary

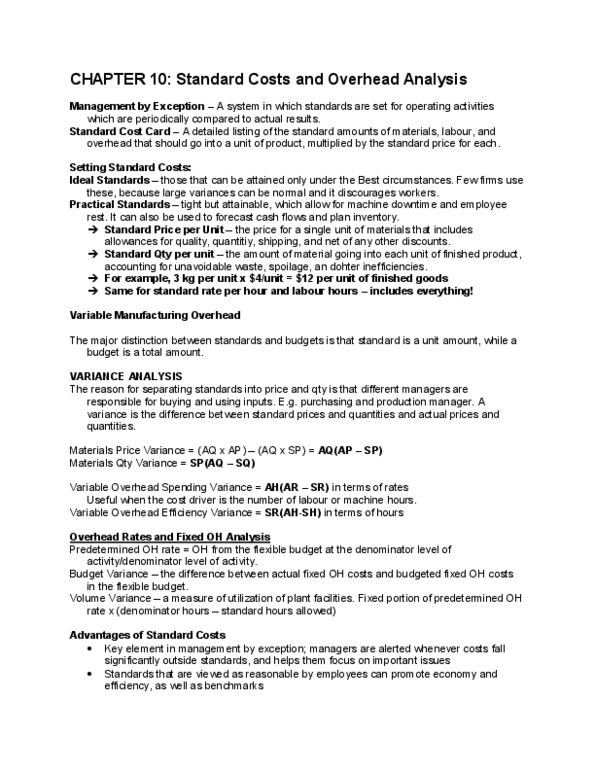

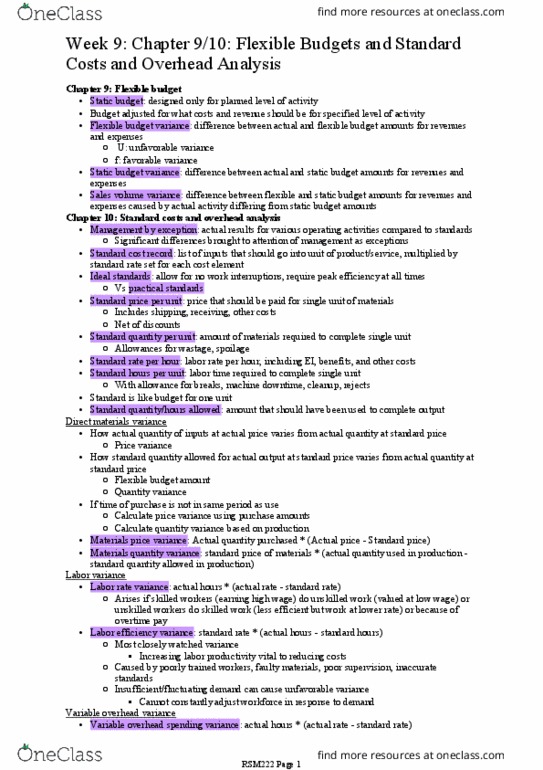

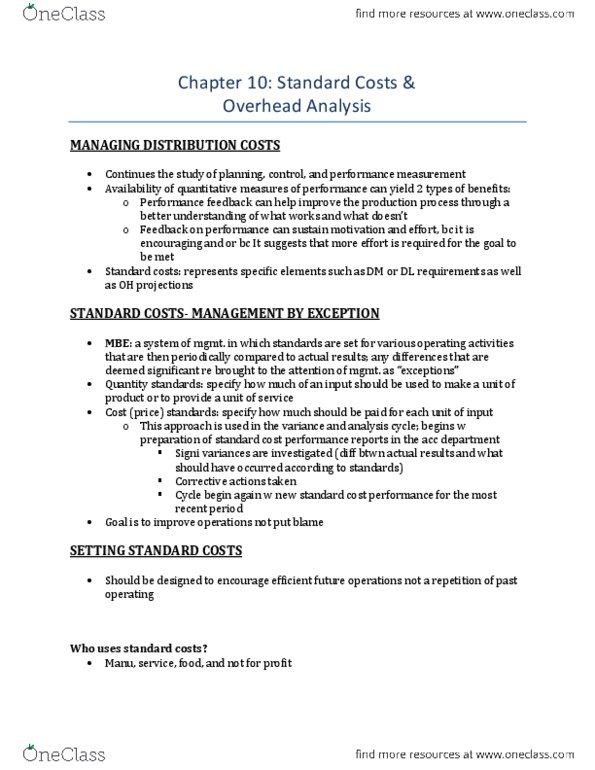

Standard cost = $ for one unit amount. Ideal standard optimum levels of performance under perfect conditions. Normal standard efficient levels under expected conditions. Standard benchmark setting for unit amount for all inputs. Standards for labour ensure they are working at efficient level to avoid waste. Wants to buy options to lock in the price. *learn adjusting entry for standard costs vs actual costs in appendix of textbook* Standards are benchmarks or norms for measuring performance. Quantity standards how much of an input should be used to make a product or provide a service. Cost standards how much should be paid for each unit of the inputs. If under variable costing approach, only add variable manufacturing o/h into standard cost. If under absorption costing, both variable + fixed manufacturing o/h into standard cost. Deviations from standard deem significant are then managed by exception. Important line items, or huge variances (by %)