Business Administration 2257 Lecture Notes - Lecture 4: Time Series, No Trend, Dependent And Independent Variables

5 Apr 2016

School

Department

Professor

Document Summary

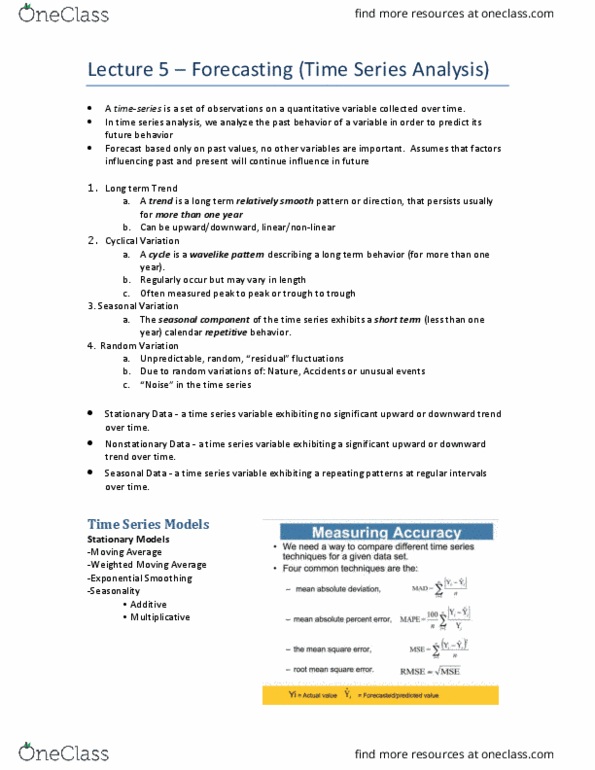

Growth (upward) or decline (downward) over long periods of ime: cycle. Measured from peak to peak or trough to trough. Example is business cycles of consumer conidence: seasonal variaion (type of cycle) Cycles within a calendar year (weekly, monthly, yearly, etc : irregular variaions. Erraic variance (noise) beyond tend, cycle, and/or seasonal variaion. Use past variaions to predict future values using extrapolaion: basic model. Time series regression (understand more about deiniions and results, not how computer computes these: (1) no trend model. If no meaningful trend, the best predictor of the future is the average of all past observaions. Yt (arrow poining up) = bo + et. Yt (arrow poining up) = predicted value of y at ime t. Bo = least squares point esimate of y = y (avg) = average value over n-ime observaions of y. Can use the no trend model to calculate a predicion interval for yt (arrow poining up)