Management and Organizational Studies 1023A/B Lecture Notes - Lecture 5: Edwin Sutherland, Donald Cressey, Differential Association

9 Mar 2015

School

Department

Professor

9

MOS 1023A/B Full Course Notes

Verified Note

9 documents

Document Summary

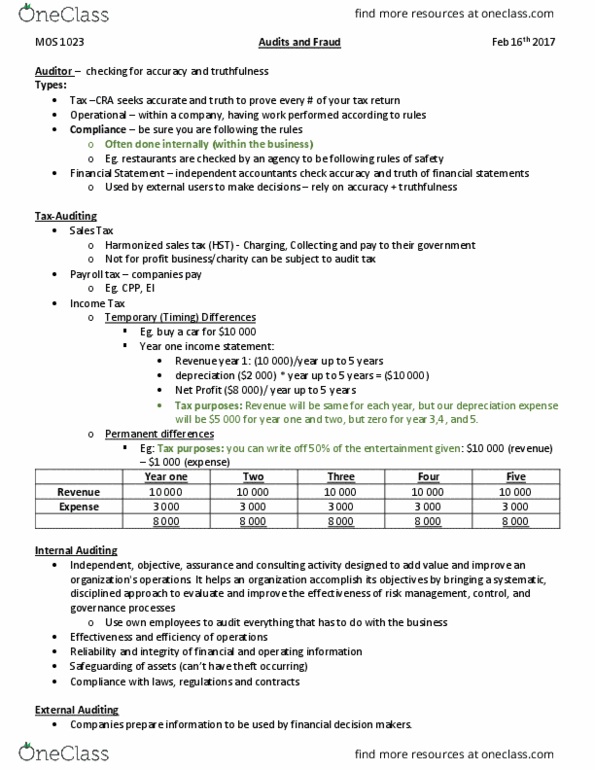

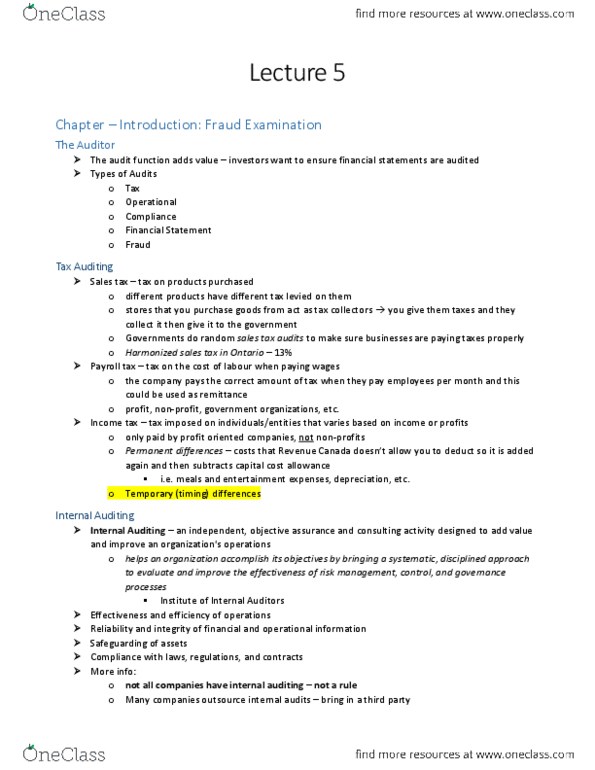

Types of audits: tax, operational, compliance, financial statement, fraud. Tax auditing: sales tax (hst) revenue generating concept for government, organization is tax collector, books must be audited if charging sales tax, if suspected of defrauding, can open books far back. Internal auditing independent, objective assurance designed to add value and improve an organization"s operations: not mandatory, happens later on as company grows to recognize needs, effectiveness and efficiency operation, safeguarding of assets, compliance with laws, regulations, contracts. Role of the auditor: determine whether the information in financial statements is reliable, and communicate findings to users (investors, process of reducing information risk. Business risk risk a company may fail to achieve its objectives due to: economic changes, technology changes, poor management, bad luck, auditors do not report on business risk. Fraud a deliberate deception practiced so as to secure unfair or unlawful gain.