Management and Organizational Studies 3370A/B Lecture Notes - Lecture 2: Opportunity Cost, Variable Cost, Fixed Cost

9 Nov 2017

School

Department

Professor

Document Summary

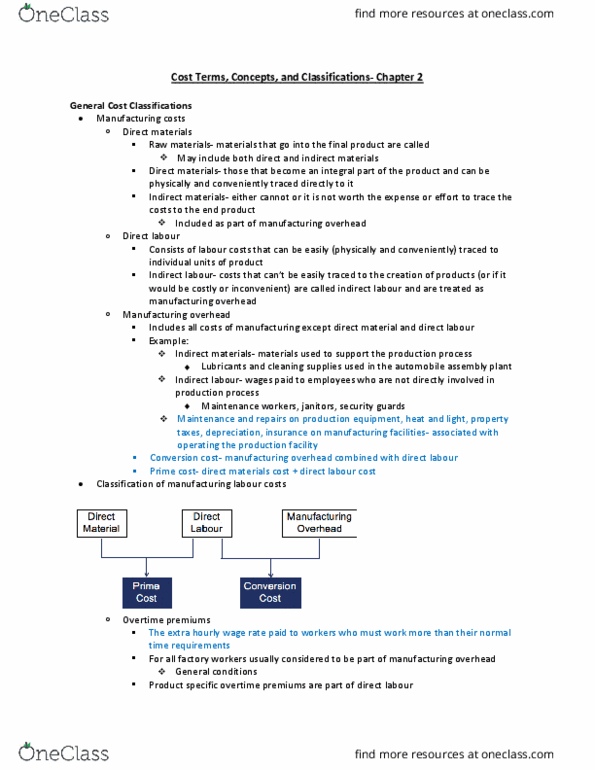

Buying seats from another company to put into train: materials that become an integral part of a finished product and can be traced to it, raw materials=materials used in final product (can be direct and indirect) Indirect materials= small items of material apart of finished product but costs of tracing do not exceed benefits: ex. the glue used in running shoes. Factory labour costs easily traced to individual units of product. Indirect labor: labour costs of janitors, supervisors, and factory workers that are not traced to directly to product. Part of manufacturing overhead: manufacturing overhead (or indirect manufacturing cost, factory overhead, factory burden, all costs associated with manufacturing (except direct material and direct labor) Ex. indirect materials, indirect labor, maintenance, repairs on equipment, heat, light, taxes, depreciation, insurance: conversion cost, direct labor cost plus manufacturing overhead cost (dl + moh) Prime cost: direct materials cost plus direct labour cost.