BU127 Lecture Notes - Lecture 1: International Financial Reporting Standards, Retained Earnings, Financial Statement

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

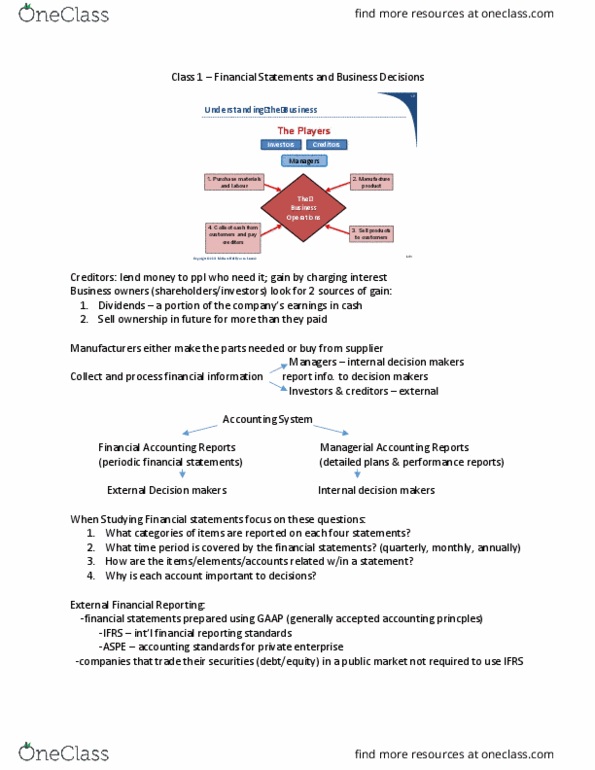

Investors: put money into the business, shareholders, hope to receive dividends or sell ownership later for more money. Creditors: lends money to the business, gain money by charging interest on the loan. Managers: run the business operations, will either manufacture products or get them from a supplier. The business operations: purchase materials and labour, manufacture product, sell products to customers, collect cash from customers and pay creditors. It collects and processes financial information for two parties: reports to managers (internal decision makers, reports to investors and creditors (external decision makers) Two types of reports for decision makers: financial accounting reports to external decision makers, managerial accounting reports to internal decision makers. The categories of items reported on the statements. The time period covered by the statements. The relationships between the elements listed on the statements. The importance of each element to decision making. Statement of financial position: repo(cid:396)ts the a(cid:373)ou(cid:374)t of assets, lia(cid:271)ilities, a(cid:374)d sha(cid:396)eholde(cid:396)s" e(cid:395)uity.