EC223 Lecture Notes - Lecture 11: Expected Return, Substitute Good, Dbrs

Document Summary

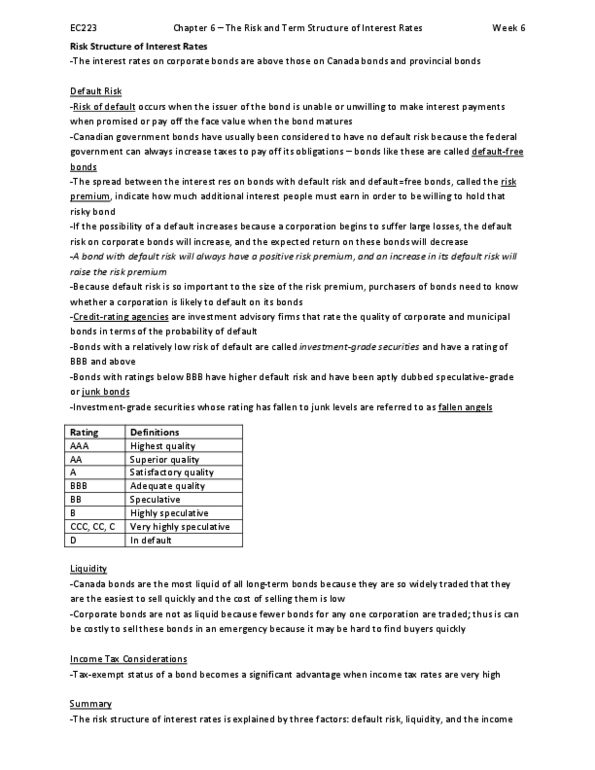

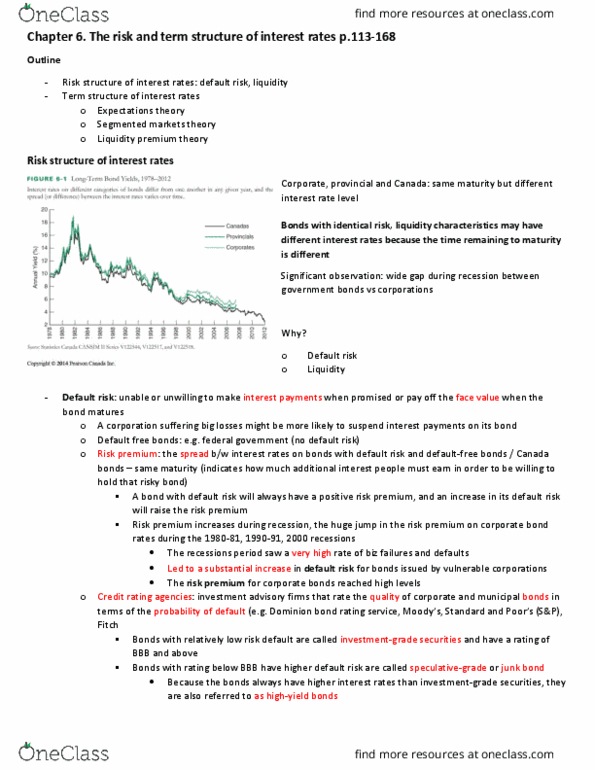

Monday, october 24, 2016 & wednesday, october 26, 2016 lectures 11 &12. Risk structure of interest rates: default risk, liquidity, income tax considerations. Term structure of interest rates: expectations period, segmented markets theory, liquidity premium theory. Bonds with the same term to maturity have different interest rates due to: risk, liquidity. Bonds with identical risks, __ characteristics may have different interest rates because the time remaining to maturity is different. Risk premium: the spread between the interest rates on bonds with default risk and the interest rates on (same maturity) canada bonds. Indicates how much additional interest people must earn in order to be willing to hold that risky bond: the higher the default risk is, the larger the risk premium will be. Investment advisory firms that rate the quality of corporate and municipal bonds in terms of the probability of default: e(cid:454): do(cid:373)i(cid:374)io(cid:374) bo(cid:374)d rati(cid:374)g e(cid:396)vi(cid:272)e, mood(cid:455)"s, ta(cid:374)da(cid:396)d a(cid:374)d poo(cid:396)"s (cid:894) *p(cid:895), fit(cid:272)h.