ADMS 1500 Lecture Notes - Activity-Based Costing, Contribution Margin, Fixed Cost

16 Oct 2011

School

Department

Course

Professor

Document Summary

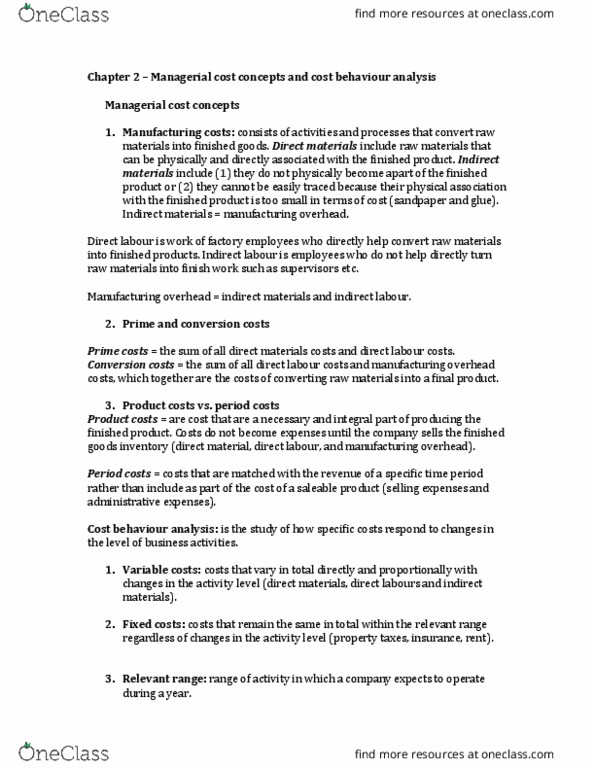

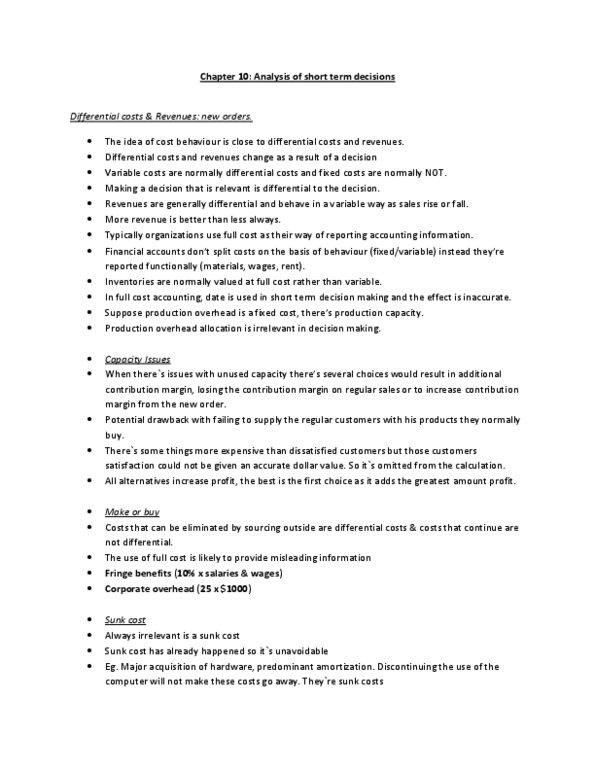

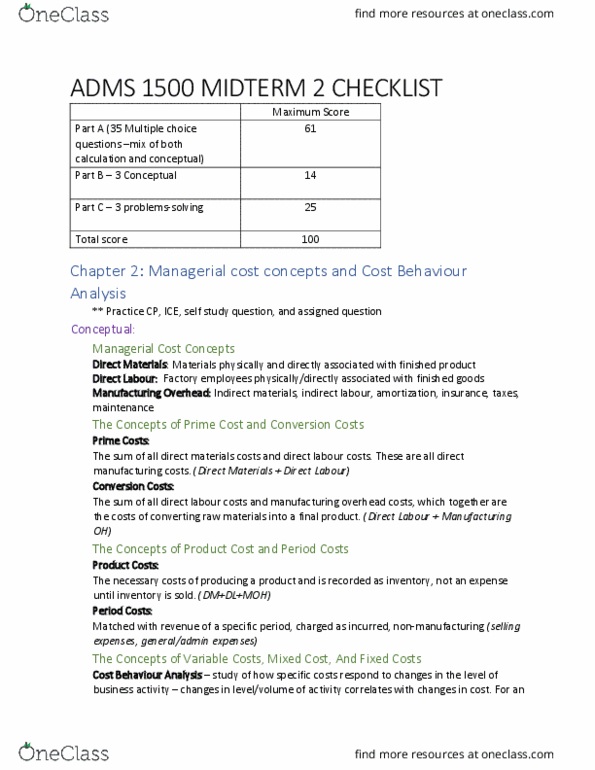

Cost behaviour: describes the relationship between cost & different activity levels variable, fixed, and mixed. Fixed costs: constant at all predetermined activities (eg: rent, heating, property tax, & management salaries); are still incurred as expense. Mixed costs: costs that do not fall into either category because they are made up of a fixed element and a variable element (electricity, cars) The break-even model: relationship between costs & revenues to determine the operating income at any level of activity; useful planning & decision support tool. Contribution margin: difference between selling price & variable cost; measures how much better off the company is as a result of the sale of one additional unit. Activity above break-even point: every unit sold above break-even point, contribution margin is pure profit; the greater the number sold, higher the profit becomes. Using the break-even model to analyze changes: used to evaluate wide range of decisions. Unit-variable costs: change with the number of units sold or produced.