TAX 3300 Lecture Notes - Lecture 6: Intangible Asset, Ordinary Income, Capital Asset

Document Summary

Get access

Related Documents

Related Questions

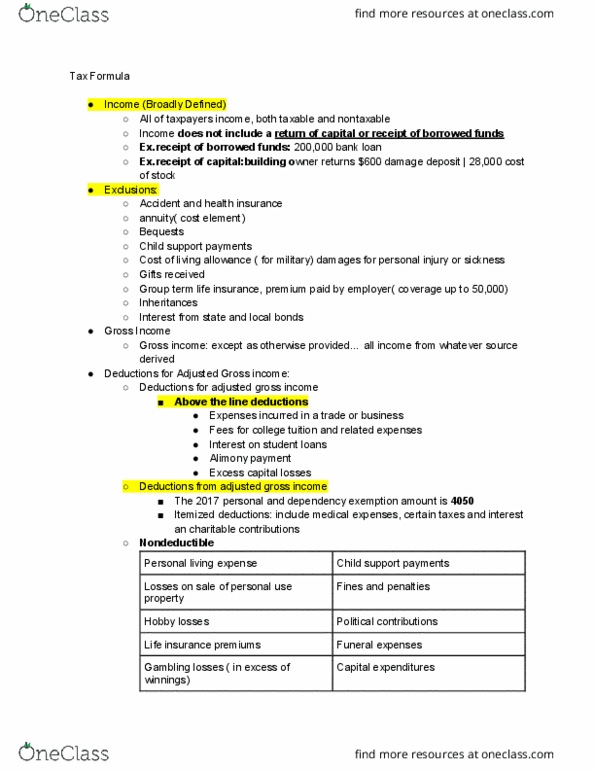

| Alexa owns a condominium near Cocoa Beach in Florida. This year, she incurs the following expenses in connection with her condo: |

| Insurance | $3,800 |

| Mortgage interest | 11,200 |

| Property taxes | 3,800 |

| Repairs & maintenance | 950 |

| Utilities | 3,700 |

| Depreciation | 19,100 |

| During the year, Alexa rented out the condo for 170 days. Alexaâs AGI from all sources other than the rental property is $200,000. Unless otherwise specified, Alexa has no sources of passive income. |

| Assume that in addition to renting the condo for 170 days, Alexa uses the condo for eight days of personal use. Also assume that Alexa receives $43,000 of gross rental receipts. Answer the following questions: |

| a. | What is the total amount of for AGI deductions relating to the condo that Alexa may deduct in the current year? Assume she uses the IRS method of allocating expenses between rental and personal days. (Do not round intermediate calculations. Round your final answers to the nearest whole dollar amount. Amounts to be deducted should be indicated with a minus sign.) |

| |

| b. | What is the total amount of from AGI deductions relating to the condo that Alexa may deduct in the current year? Assume she uses the IRS method of allocating expenses between rental and personal days. (Do not round intermediate calculations. Round your answer to the nearest whole dollar amount. Amounts to be deducted should be indicated with a minus sign.) |

| c. | Would Alexa be better or worse off after taxes in the current year if she uses the Tax Court method of allocating expenses? | ||||

|

During 2015, George, a salaried taxpayer, paid the followingtaxes which were not incurred in connection with a trade orbusiness: Federal income tax withheld by employer $1,500; Stateincome tax withheld by employer $1,100; FICA tax withheld byemployer $700; Real property taxes $900; Federal auto gasolinetaxes $300; Federal excise tax on telephone bills $50. What amountcan George claim for 2015 as an itemized deduction for the taxespaid, assuming he elects to deduct state and local incometaxes?

| A. | $1,400 | |

| B. | $1,100 | |

| C. | $1,150 | |

| D. | None are correct | |

| E. | $2,000 |

Choose the correct statement:

| A. | If a financial planner becomes certified, then he/she may notdeduct the Certified Financial Planner (CFP) dues because it is notnecessary to be certified in order to engage in the business ofbeing a financial planner. | |

| B. | If a taxpayer does a lot of business travel, the taxpayer maydeduct the amount paid for an airline club membership. | |

| C. | None are correct | |

| D. | Membership dues to a golf club are deductible as long as thereis a business purpose. | |

| E. | In order to be deductible, dues and subscriptions must berelated to the taxpayerâs occupation. |

For 2015, Eugene and Linda had adjusted gross income of $30,000.Additional information for 2015 is as follows: Cash contribution tochurch $1,500; Tuition paid to a parochial school $1,200;Contribution to the American Red Cross $400; Cash contribution to aneedy family $75. What is the maximum amount that they can use as adeduction for charitable contributions for 2015?

| A. | $1,900 | |

| B. | $1,975 | |

| C. | none are correct | |

| D. | $3,175 | |

| E. | $3,000 |

For the year ended December 31, 2015, David, a married taxpayerfiling a joint return, reported the following: Investment incomefrom interest $24,000; Investment expenses other than interest$4,000; Interest expense on funds borrowed in 2006 to purchaseinvestment property $70,000. What is the maximum amount that Davidcan deduct in 2015 as investment interest expense?

| A. | $7,000 | |

| B. | $20,000 | |

| C. | None are correct | |

| D. | $21,000 | |

| E. | $24,000 |

Barry is a self-employed attorney who travels to New York on abusiness trip during 2015. Barry's expenses were as follows:Airfare $560; Taxis $40; Meals $200; Lodging $350. How much mayBarry deduct as travel expenses for the trip?

| A. | $1,050 | |

| B. | $1,000 | |

| C. | $950 | |

| D. | None are correct | |

| E. | $0 |

Christine saw a television advertisement asking for donations ofused vehicles to a charitable foundation and decided to donate herold car. Which of the following statements is correct?

| A. | She can take a deduction greater than the amount for which thecharity actually sells the vehicle. | |

| B. | She can claim an estimated value for the auto if the charityuses it rather than selling it. | |

| C. | The charity is not required to provide her with any informationabout what they do with the auto. | |

| D. | She can take a tax deduction large enough on an after-tax basisto equal the amount she would have received if she sold the cardirectly. |