ACC 442 Lecture Notes - Lecture 14: Public Company Accounting Oversight Board, International Accounting Standards Board, Auditing Standards Board

Financial Statements are...

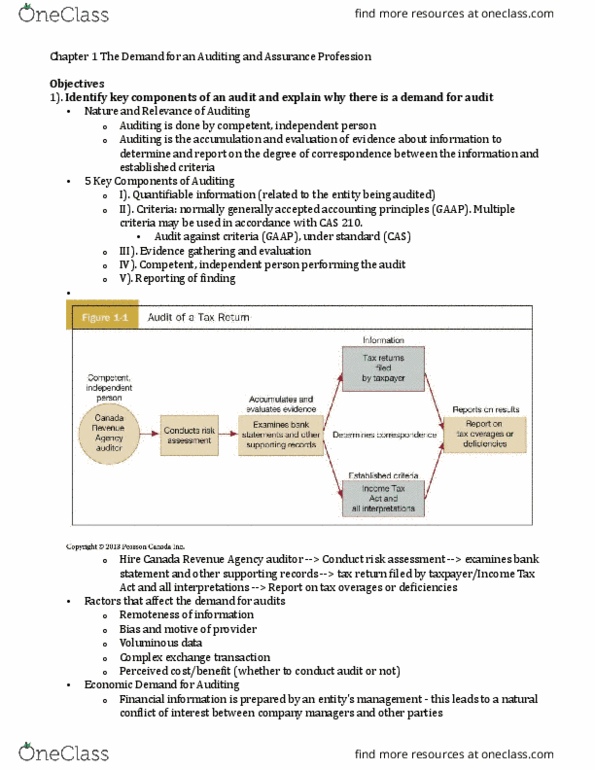

A summary of events

Phases of Audit

Client acceptance/Continuance

Plan the audit

Consider and audit internal control

Perform substantive testing

Complete the audit

Evaluate results and issue audit report

Auditing

Process of obtaining and evaluating evidence regarding assertions about economic actions and events,

then communicating the results to interested users

Assurance as to whether or not management is reporting financial info based on GAAP, with no material

misstatements

Attest

Not as rigorous as auditing (10-Q)

Assurance

Independent professional services that improve quality of information for decision makers

Audit Opinion big picture

"What you see, is what you get"

Principal Agent Theory

Information asymmetry

Conflict of interest

Monitoring problems

find more resources at oneclass.com

find more resources at oneclass.com

Moral hazard

Agency costs

Solution: monitoring

Materiality

How wrong do financial statements need to be before a financial statement user would change their

economic decision

"Big Deal" Threshold

Materiality Rule of Thumb

5% of Pretax Income

Qualitative factors matter too

Audit Risk

Risk of issuing a clean opinion when there is a material misstatement

Audit Report provides only 'reasonable assurance"

Evidence

Anything an auditor looks at and/or observes

Sampling

Can't look at everything, so we pick a percent of things/transactions to look at

Audit Report

Title

Audience

Intro Paragraph

find more resources at oneclass.com

find more resources at oneclass.com

Scope Paragraph

Opinion Paragraph

Explanatory Paragraph

Audit Firm and Report Date

Four Types of Reports

Unqualified - good to go

Qualified - some sort of limitation ("all is good except for...")

Adverse - financials are super messed up, don't trust

Disclaimer - auditor does not issue an opinion, too much missing

Types of Auditors

External - CPA

Internal - industry

Government - government agencies (FBI, IRS, etc.)

Forensic - detect fraud

Academic - University professors

Public Accounting Firms

Limited Liability Partnership

Partners not responsible for fraud, only the person involved in the fraud

Audit Teams

Associate/staff, Senior, Manager, Partner

Sarbanes Oxley Act (SOX)

Only for public companies

Prohibited non-audit services other than tax planning

Audit partner rotation every five years

Board of Directors hires the auditor

find more resources at oneclass.com

find more resources at oneclass.com