ACCT 1A Lecture Notes - Lecture 12: Management Accounting, Target Costing

Document Summary

Get access

Related Documents

Related Questions

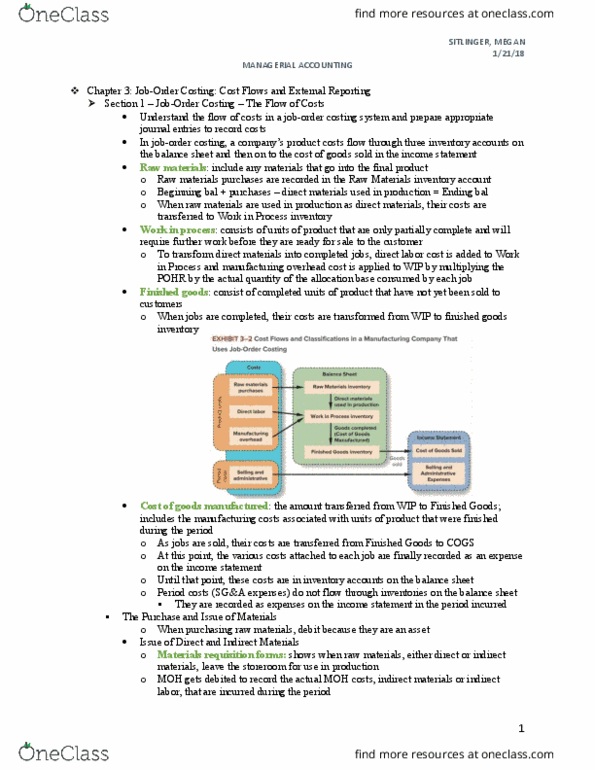

1.) When products held in inventory are sold:

A.)Cost of Goods Sold is credited.

B.)Work in Process Inventory is credited.

C.)Finished Goods Inventory is credited.

D.)Finished Goods Inventory is debited.

2.)Since manufacturing costs (direct materials, direct labor,and overhead) are incurred in the process of manufacturing units ofproduct, these costs are credited t

| A.) | The Direct Materials Inventory, Direct Labor, and ManufacturingOverhead accounts respectively. |

| B.) | Liability accounts. |

| C.) | The Work in Process Inventory account. |

| D.) | The Cost of Goods Sold account. |

3.)Management accounting systems are designed to assistorganizations in the performance of all of the following functionsexcept:

| A.) | The assignment of decision-making authority over companyassets. |

| B.) | Planning and decision-making. |

| C.) | Monitoring, evaluating, and rewarding performance. |

| D.) | The preparation of income tax returns. |

4.)In a schedule of cost of finished goods manufactured, thefigure for total manufacturing costs:

| A.) May be less than the cost of direct materials used. | |

| B.) May be less than the direct labor costs assigned toproduction. | |

| C.) May be less than the manufacturing overhead applied toproduction. | |

| D.) May be less than the cost of finished goodsmanufactured. |

5.) When a manufacturing company purchases raw materials orcomponent parts to be used in manufacturing finished goods, thesecosts are initially debited to:

| A.) Expense accounts. | |

| B.) Raw Materials Inventory. | |

| C.) Finished Goods Inventory. | |

| D.) Manufacturing Overhead. |

6.) The wages paid to employees working directly on a company'sproducts would be shown as a:

| A.) Credit to Direct Labor. | |

| B.) Debit to Direct Labor. | |

| C.) Credit to Work in Process. | |

| D.) Debit to Manufacturing Overhead. |

7.) Amounts credited to the Work in Process inventory accountmay best be described as:

| A.) The cost of finished goods manufactured. | |

| B.) Total manufacturing costs charged to production. | |

| C.) The cost of goods sold. | |

| D.) Direct materials purchased, direct labor costs paid, andpayments for items classified as manufacturing overhead. |

1. Sydney's Barbecue reported the following information:

Sydney's Barbecue

Period Ending December 31, 20XX

| Manufacturing costs | $5,400,000 |

| Units manufactured | $54,000 |

| Beginning inventory in Units | $ 0 |

Note: 45,600 units sold during year at $300 per unit

What is the amount of ending finished goods inventory for theperiod ending December 31, 20XX?

| $860,000 | |

| $830,000 | |

| $840,000 | |

| $850,000 | |

| $820,000 |

2.Net income reported under absorption costing will exceed netincome reported under variable costing for a given period if

| production equals sales for thatperiod. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| variable overhead exceeds fixedoverhead for that period. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| production exceeds sales for thatperiod. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| sales exceed production for that period. 3. A company manufactures wallets. Last month's costs were aslisted below:

What were the conversion costs for the month?

|