ACCT 121 Lecture 2: Chap 2 Part 8

Document Summary

Get access

Related Documents

Related Questions

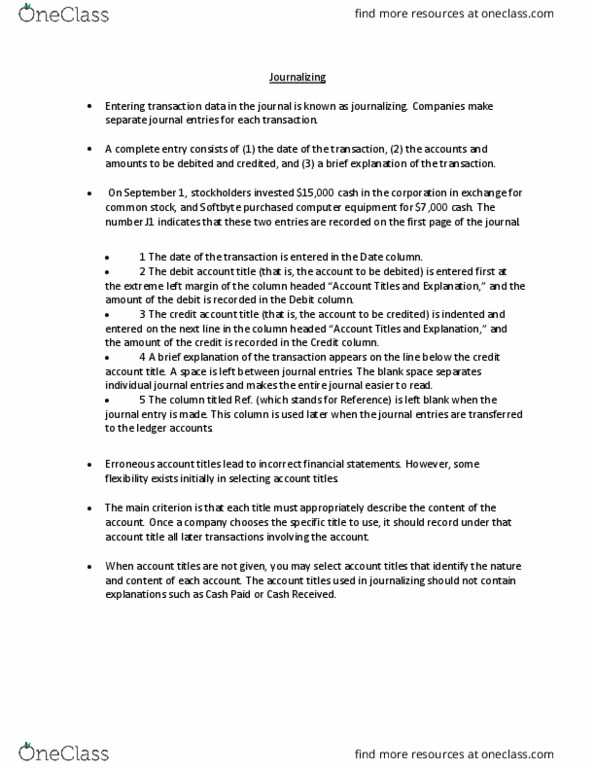

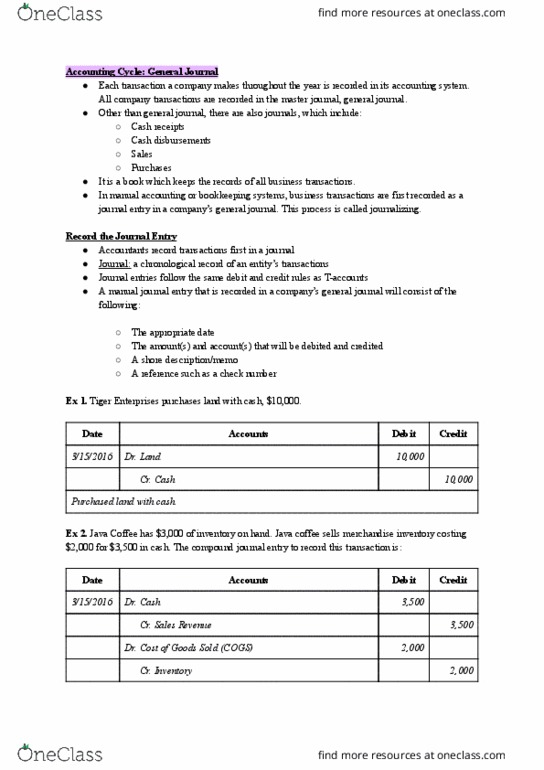

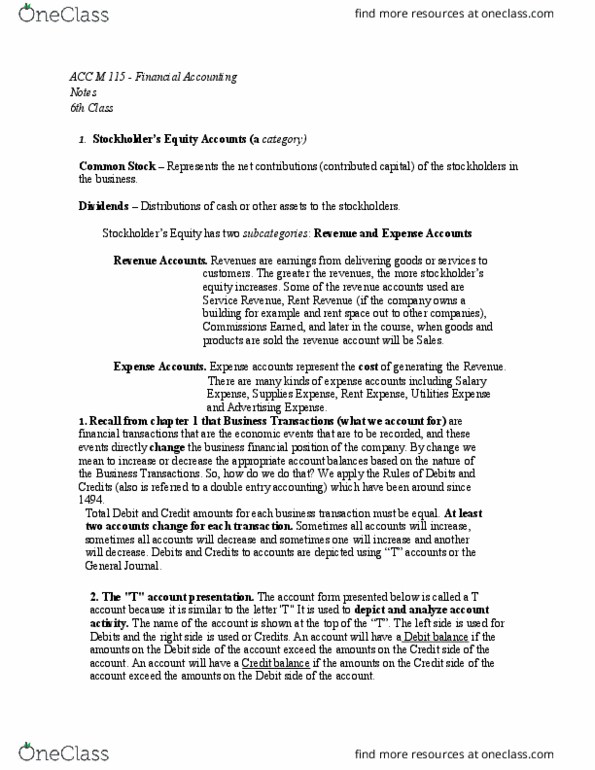

Recording Transactions (Including Adjusting and Closing Entries), Preparing Financial Statements, and Performing Ratio Analysis

Josh and Kelly McKay began operations of their furniture repair shop (Furniture Refinishers, Inc.) on January 1, 2016. The annual reporting period ends December 31. The trial balance on January 1, 2017, was as follows:

| Account Titles | Debit | Credit |

| Cash | â5,000 | |

| Accounts receivable | â4,000 | |

| Supplies | â2,000 | |

| Small tools | â6,000 | |

| Equipment | ||

| Accumulated depreciation (on equipment) | ||

| Other assets (not detailed to simplify) | â9,000 | |

| Accounts payable | â7,000 | |

| Notes payable | ||

| Wages payable | ||

| Interest payable | ||

| Income taxes payable | ||

| Unearned revenue | ||

| Common stock (60,000 shares, $0.10 par value) | â6,000 | |

| Additional paid-in capital | â9,000 | |

| Retained earnings | â4,000 | |

| Service revenue | ||

| Depreciation expense | ||

| Wages expense | ||

| Interest expense | ||

| Income tax expense | ||

| Remaining expenses (not detailed to simplify) | ||

| âTotals | 26,000 | 26,000 |

Transactions during 2017 follow:

A.Borrowed $20,000 cash on July 1, 2017, signing a one-year, 10 percent note payable.

B.Purchased equipment for $18,000 cash on July 1, 2017.

C.Sold 10,000 additional shares of capital stock for cash at $0.50 market value per share at the beginning of the year.

D.Earned $70,000 in revenues for 2017, including $14,000 on credit and the rest in cash.

E.Incurred remaining expenses of $35,000 for 2017, including $7,000 on credit and the rest paid with cash.

F.Purchased additional small tools, $3,000 cash.

G.Collected accounts receivable, $8,000.

H.Paid accounts payable, $11,000.

I..Purchased $10,000 of supplies on account.

J.Received a $3,000 deposit on work to start January 15, 2018.

K.Declared and paid a cash dividend, $10,000.

Data for adjusting entries:

L.Supplies of $4,000 and small tools of $8,000 were counted on December 31, 2017 (debit Remaining Expenses).

M.Depreciation for 2017, $2,000.

N.Interest accrued on notes payable (to be computed).

O.Wages earned since the December 24 payroll but not yet paid, $3,000.

P.Income tax expense was $4,000, payable in 2018.

Required:

1.Set up T-accounts for the accounts on the trial balance and enter beginning balances.

2.Prepare journal entries for transactions (a) through (k) and post them to the T-accounts.

3.Journalize and post the adjusting entries (l) through (p).

4.Prepare an income statement (including earnings per share rounded to two decimal places), statement of stockholdersâ equity, and balance sheet.

5.Identify the type of transaction for (a) through (k) for the statement of cash flows (O for operating, I for investing, F for financing), and the direction and amount of the effect.

6.Journalize and post the closing entry.

7.Compute the following ratios (rounded to two decimal places) for 2017 and explain what the results suggest about the company:

a,Current ratio

b,Total asset turnover

c,Net profit margin

Now that you have reviewed information about Hi-Fi Way, you are ready to begin the first step in the accounting cycle, recording transactions. On this page of the practice set, you are asked to record transactions that occurred during the first week of June into the company's journals and post the appropriate entries to the ledger accounts. The following transactions occurred throughout the first week of June:

| Week 1 | ||

| Date | Transaction description | |

| 1 | Issued Check No. 570 for $8,400 to pay Realty Bites for two month's worth of rent in advance. | |

| 1 | Obtained a loan of $59,000 from ZNZ Bank at a simple interest rate of 6% per year. The first interest payment is due at the end of August 2017 and the principal of the loan is to be repaid on June 1, 2021. | |

| 3 | Made payment of $764 to Integer Energy for 3 months of electricity up to and including May 31, Check No. 571. | |

| 4 | Turbo Tech paid the full amount owing on their account. | |

| 4 | Paid sales staff wages of $13,224 for the week up to and including yesterday, Check No. 572. Note that $6,637 of this payment relates to the wages expense incurred during the last week of May. | |

| 5 | Paid the full amount owing to Big Telco, Check No. 573. | |

| 7 | Issued Check No. 574 to Office Supplies Warehouse for the purchase of $301 worth of office supplies. | |

After completing this practice set page, you should know how to record basic transactions in the journals provided below and understand the posting process in the manual accounting system. Note that you will record the remaining June transactions in the following sections of this practice set.

Remember, one purpose of using special journals is to make the posting process more efficient by posting the total of most columns in the special journals after all of the transactions for the period have been recorded. However, some parts of a journal entry are still required to be posted on a daily basis. View the company's accounting policies and procedures for details of what is to be posted daily or monthly.

Instructions for week 1

1)Record all week 1 transactions in the relevant journals.

Note that special journals must be used where applicable. Any transaction that cannot be recorded in a special journal should be recorded in the general journal.

2)Post entries recorded in the journals to the appropriate ledger accounts according to the company's accounting policies and procedures.

Note that the relevant totals of the special journals will be posted to the general ledger accounts at the end of the month. You will enter this before you prepare the Bank Reconciliation Statement.

Remember to enter all answers to the nearest whole dollar. When calculating a discount, if a discount is not a whole number, round the discount to the nearest whole dollar. Then, to calculate the cash amount, subtract the discount from the original amount.

Additional instructions

Displaying selected accounting records:

To save space, not all accounting records (e.g. journals and ledgers) will be displayed on every page. However, on each page you can access all accounting records necessary to answer the questions on that page.

There are several tabs representing different views of the accounting records. The active tab by default is Show All, but you may also select to view just one particular accounting record by selecting the appropriate tab.

If you fill in any accounting records and change the view on the page by selecting a different tab, the information that you have entered will remain in that accounting record and be displayed whenever you can see that accounting record.

Before submitting your answers, we recommend that you click the Show All tab and check that all relevant accounting records have been completed. You are required to complete all relevant accounting records before pressing the Submit answers button. Once submitted, you will not be able to return to the page to re-enter or alter your answers.

Journals:

Each transaction recorded in a special journal must be entered in one line. In order to receive full points, you must not split up the relevant transaction into more than one line in the special journal.

For certain transactions in special journals, some accounting textbooks do not always require an account to be chosen under the column labeled Account. In this practice set you arerequired to select an account for each transaction in the special journals. Specifically, in all special journals, under the column labeled Account, you must select the correct account name for each transaction in order to receive full points. Note that for some transactions, this will mean that the account name selected will correspond to the heading of one of the columns in that special journal.

For each journal, in the Post Ref. column you will need to correctly type the account number of the account you are posting to. In particular, in special journals, some accounting textbooks do not always require a reference to be recorded in the Post Ref. column. In this practice set, in order to receive full points, every transaction entered in a special journal requires an entry in the Post Ref. column. Note that in the special journals, if the account name selected for a transaction corresponds to the heading of one of the columns in that special journal, the post ref is to be recorded as an X. This is because these transactions are not posted on a daily basis. In order to receive full points, you must record only the letter Xin the Post Ref. column for these transactions.

Note that in special journals, the Other Accounts column should not be used to record movements of inventory.

There may be entries in the general journal that require posting to both a control account and a subsidiary ledger. In these cases, after you have posted to both ledgers, you should enter the reference for both the general ledger account and the subsidiary ledger account in the Post Ref. column to indicate that you have posted to both accounts. For example, if the reference number for the control account is 110 and the reference number for the subsidiary ledger account is 110-1, you should type '110/110-1' into the Post Ref. column.

General journal entries do NOT require a description of the journal entries.

Ledgers:

When posting a transaction to a ledger account, under the Description column, please type the description of the transaction directly into the field. The exact wording does not matterfor grading purposes. For example, it does not matter in an electricity transaction if you type 'Paid for electricity' or 'Paid electricity bill'.

For each ledger, under the Ref. column, you need to select the correct journal from a list in the drop-down box provided in order to receive full points.

If the balance of a ledger account is zero you do not need to select a debit or credit from the drop-down box.

Each transaction posted to the subsidiary ledgers must be entered in one line. In order to receive full points, you must not split up the relevant transaction into more than one line in the subsidiary ledger.

Both journals and ledgers:

Most journals and ledgers will have blank rows left at the end of the page.

Some journals and ledgers may not require any entries.

When purchases and sales are recorded in special journals, changes in inventory must not be posted to the Merchandise Inventory account in the general ledger on a daily basis.