BLS 342 Lecture Notes - Lecture 20: Capital Structure, Investment, Double Taxation

7 Sep 2016

School

Department

Course

Professor

Document Summary

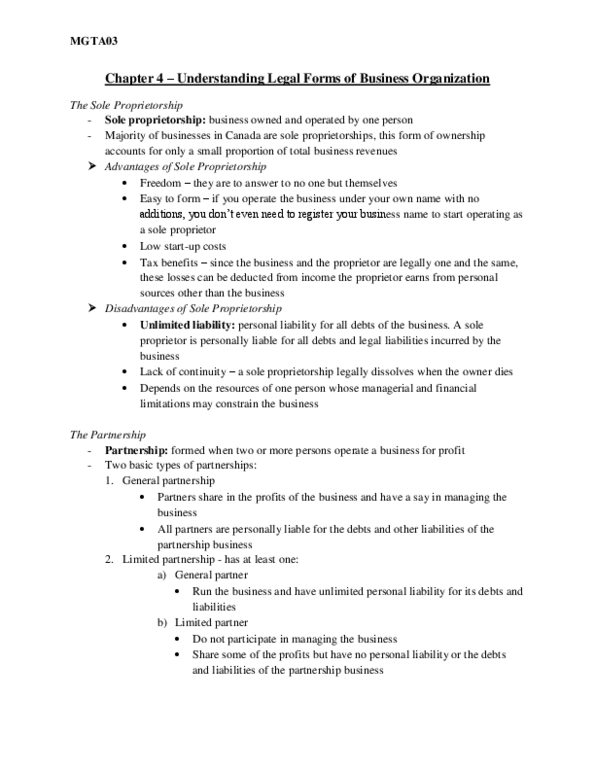

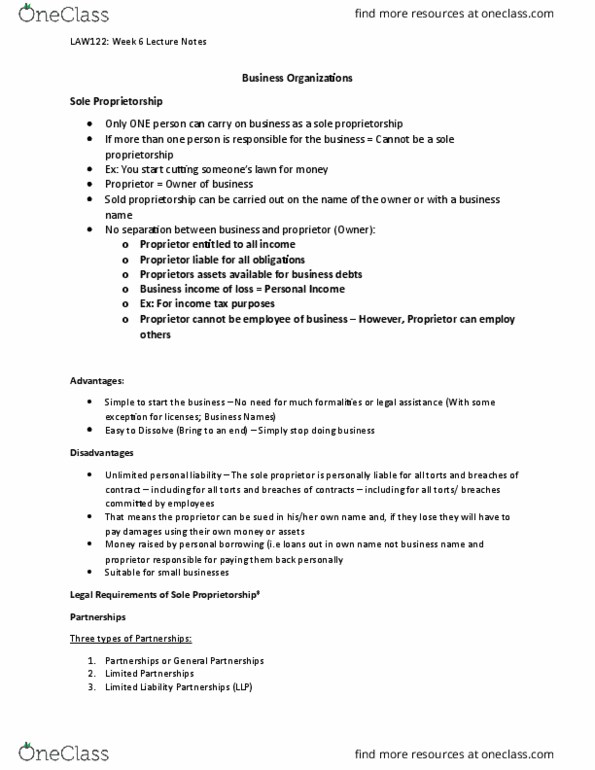

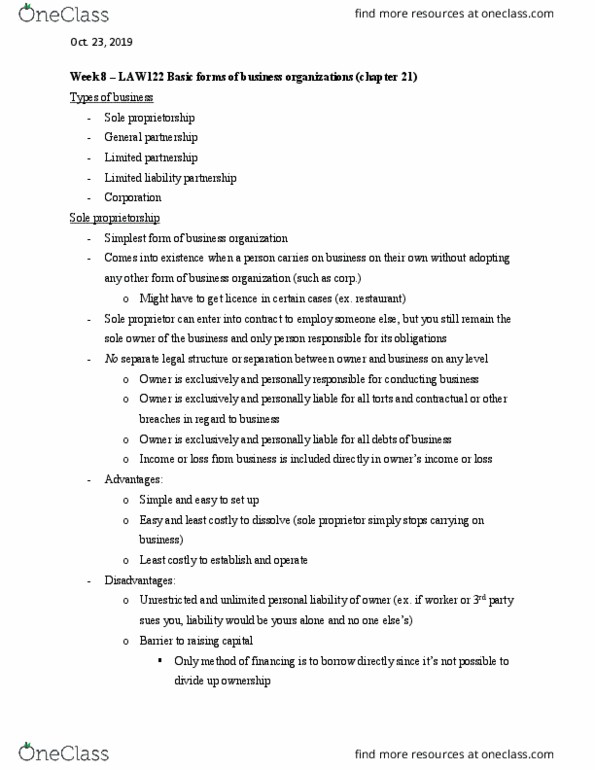

Types of business organizations: sole proprietorship, partnership, limited liability company not a corporation, corporation. When an individual goes into business by themselves. You alone are in charge of management of the company. Owner of a sole proprietorship incurs debts personally not as a business. Non transferable dissolve when proprietor dies or decides to stop doing business. Ex. girl making/selling jewelry and a baby chokes on it, she is liable. Assumed to be a 50/50 split of everything unless otherwise stated. More than one person enters a business and agree to share, split, and control profits, mgt, responsibilities equally, zero formal requirements. Income is taxed as individual income per partner and partners can deduct losses from taxable income. Partners are personally liable for partnership debts equally regardless of which partner is at fault. Defines a partnership as an association of 2 or more people/groups who voluntarily and consensually enter into an agreement to do business.