ACCT-GB 3150 Lecture Notes - Lecture 5: Income Statement, Financial Statement, Accounts Receivable

61 views3 pages

3 Oct 2016

School

Department

Course

Professor

Document Summary

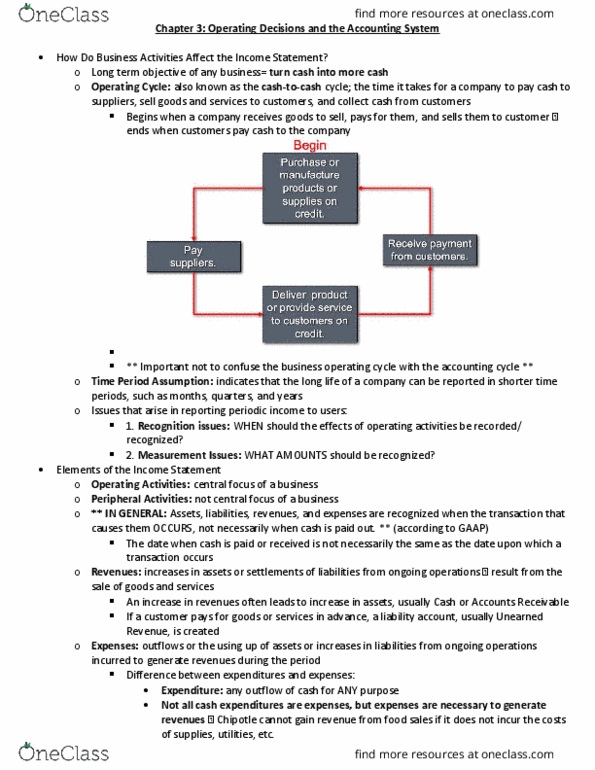

Long-term objective for any business is to turn cash into more cash. If the company is to stay in business, this excess cash must be generated from operations, not from borrowing money or selling long-lived assets. The operating (cash-to-cash) cycle begins when a company receives goods to sell, pays for them, and sells to customers; it ends when customers pay cash to the company. To measure income for a specific time period of time, accountants follow the time period assumption, which assumes that the long life of a company can be reported in short-time periods, such as months, quarter s and years. There are two types of issues that arise in reporting periodic income to users: Revenues are defined as increases in assets or settlements of liabilities from ongoing operations of business. Operating revenues result from the sale of goods and services. When revenue is earned, assets usually cash or accounts receivable often increase.

Get access

Grade+

$40 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

10 Verified Answers

Class+

$30 USD/m

Billed monthly

Homework Help

Study Guides

Textbook Solutions

Class Notes

Textbook Notes

Booster Class

7 Verified Answers