Economics A100 Lecture Notes - Lecture 13: Economic Equilibrium, Perfect Competition, Demand Curve

28 Dec 2020

School

Department

Course

Professor

Document Summary

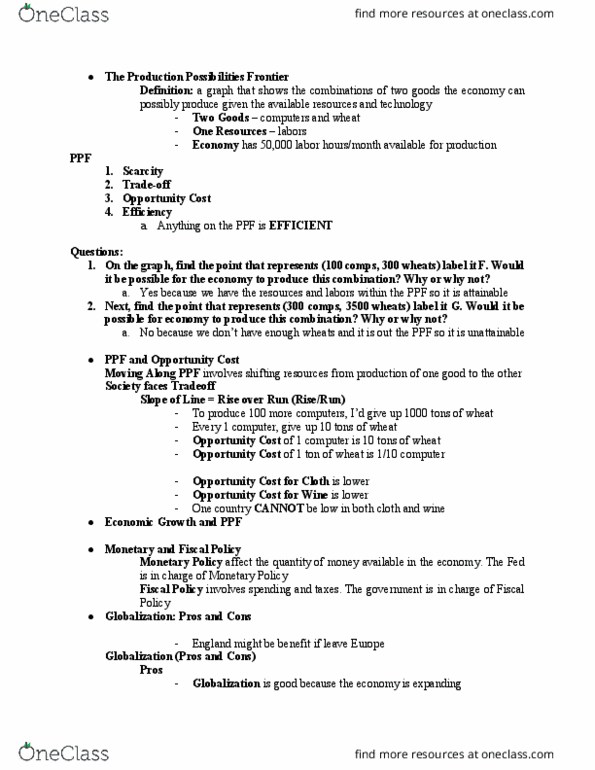

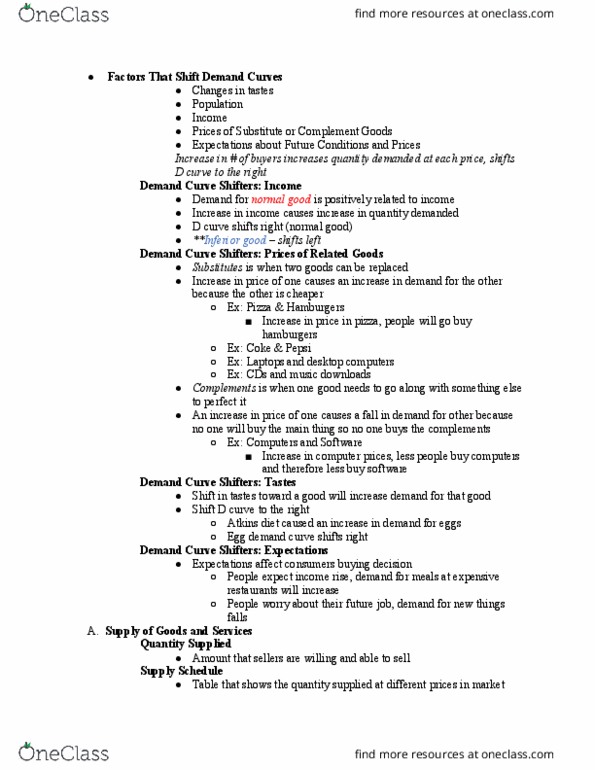

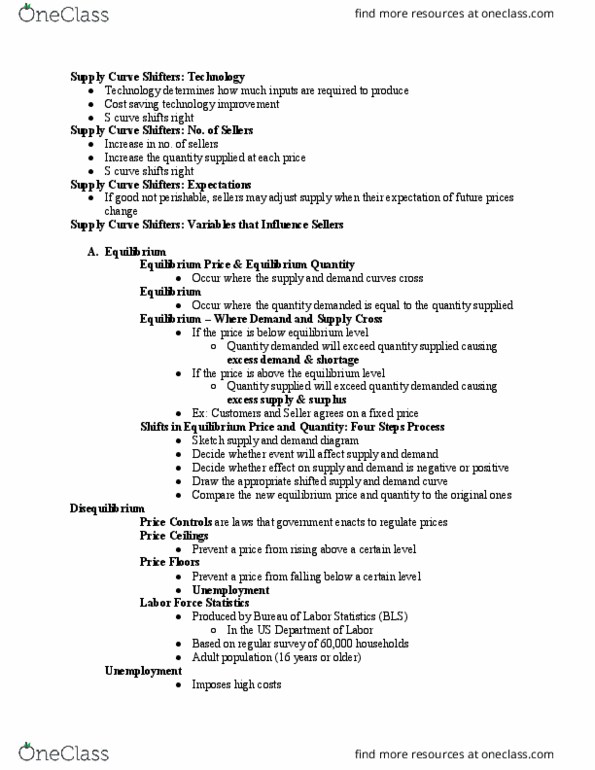

A group of buyers and sellers of a particular good or service. A market is competitive if there are so many buyers and so many sellers that each has a negotiable impact on the market price. Buyers and sellers in this case are price takers because they must accept the price that the market determines. Monopoly: only one seller in the market, and this seller determines the price (opposite of perfect competition) Quantity demanded= the amount of the good that buyers are willing and able to purchase. Law of demand: other things equal, when the price of a good rises, the quantity demanded falls, and when the price falls, the quantity demanded rises. Demand schedule: a table that shows the relationship between the price of a good and the quantity demanded, holding constant everything else that influences how much of the good consumers want to buy. Demand curve: the downward-sloping line relating price and quantity demanded.