FINC-220 Lecture Notes - Lecture 10: Economic Equilibrium, Expected Return, Capital Asset Pricing Model

Chapter 13

Return, risk and the security market line

Chapter outline

• Expected Returns and Variances

• Portfolios

• Announcements, Surprises, and Expected Returns

• Risk: Systematic and Unsystematic

• Diversification and Portfolio Risk

• Systematic Risk and Beta

• The Security Market Line

• The SML and the Cost of Capital: A Preview

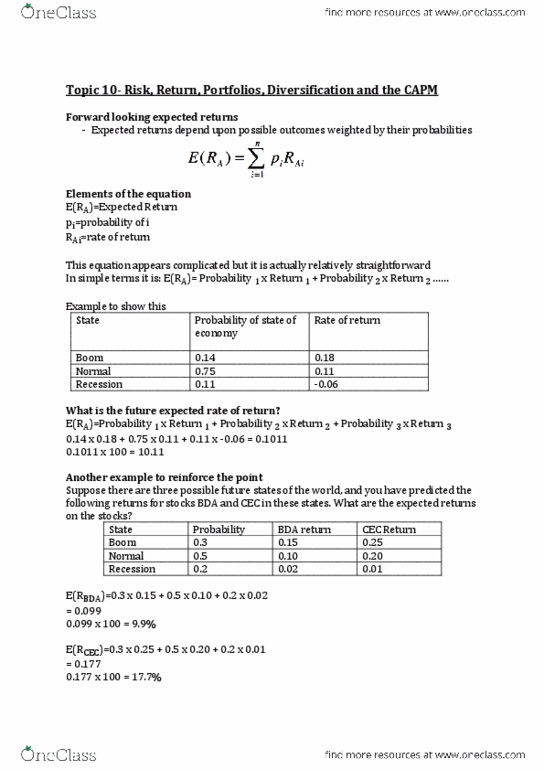

Expected returns

• Expected returns are based on the probabilities of possible outcomes

å

n

i

ii RpRE

1

)(

find more resources at oneclass.com

find more resources at oneclass.com

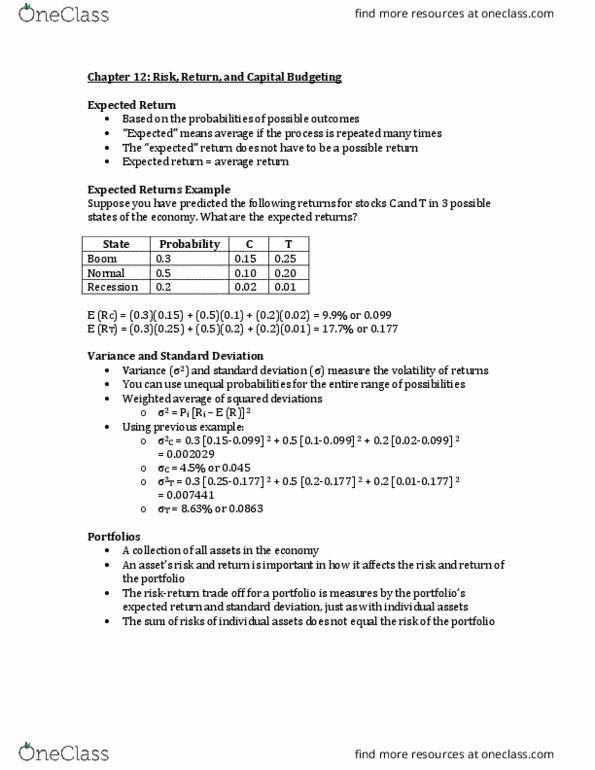

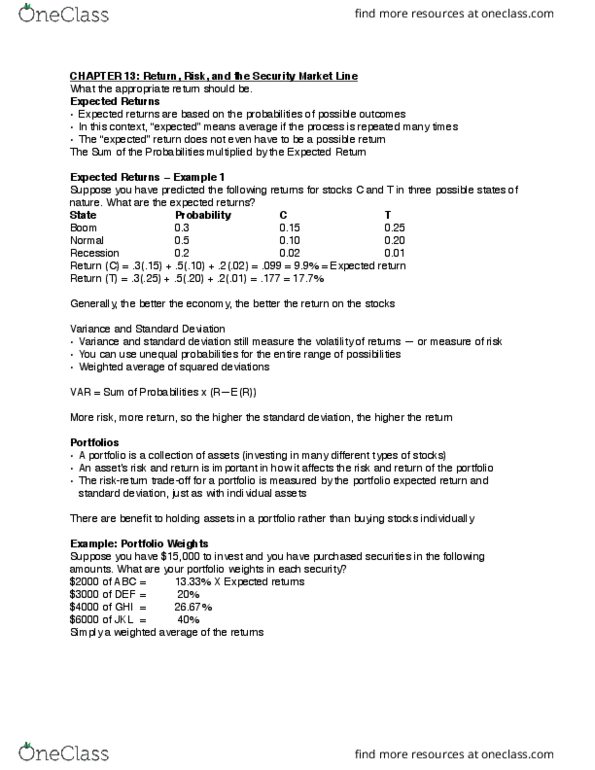

Example: expected returns

• Suppose you have predicted the following returns for stocks C and T in three possible

states of the economy.

What are the expected returns?

State Probability C T

Boom 0.3 15 25

Normal 0.5 10 20

Recession 0.2 2 1

RC = (15*0.3) + (10*0.5) + (2*0.2) = 9.9%

RT = (25*0.3) + (20*0.5) + (1*0.2) = 17.7%

• The three states of the economy still apply to stocks C and T.

• If the risk-free rate (from chapter 12) is 4.15%, what is the risk premium for C & T?

o RC = 9.9%

o RT =17.7%

o Stock C’s risk premium = 5.75%

o Stock T’s risk premium = 13.55%

Variance and standard deviation

• Variance and standard deviation measure the volatility of returns

• Weighted average of squared deviations

å

=

-=

n

i

ii

RERp

1

22

))((σ

Example: variance and standard deviation

What is the variance and standard deviation for C? for T?

State Probability C T

Boom 0.3 15 25

Normal 0.5 10 20

Recession 0.2 2 1

Expected return 9.9% 17.7%

Stock C

2 = .3(15-9.9)2 + .5(10-9.9) 2 + .2(2-9.9) 2 = 20.29

= 4.50%

Stock T

2 = 74.41; = 8.63%

find more resources at oneclass.com

find more resources at oneclass.com

Practice example

Consider the following information:

State Probability ABC, Inc. (%)

Boom .25 15

Normal .50 8

Slowdown .15 4

Recession .10 - 3

What is the expected return, variance and standard deviation?

E(R) = 8.05%

Variance = σ2= 26.7475

σ = √ 26.7475 = 5.17%

Portfolios

• A portfolio is a collection of assets

• An asset’s risk and return are important in how they affect the risk and return of the

portfolio

Example: portfolio weight

Suppose you have $15,000 to invest and you have purchased securities in the following amounts:

What are your portfolio weights in each security?

.133, .200, .267, .400

Portfolio expected return and variance

• Compute the portfolio return for each state:

RP = w1R1 + w2R2 + … + wmRm

• Compute the expected portfolio return, the variance, and the standard deviation using the

same formula as for an individual asset

Example: portfolio variance

Consider the following information:

State Probability A B

Boom .4 30% -5%

Bust .6 -10% 25%

• What is the expected return for asset A?

o Asset A: E(RA) = .4(30) + .6(-10) = 6%

• What is the variance for asset A?

o Variance(A) = .4(30-6)2 + .6(-10-6)2 = 384

• What is the standard deviation for asset A?

o Std. Dev.(A) = 19.6%

Consider the following information:

State Probability A B

Boom .4 30% -5%

Bust .6 -10% 25%

• What is the expected return for asset B?

o Asset B: E(RB) = 13%

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Chapter outline: expected returns and variances, portfolios, announcements, surprises, and expected returns, risk: systematic and unsystematic, diversification and portfolio risk, systematic risk and beta, the security market line, the sml and the cost of capital: a preview. Expected returns: expected returns are based on the probabilities of possible outcomes n. Example: expected returns: suppose you have predicted the following returns for stocks c and t in three possible. Rc = (15*0. 3) + (10*0. 5) + (2*0. 2) = 9. 9% Rt = (25*0. 3) + (20*0. 5) + (1*0. 2) = 17. 7% 1: the three states of the economy still apply to stocks c and t. If the risk-free rate (from chapter 12) is 4. 15%, what is the risk premium for c & t: rc = 9. 9, rt =17. 7, stock c"s risk premium = 5. 75, stock t"s risk premium = 13. 55% Variance and standard deviation: variance and standard deviation measure the volatility of returns, weighted average of squared deviations.