CEE 4303 Lecture Notes - Lecture 6: Accounts Payable, Current Liability, Accounts Receivable

25 Mar 2016

School

Department

Course

Professor

Document Summary

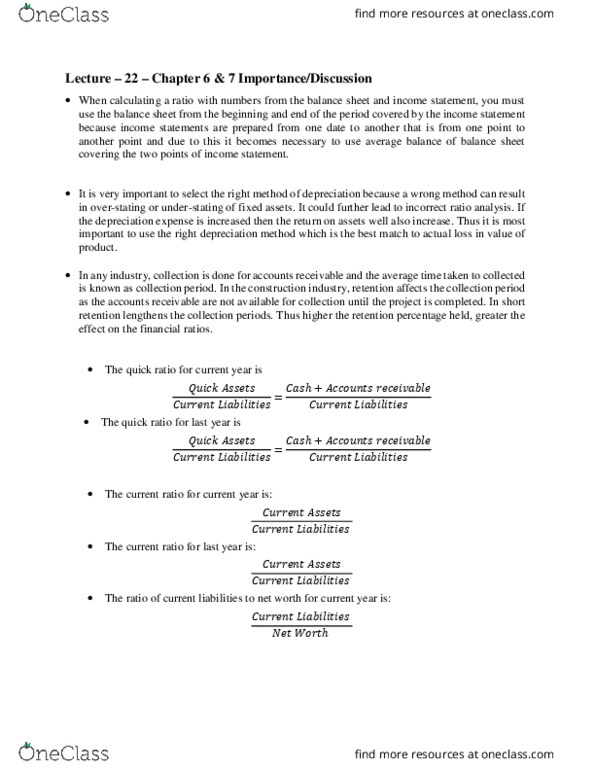

Lecture 6 chapter 6- analysis of financial statements. Financial ratios: affected by, method of depreciation, retention, of financial statements, when comparing items on the balance sheet and income statement, use the average of the balance before and after the period covered by the income statement. Quick ratio: ability to pay current (short-term) liabilities with cash or other near cash assets, quick ratio = (cash + accounts receivable) Current liabilities: accounts receivable-retention should not be included in the accounts receivable, ideal is 1. 00 to 1. Current ratio: ability to use current assets to pay for current liabilities, current ratio = current assets. Current liabilities: ideal is 2. 00 to 1. Debt to equity ratio: risk in the company all creditors are taking compared to the risk the company"s owners are taking, debt to equity = total liabilities/net worth, ideal is less than 2. 00 to 1.