AC 210 Lecture Notes - Lecture 35: Internal Revenue Service, Accounts Receivable, Subledger

5 Jun 2018

School

Department

Course

Professor

Evaluating Accounts Receivable

Business owners know that some customers who receive credit will never pay their

account balances. These uncollectible accounts are also called bad debts. Companies

use two methods to account for bad debts: the direct write‐off method and the

allowance method.

Direct write‐off method. For tax purposes, companies must use the direct write‐off

method, under which bad debts are recognized only after the company is certain the

debt will not be paid. Before determining that an account balance is uncollectible, a

company generally makes several attempts to collect the debt from the customer.

Recognizing the bad debt requires a journal entry that increases a bad debts expense

account and decreases accounts receivable. If a customer named J. Smith fails to pay a

$225 balance, for example, the company records the write‐off by debiting bad debts

expense and crediting accounts receivable from J. Smith.

The Internal Revenue Service permits companies to take a tax deduction for bad debts

only after specific uncollectible accounts have been identified. Unless a company's

uncollectible accounts represent an insignificant percentage of their sales, however,

they may not use the direct write‐off method for financial reporting purposes. Since

several months may pass between the time that a sale occurs and the time that a

company realizes that a customer's account is uncollectible, the matching principle,

which requires that revenues and related expenses be matched in the same accounting

period, would often be violated if the direct write‐off method were used. Therefore, most

companies use the direct write‐off method on their tax returns but use the allowance

method on financial statements.

Allowance method. Under the allowance method, an adjustment is made at the end of

each accounting period to estimate bad debts based on the business activity from that

accounting period. Established companies rely on past experience to estimate

unrealized bad debts, but new companies must rely on published industry averages

until they have sufficient experience to make their own estimates.

find more resources at oneclass.com

find more resources at oneclass.com

The adjusting entry to estimate the expected value of bad debts does not reduce

accounts receivable directly. Accounts receivable is a control account that must have

the same balance as the combined balance of every individual account in the accounts

receivable subsidiary ledger. Since the specific customer accounts that will become

uncollectible are not yet known when the adjusting entry is made, a contra‐asset

account named allowance for bad debts, which is sometimes called allowance for

doubtful accounts, is subtracted from accounts receivable to show the net realizable

value of accounts receivable on the balance sheet.

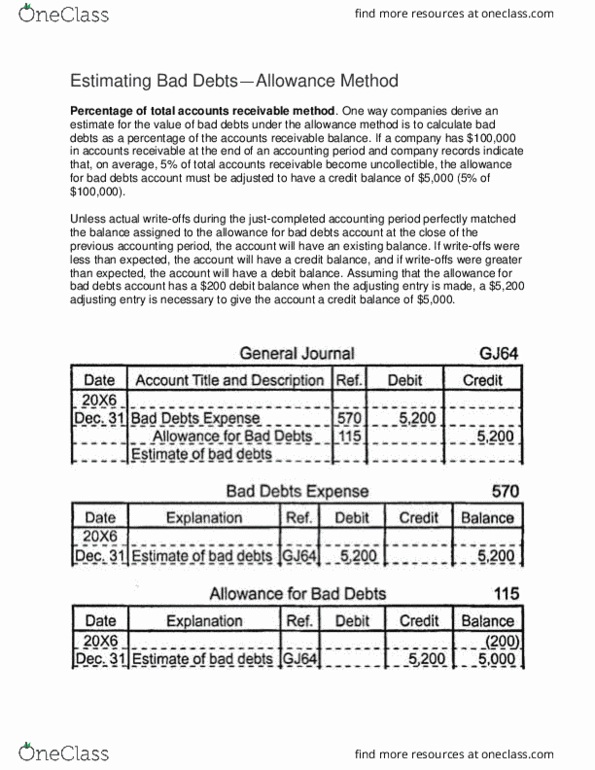

If at the end of its first accounting period a company estimates that $5,000 in accounts

receivable will become uncollectible, the necessary adjusting entry debits bad debts

expense for $5,000 and credits allowance for bad debts for $5,000.

After the entry shown above is made, the accounts receivable subsidiary ledger still

shows the full amount each customer owes, the balance of the control account

(accounts receivable) agrees with the total balance in the subsidiary ledger, the credit

balance in the contra asset account (allowance for bad debts) can be subtracted from

the debit balance in accounts receivable to show the net realizable value of accounts

receivable, and a reasonable estimate of bad debts expense is recognized in the

appropriate accounting period.

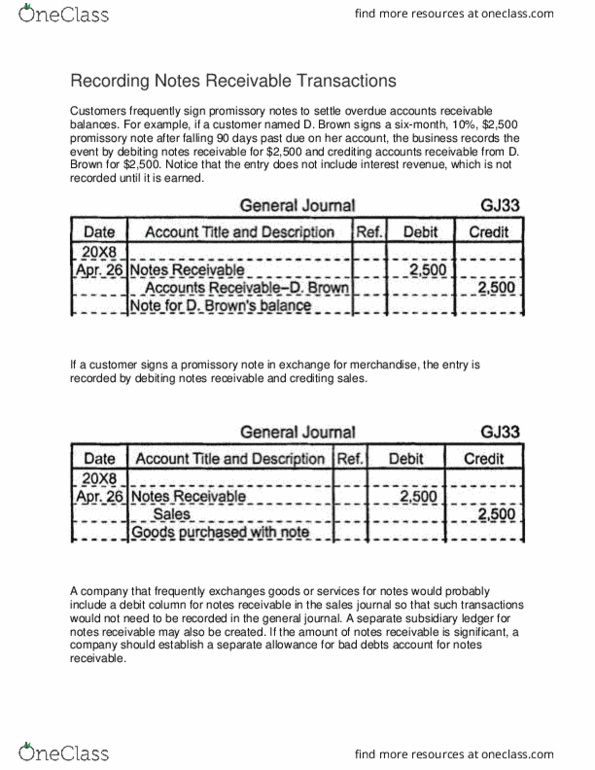

When a specific customer's account is identified as uncollectible, it is written off against

the balance in the allowance for bad debts account. For example, J. Smith's

uncollectible balance of $225 is removed from the books by debiting allowance for bad

debts and crediting accounts receivable. Remember, general journal entries that affect

a control account must be posted to both the control account and the specific account in

the subsidiary ledger.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Business owners know that some customers who receive credit will never pay their account balances. These uncollectible accounts are also called bad debts. Companies use two methods to account for bad debts: the direct write off method and the. For tax purposes, companies must use the direct write off. balance, for example, the company records the write off by debiting bad debts method, under which bad debts are recognized only after the company is certain the debt will not be paid. Before determining that an account balance is uncollectible, a company generally makes several attempts to collect the debt from the customer. Recognizing the bad debt requires a journal entry that increases a bad debts expense account and decreases accounts receivable. If a customer named j. smith fails to pay a expense and crediting accounts receivable from j. smith.