AC 210 Lecture Notes - Lecture 43: Consignor, Consignee, Cash Flow

5 Jun 2018

School

Department

Course

Professor

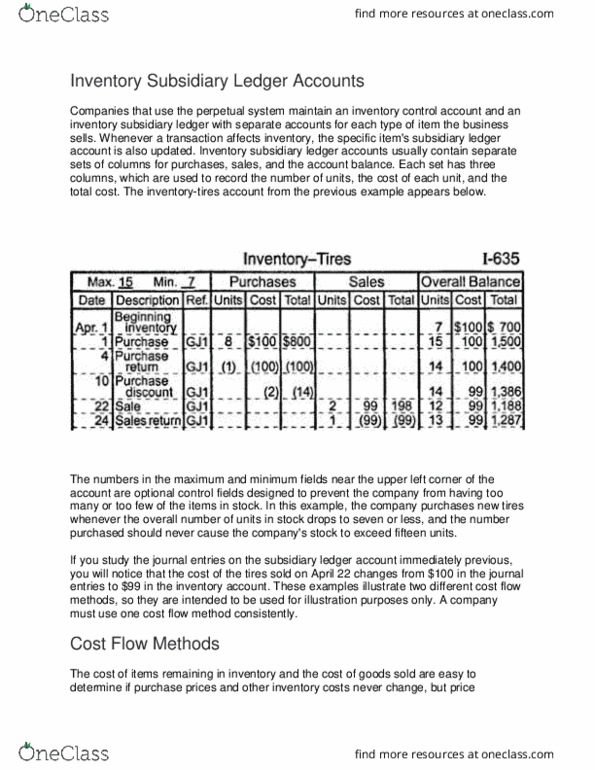

Determining Inventory Levels

Merchandising and manufacturing companies keep an inventory of goods held for sale.

Management is responsible for determining and maintaining the proper level of goods in

inventory. If inventory contains too few items, sales may be missed. If inventory

contains too many items, the business pays unnecessary amounts to warehouse,

secure, and insure the items, and the company's cash flow becomes one sided‐cash

flows out to purchase inventory but cash does not flow in from sales.

Companies take physical inventories to count how many (or measure how much) of

each item the company owns. Inventory is easier to count when sales and deliveries are

not occurring, so many companies take inventory when the business is closed.

Taking a physical inventory involves internal control principles. Examples of these

internal control principles include the following:

• Segregation of duties. Specific items should be counted by employees who do

not have custody of the items.

• Proper authorization. Managers are responsible for assigning each employee

to a specific set of inventory tasks. In addition, employees who help take

inventory are responsible for verifying the contents of boxes, barrels, and other

containers.

• Adequate documents and records. Prenumbered count sheets are provided to

all employees involved in taking inventory. These count sheets provide evidence

to support reported inventory levels and, when signed, show exactly who is

responsible for the information they include.

• Physical controls. Access to inventory should be limited until the physical

inventory is completed. If the company plans to ship inventory items during a

physical inventory, these items should be placed in a separate area. Similarly, if

the company receives inventory items during a physical inventory, these items

should be kept in a designated area and counted separately.

• Independent checks on performance. After the employees finish counting, a

supervisor should verify that all items have been counted and that none have

been counted twice. Some companies use a second counter to check the first

counter's results.

Consigned merchandise. Consigned merchandise is merchandise sold on behalf of

another company or individual, who retains title to it. Although the seller (consignee) of

the merchandise displays the items, only the owner (consignor) includes the items in

inventory. Therefore, companies that sell goods on consignment must be careful to

exclude from inventory those items provided by consignors.

Goods in transit. Goods in transit must be included in either the seller's or the buyer's

inventory. When merchandise is shipped FOB (free on board) shipping point, the

purchaser pays the shipping fees and gains title to the merchandise once it is shipped.

Therefore, the merchandise must be included in the purchaser's inventory even if the

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Merchandising and manufacturing companies keep an inventory of goods held for sale. Management is responsible for determining and maintaining the proper level of goods in inventory. If inventory contains too few items, sales may be missed. If inventory contains too many items, the business pays unnecessary amounts to warehouse, secure, and insure the items, and the company"s cash flow becomes one sided cash flows out to purchase inventory but cash does not flow in from sales. Companies take physical inventories to count how many (or measure how much) of each item the company owns. Inventory is easier to count when sales and deliveries are not occurring, so many companies take inventory when the business is closed. Taking a physical inventory involves internal control principles. Examples of these internal control principles include the following: segregation of duties. Specific items should be counted by employees who do not have custody of the items: proper authorization.