ECON 161A Lecture Notes - Lecture 2: Loan

Document Summary

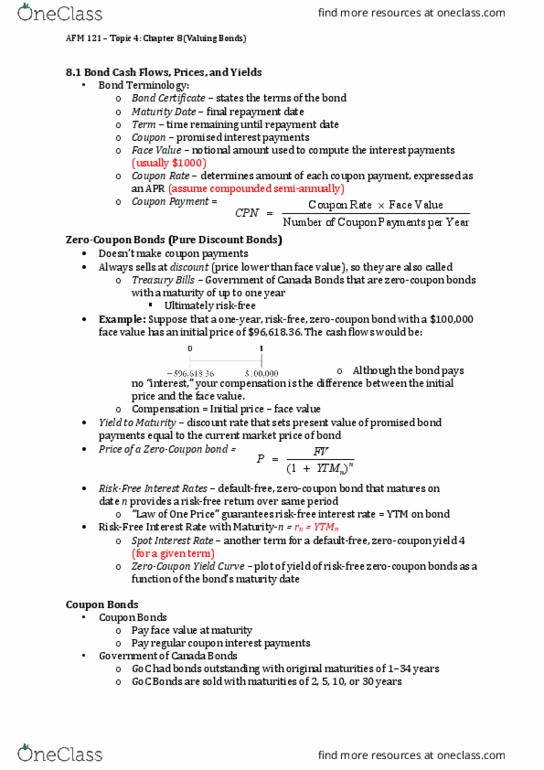

Def: interest rate that equates pv of a payment stream with the value or price today. Short term bond that doesn"t make periodic payments, it only pays its face value. Sells at market price and pays face value sometime in the future. Zero-coupon means there are no periodic interest payments. A single one time payment, the yield to maturity is defined by: Pzb = face value/(1+i/m) m = 12/months to maturity (if six month bond, m = 2) Pzb = what people are paying for it today i = annualized interest rate. Bond issuer decides the face value, the market decides the price. No individual person who decides what the interest rate on the debt is; not that the government is announcing the interest rate, we back out the interest rate based on the transactions made. Government says we want to borrow some funds, we"ll give 100,000 and pay it back in six months.