FINC314 Lecture Notes - Lecture 8: Time Series, Investment Management, Kurtosis

10 Feb 2020

School

Department

Course

Professor

Document Summary

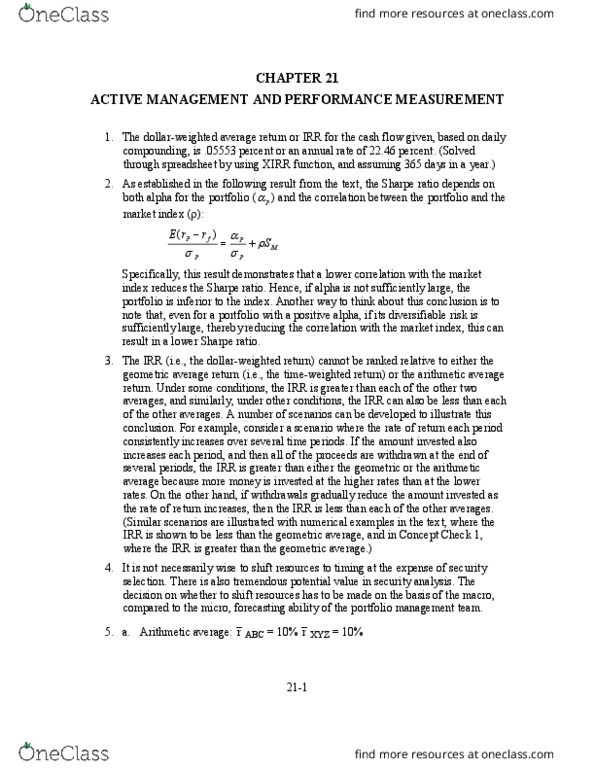

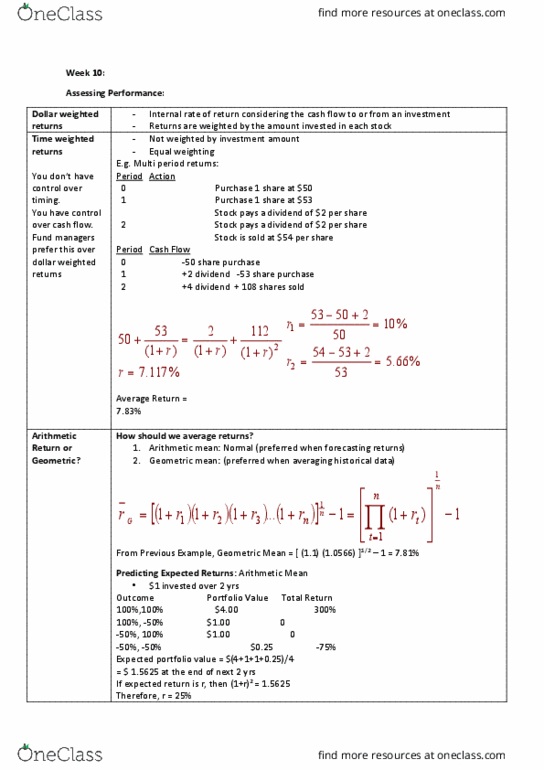

This note expands upon its predecessor by addressing time series analysis, normality, and deviation (skewness and kurtosis). When working with historical data, each of the observed holding period returns are assumed to have equal probabilities. Such average returns can be measured using either a simple arithmetic average or a slightly more complex geometric average. Starting with the arithmetic average rate of return: Practitioners of investments call g the time-weighted (as opposed to dollar-weighted) average return to emphasize that each past return receives an equal weight in the process of averaging. This distinction (which is not between arithmetic and geometric average returns) is important because investment managers often experience significant changes in funds under management as investors purchase or redeem shares. Naturally, rates of return obtained during periods when the fund is large produce larger dollar profits than rates obtained when the fund is small.