ACG 2021 Lecture Notes - Lecture 22: Retained Earnings, Issued Shares, Stock Split

8 Apr 2018

School

Department

Course

Professor

Document Summary

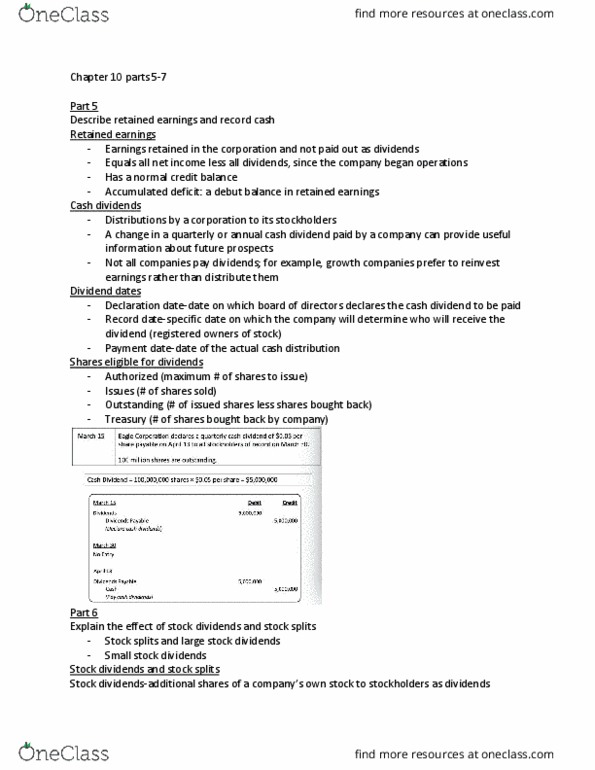

Account for retained earnings: net income increases, less net losses, less declared dividends. Accumulated over corporation"s lifetime: distribution by a corporation to its stockholders, usually based on earnings, usually take one of three forms, cash, stock, noncash assets. Cash dividends: company must have both, enough retained earnings to declare the dividend, enough cash to pay the dividend, board of directors has authority to declare a dividend, company not obligated to pay dividend until declared. Dividends dates: declaration date now a liability of the company, debit retained earnings, credit dividends payable, date of record no journal entry, payment date debit dividends payable, credit cash. Dividends on preferred stock: paid dividends before common stockholders, stated as a percent of par value or a dollar amount per share, may be cumulative, passed dividends are owed to preferred shareholders, in arrears, almost debt. Stock dividends: proportional distribution of stock to shareholders.