ACCTG 2600 Lecture Notes - Lecture 6: Fiduciary, Income Statement, Financial Statement

6 Feb 2017

School

Department

Course

Professor

Document Summary

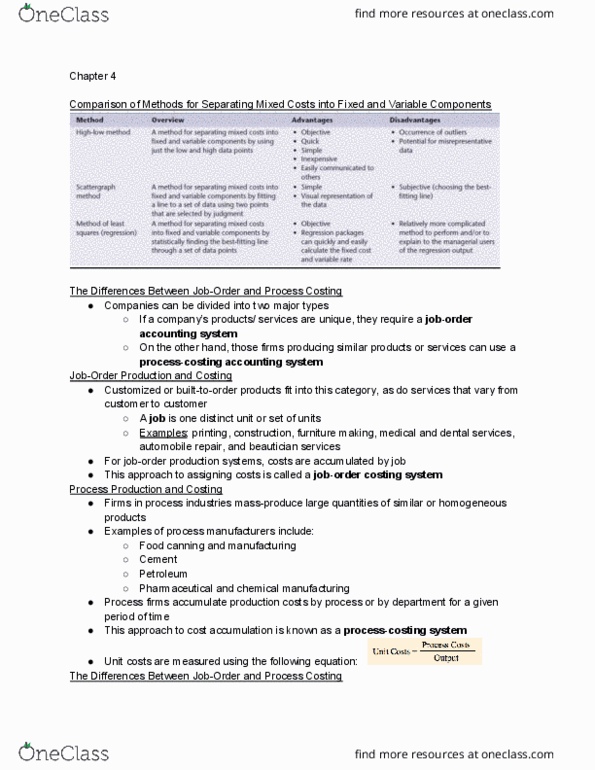

Those firms producing similar products or services can use a process-costing accounting system. On the other hand, if a company"s products/ services are unique, they require a job-order accounting system. When each job you are working on is specific: characteristics of the job-order environment, customized or built-to-order products fit into this category, as do services that vary from customer to customer. A job is one distinct unit or set of units. Pharmaceutical and chemical manufacturing: process production and costing, process firms accumulate production costs by process or by department for a given period of time, unit costs are measured using the following equation: Unit costs = process costs output: the differences between job-order and process costing. Defining overhead costs: overhead items do not have the direct relationship with units produced that direct materials and direct labor do. Uneven overhead costs: many overhead costs are not incurred uniformly throughout the year.