BUSI 1011 Lecture Notes - Lecture 4: Payback Period, Capital Budgeting, Net Profit

Document Summary

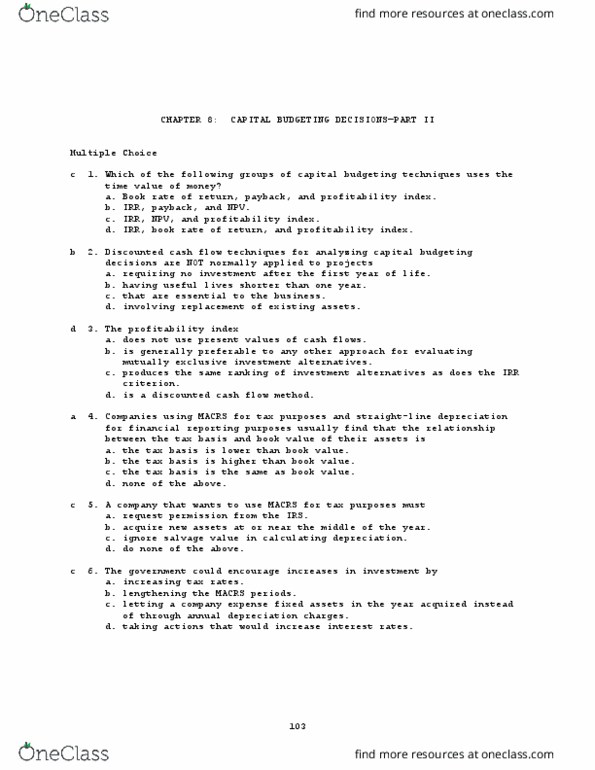

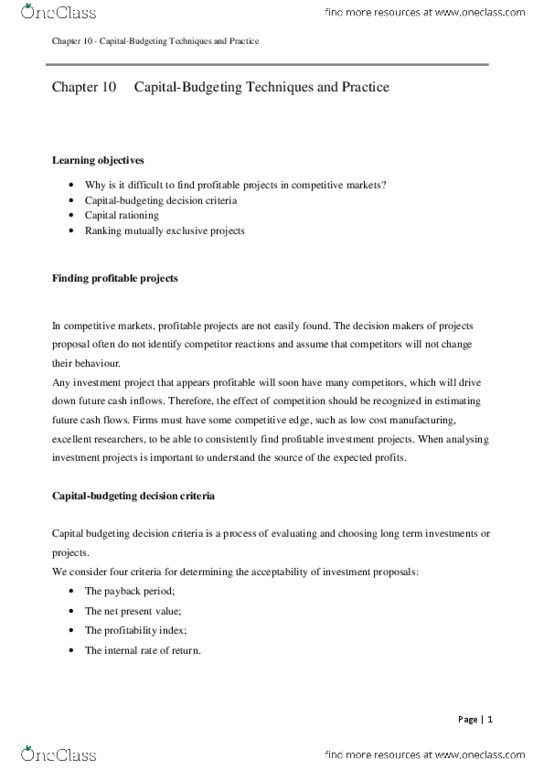

Capital budgeting (or investment appraisal) is the planning process used to determine whether an organisation"s long term investments such as new machinery, replacement machinery, new plants, new products, and research development projects are worth pursuing. Payback period is the time duration required to recoup the investment committed to a project. Here payback period is the time when cumulative cash inflows are equal to the outflows: the payback period is stated in terms of years. This can be stated in terms of percentage also. In the case of two mutually exclusive projects, the one with a lower payback period is accepted, when the respective payback periods are less than or equivalent to the stipulated payback period. Accounting rate of return is the rate arrived at by expressing the average annual net profit (after tax) as given in the income statement as a percentage of the total investment or average investment. The accounting rate of return is based on accounting profits.