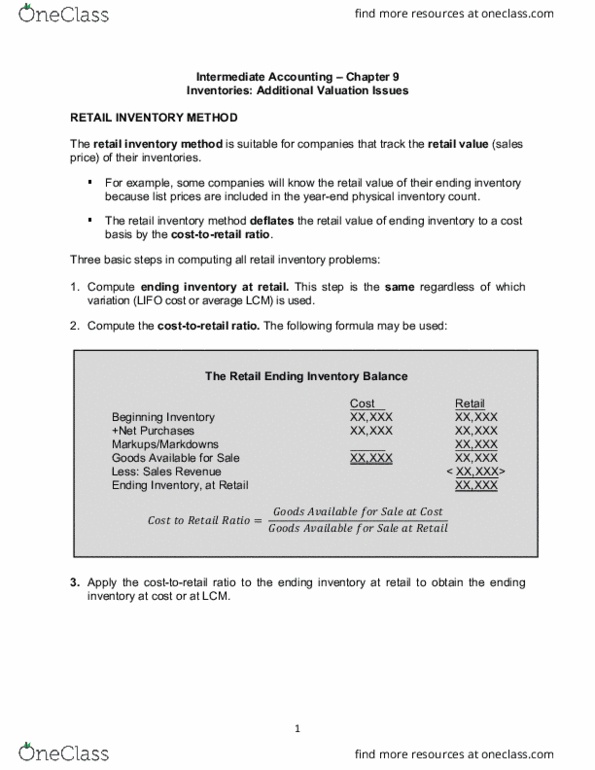

The following independent situations occurred at the end of Year 2 and require an inventory report in the year-end financial statements. The dollar amounts provided in the table below are on a per-unit basis. In Situation 5., assume that the company is applying IFRS.

Situation Historical cost Estimated selling price Cost of completion Cost of disposal Current replacement cost Normal profit margin 1. $60 $70 -- $5 $55 $7 2. $50 $80 $20 $6 $53 $3 3. $45 $44 $3 $2 $40 $4 4. $29 $40 $4 $6 $28 $5 5. $100 $110 $15 $5 $82 $5

Select from the option list provided the appropriate measurement attributes for reporting inventory in the year-end financial statements. Each choice may be used once, more than once, or not at all.

Situation Answer 1. The company accounts for its inventory using the LIFO method. 2. The company accounts for its inventory using the average-cost method. 3. The company accounts for its inventory using the FIFO method. 4. The company accounts for its inventory using the LIFO method. 5. (Under IFRS)

Answer Choices: ( Historical Cost, Net Realizable Value, Net Realizable Value minus Normal Profit Margin, Current Replacement Cost)

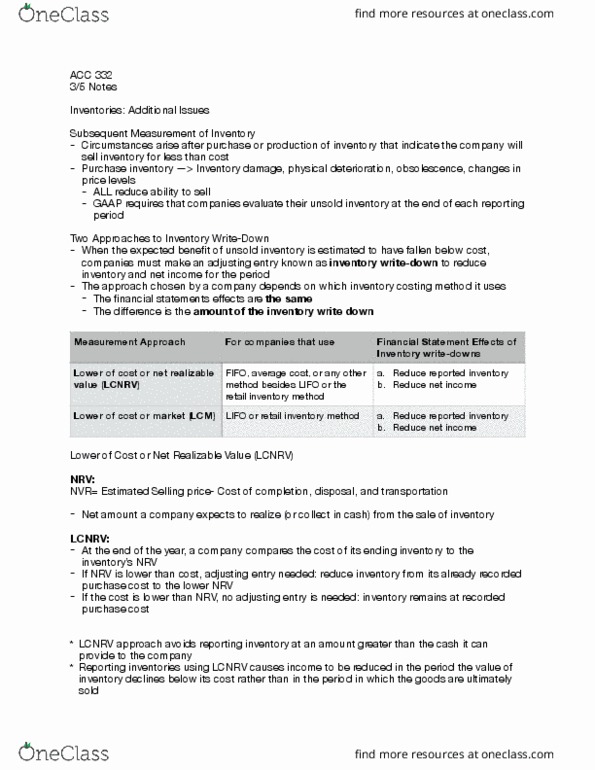

The following independent situations occurred at the end of Year 2 and require an inventory report in the year-end financial statements. The dollar amounts provided in the table below are on a per-unit basis. In Situation 5., assume that the company is applying IFRS.

| Situation | Historical cost | Estimated selling price | Cost of completion | Cost of disposal | Current replacement cost | Normal profit margin |

| 1. | $60 | $70 | -- | $5 | $55 | $7 |

| 2. | $50 | $80 | $20 | $6 | $53 | $3 |

| 3. | $45 | $44 | $3 | $2 | $40 | $4 |

| 4. | $29 | $40 | $4 | $6 | $28 | $5 |

| 5. | $100 | $110 | $15 | $5 | $82 | $5 |

Select from the option list provided the appropriate measurement attributes for reporting inventory in the year-end financial statements. Each choice may be used once, more than once, or not at all.

| Situation | Answer |

| 1. The company accounts for its inventory using the LIFO method. | |

| 2. The company accounts for its inventory using the average-cost method. | |

| 3. The company accounts for its inventory using the FIFO method. | |

| 4. The company accounts for its inventory using the LIFO method. | |

| 5. (Under IFRS) Answer Choices: ( Historical Cost, Net Realizable Value, Net Realizable Value minus Normal Profit Margin, Current Replacement Cost) |

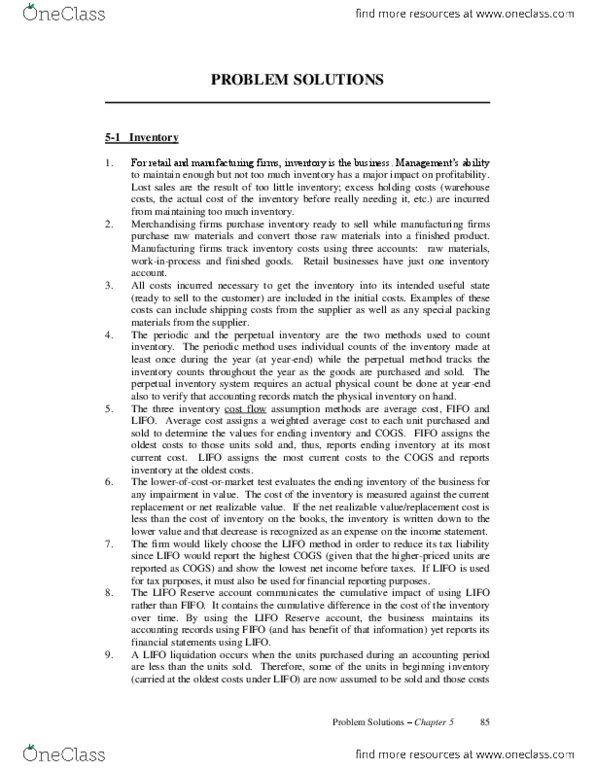

Related questions

E7-6 Analyzing and Interpreting the Financial Statement Effects of Periodic FIFO, LIFO, and Weighted Average Cost [LO 7-3]

| Orion Iron Corp. tracks the number of units purchased and sold throughout each year but applies its inventory costing method at the end of the year, as if it uses a periodic inventory system. Assume its accounting records provided the following information at the end of the annual accounting period, December 31. |

| Transactions | Units | Unit Cost | ||||

| a. Inventory, Beginning | 350 | $ | 14 | |||

| For the year: | ||||||

| b. Purchase, April 11 | 950 | 12 | ||||

| c. Purchase, June 1 | 700 | 15 | ||||

| d. Sale, May 1 (sold for $42 per unit) | 350 | |||||

| e. Sale, July 3 (sold for $42 per unit) | 610 | |||||

| f. Operating expenses (excluding income tax expense), $18,000 | ||||||

| Required: |

| 1. | Calculate the number and cost of goods available for sale. |

| 2. | Calculate the number of units in ending inventory. |

| 3. | Compute the cost of ending inventory and cost of goods sold under (a) FIFO, (b) LIFO, and (c) weighted average cost. (Do not round intermediate calculations. Round your final answers to the nearest dollar amount.) |

| 4. | Prepare an Income Statement that shows the FIFO method, LIFO method and weighted average method. |

| 6. | Which inventory costing method minimizes income taxes? | ||||||

|