SMG SM 131 Study Guide - Final Guide: Ethical Movement, Insider Trading, Stakeholder Management

11 Dec 2018

School

Department

Course

Professor

Exam #2 Study Guide

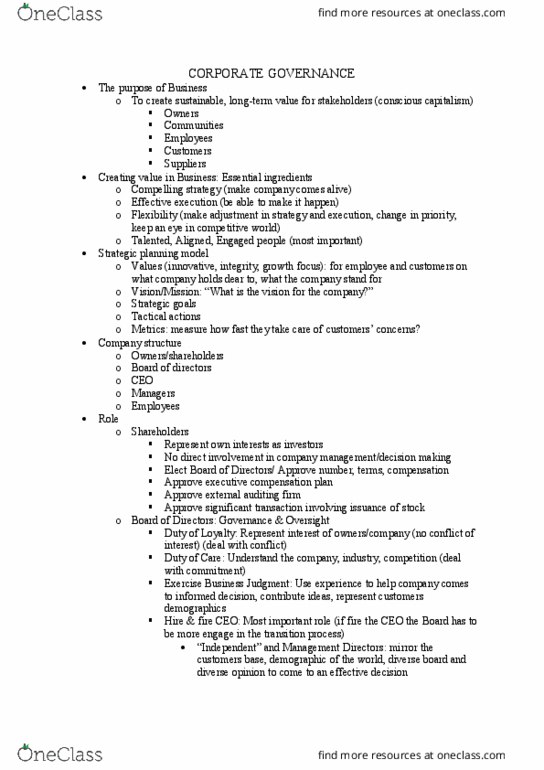

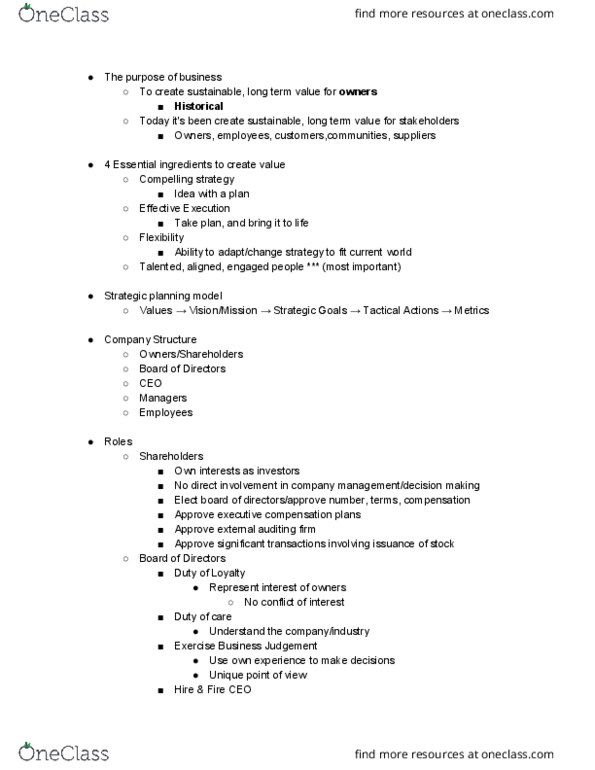

Corporate Governance

o Purpose of Business

To create sustainable, long-term value for stakeholders including, owners,

employees, customers, communities and suppliers

o Public Company Structure

Owners/shareholders

Board of directors

CEO

Managers

Employees

o Role of Shareholders

No direct involvement in decision-making

Elects the Board, approves terms and executive compensation

Approves external auditors and significant stock transactions

o Role of the Board of Directors

Duty of Loyalty – represent interest of owners

Duty of Care – Understand the companies needs and do what’s best for it

Exercise business judgement – Use experience to make proper decisions

for the company that are in the best interest – diversity is important

Hire and fire CEO

o Role of the CEO

Run the company

Establish strategy

Role model for employees

Sets financial and non-financial goals

o Line and Staff Employees

Lone roles face the customers on a day to day basis

o Problems in Corporate Governance

Board independence

Insiders v.s Outside (independent/nonemployees)

Compensation

CRO pay-firm performance relationship / excessive pay

Exec. Retirement plans and exit packages (golden parachute)

Outside director compensation (avg. $250,000)

Transparency

Insider trading

o Improving Corporate Governance

Enablers of Ethical Culture = People, Processes, and Measurements.

Legislative Measures – Sarbanes Oxley and Dodd Frank

Dodd Frank – disclosure of conflicts, golden parachutes,

independence of directors, CRO compensation (say-on-pay)

Sarbanes Oxley – independent auditor who does not consult with

firm, CEO & CFO must certify financial reports

Change in board of directors

Diversity/outside directors

Board committee action

Nominate, audit, compensation, CSR

Standards, training and monitoring.

o Legitimacy of Corporate Governance

U.S. uses a Anglo-American model with “shareholder primacy”

Shareholders (own)-> Board (govern)-> Management (run)-> Employees

(work)

Agency problem – Management is supposed to be an agent of the owners,

but they have power/control that can be used against owner’s best interest.

Business Forms

o Sole Proprietorship

72% of all business forms

Owners by one person

Unlimited liability

Pass-through taxation (taxed at personal level)

o Partnership

Two or more owners

Each partner responsible for profits, taxes and unlimited liability

Pass-through taxation (taxed at personal level)

o C Corporation

Separate legal entity for tax and liability purposes

Owners not personally liable

Corporate entity is responsible for taxes and debts

Higher tax rate – 21% at federal level and state taxes

Double taxes (business and personal)

High ability to raise money

Can go public

o S Corporation

Tax status of a sole proprietorship/partnership

Limited liability of a C corporation

> 100 shareholders

One form of stock

Pass through taxation (taxed at personal level only)

o Limited Liability Company (LLC)

Tax structure of a partnership

Limited liability of a C corporation

Loses tax status If it goes public (must pay both types and pay backed

taxes)

Corporation can be a partner of an LLC

o Social Benefit Corporation

Created under state law in 31 states

Goal is to make a profit and pursue a social mission

Benefits director and fiduciary duties owed to shareholders

Social mission > profit

Must publish yearly social and environmental impact report

o B Corp

Any for-profit entity given a certification from B-Lab

Accounting

o Accounting

Recording, classifying, summarizing and interpreting of financial events

and transactions in an organization to provide interested parties needed

financial information.

Employees, owners, creditors, unions, investors, and the government will

make use of a firms accounting information.

o Balance sheet

Assets, liabilities and equity

o Income statement

Revenues, expenses and profit (net income)

o Statement of cash flows

Cash inflow (revenue), cash outflow (cost of operation/Production) and

cash on hand

5 Working Areas of Accounting

o Financial Accounting

Provides financial information for people outside organization.

Profitability, debt and performance

o Managerial Accounting

Provides financial information for managers inside the organization to

assist in decision making

Cost of production/marketing

Preparation and control of budget

Minimizing tax liability

o Auditing

Reviews and evaluates the information used to prepare a company’s

financial statements

Independent auditors (Sarbanes-Oxley)

Internal audits (accountants within firm)

o Tax

Tax accountant are trained in tax law and are responsible for preparing tax

returns and developing strategies

Document Summary

To create sustainable, long-term value for stakeholders including, owners, employees, customers, communities and suppliers: public company structure. Elects the board, approves terms and executive compensation. Approves external auditors and significant stock transactions: role of the board of directors. Duty of loyalty represent interest of owners. Duty of care understand the companies needs and do what"s best for it. Exercise business judgement use experience to make proper decisions for the company that are in the best interest diversity is important. Hire and fire ceo: role of the ceo. Sets financial and non-financial goals: line and staff employees. Lone roles face the customers on a day to day basis: problems in corporate governance. Cro pay-firm performance relationship / excessive pay. Enablers of ethical culture = people, processes, and measurements. Legislative measures sarbanes oxley and dodd frank. Dodd frank disclosure of conflicts, golden parachutes, independence of directors, cro compensation (say-on-pay)