BUS-F 446 Study Guide - Midterm Guide: Cash Flow, Risk-Adjusted Return On Capital, Reserve Requirement

Chapter Notations

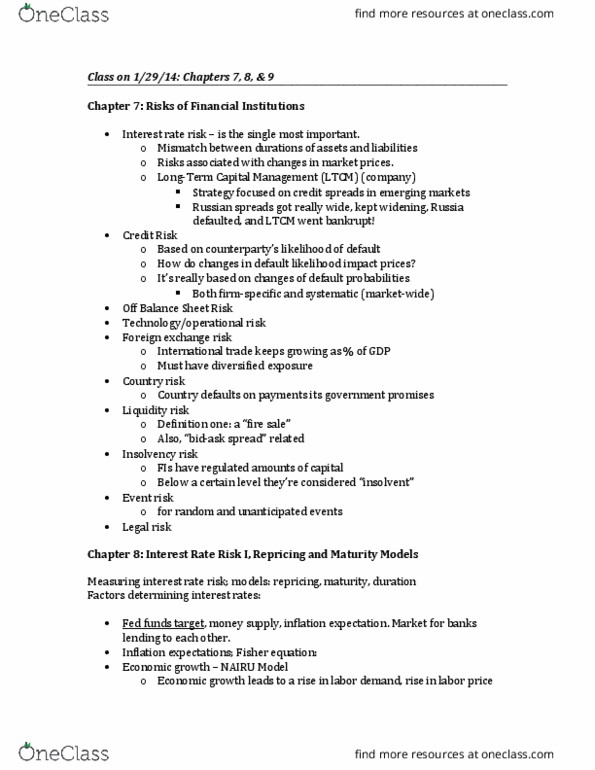

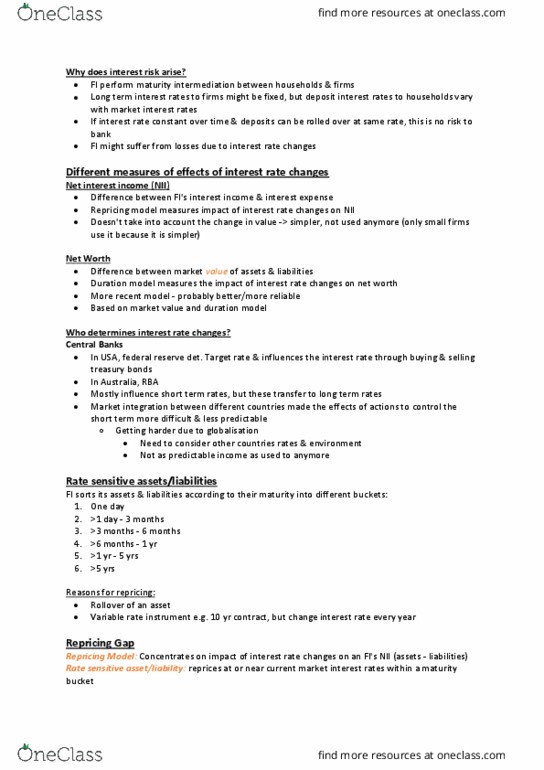

Chapter Eight: Interest Rate Risk I

NII = change in net interest income in the ith maturity bucket

GAP (CGAP) = the dollar size of the gap between the book value of rate sensitive assets and liabilities in

maturity bucket i

Ri = yield to maturity on security i

RSA = an asset on the balance sheet that is repriced at or near current market interest rates within a

maturity bucket.

RSL= a liability on the balance sheet that is repriced at or near current market interest rates within a

maturity bucket.

PtB = the present value of the cash flows on a bond

F = the face value of a security (e.g., a bond) to be paid on maturity

C= dollar amount of a coupon payment on a bond paid at a stated rate (e.g., 10 percent) of the face value

PtD = the present value of the cash flows on a deposit

Mi = the weighted-average maturity of an FI’s assets (liabilities), I = A or L

Wij = the importance of each asset (liability) in the asset (liability) portfolio as measured by the market

value of that asset (liability) position relative to the market value of all the assets (liabilities)

Mij = the maturity of the jth asset (or liability), j = 1...n

A = the market value of an FI’s assets

L = the market value of an FI’s liabilities

E = the net worth or true equity value of an FI

maturity gap = MA - ML,

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Nii = change in net interest income in the ith maturity bucket. Gap (cgap) = the dollar size of the gap between the book value of rate sensitive assets and liabilities in maturity bucket i. Rsa = an asset on the balance sheet that is repriced at or near current market interest rates within a maturity bucket. Rsl= a liability on the balance sheet that is repriced at or near current market interest rates within a maturity bucket. B = the present value of the cash flows on a bond. D = the present value of the cash flows on a deposit. Mi = the weighted-average maturity of an fi"s assets (liabilities), i = a or l. Wij = the importance of each asset (liability) in the asset (liability) portfolio as measured by the market value of that asset (liability) position relative to the market value of all the assets (liabilities)