FINS1612 Chapter Notes - Chapter 13: Financial Market Participants, Future Interest, Economic Indicator

1

Financial Institutions, Instruments and Markets

8th edition

Instructor's Resource Manual

Christopher Viney and Peter Phillips

Chapter 13

An introduction to interest rate determination and forecasting

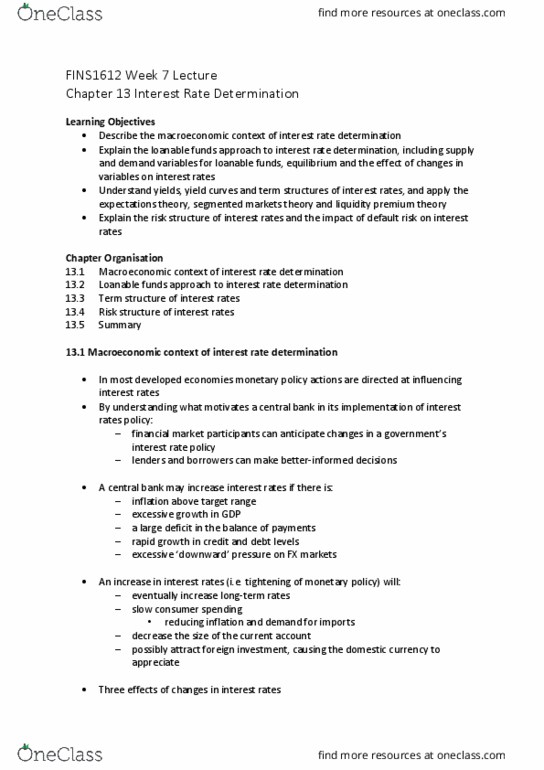

Learning objective 1: Describe at a macroeconomic level how the liquidity effect, the income

effect and the inflation effect influence the determination of interest rates

• In forming a view on the future direction of interest rates, it is necessary to recognise that

changes in monetary policy settings are likely to affect the state of the economy, which in

turn affects interest rates generally.

• Within the macroeconomic context, these progressive changes are referred to as the liquidity

effect, the income effect and the inflation effect on interest rates.

• The liquidity effect derives from monetary-policy-induced changes to in interest rates such as

an increase in interest rates due to a reduction in liquidity in financial system.

• As interest rates rise, economic activity will slow and incomes fall. This will cause interest

rates to begin to ease or fall. This is the income effect.

• The income effect will reduce upward pressures on prices as the economy slows and there is

likely to be a reduction in the rate of inflation, thus causing interest rates to fall further (the

inflation effect).

• Therefore, when trying to forecast the state of an economy and future interest rates, policy

makers, economists and financial market participants consider a range of economic

indicators, such as the level of employment, productivity and housing approvals.

find more resources at oneclass.com

find more resources at oneclass.com

2

• Indicators may be described as leading, coincident and lagging indicators of future economic

activity.

Learning objective 2: Explain the loanable funds approach to interest rate determination,

highlighting variables that affect the demand and supply for loanable funds. Consider the

effects of changes in those variables on interest rate equilibrium

• A disciplined approach to forming a view on the future direction of interest rate movements

is provided by the loanable funds approach.

• Typically, the demand for loanable funds within the financial system originates from the

business sector and the government sector and is represented by a downward sloping demand

curve.

• The supply of loanable funds derives from the savings of the household sector, changes in

the money supply and the hoarding or dishoarding that takes place in response to changes in

interest rates. This is represented by an upward sloping supply curve.

• Under the loanable funds approach, the prevailing rate of interest is determined by the

intersection of the demand and supply curves; the equilibrium point.

• Factors that cause the demand or supply curves to change will result in a change in the rate of

interest.

• While the framework is useful in identifying impacts on interest rates, its major shortcoming

is that the supply and demand curves are interdependent. For example, changes in the level of

economic activity or inflationary expectations may impact both the demand side and the

supply side of the curves. As a result, it is not possible to determine a unique equilibrium

interest rate.

• Another shortcoming of the loanable funds approach is that it addresses interest rate

determination as if only one interest rate exists at a particular time. This is clearly not the

case in reality. At any point there are many rates of interest.

• The differences in rates reflect the different terms to maturity of instruments and the credit

risk of a borrower. Differences between the interest rates on instruments of similar risk, but

with different terms to maturity, are explained by theories of the term structure of interest

find more resources at oneclass.com

find more resources at oneclass.com

3

rates.

Learning objective 3: Understand interest rate yields and the shape of various yield curves.

Apply the expectations theory, the segmented markets theory and the liquidity premium theory

within the context of the term structure of interest rates

• The term structure of interest rates is represented by a yield curve.

• The yield is the rate of return on debt instruments and a yield curve graphs the relationship

between interest rates and the term to maturity of debt instruments in the same risk class.

• The shape of the yield curve may be normal, inverse or humped.

• A normal yield curve is an upward-sloping curve where there is an expectation that short-term

interest rates in the future will rise. A steeper normal curve indicates an expectation that there

will be larger interest rate increases in the future.

• An inverse yield curve is a downward-sloping curve, typically induced through a tightening of

monetary policy by a central bank. It indicates that current short-term interest rates are high, but

that there is an expectation that in the future there will be an easing of monetary policy and short-

term interest rates will begin to fall.

• The expectations theory argues that, in an efficient market, interest rates on longer-term

instruments are determined by two factors: the current short-term interest rate and the short-

term rates that are expected to prevail over the longer term.

• The segmented markets theory provides a further explanation of the shape of the yield curve. It

contends that investors do not view bonds of different maturities as being close substitutes. It is

argued that investors will have a preference to accumulate a majority of securities in an

investment portfolio that have predominantly short-term, medium-term or long-term maturities.

The implication is that the shape of the yield curve is explained by the demand and supply

conditions that are evident in the various maturity segments of the overall yield curve.

• However, the arguments of the segmented markets theory ignore the role of market arbitrage and

speculation in ensuring that the yield curve over the maturity spectrum remains in equilibrium.

Also, in a modern financial market, risk managers are able to hedge such risk using synthetic risk

management products such as derivatives. As a result, the forecasts derived from the segmented

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

An introduction to interest rate determination and forecasting. Learning objective 1: describe at a macroeconomic level how the liquidity effect, the income effect and the inflation effect influence the determination of interest rates. This will cause interest rates to begin to ease or fall. Indicators may be described as leading, coincident and lagging indicators of future economic activity. Learning objective 2: explain the loanable funds approach to interest rate determination, highlighting variables that affect the demand and supply for loanable funds. For example, changes in the level of economic activity or inflationary expectations may impact both the demand side and the supply side of the curves. This is clearly not the case in reality. At any point there are many rates of interest: the differences in rates reflect the different terms to maturity of instruments and the credit risk of a borrower.