ACTG 2P12 Chapter Notes - Chapter 7: Total Absorption Costing, Expense, Lean Manufacturing

13 Mar 2017

School

Department

Course

Professor

Document Summary

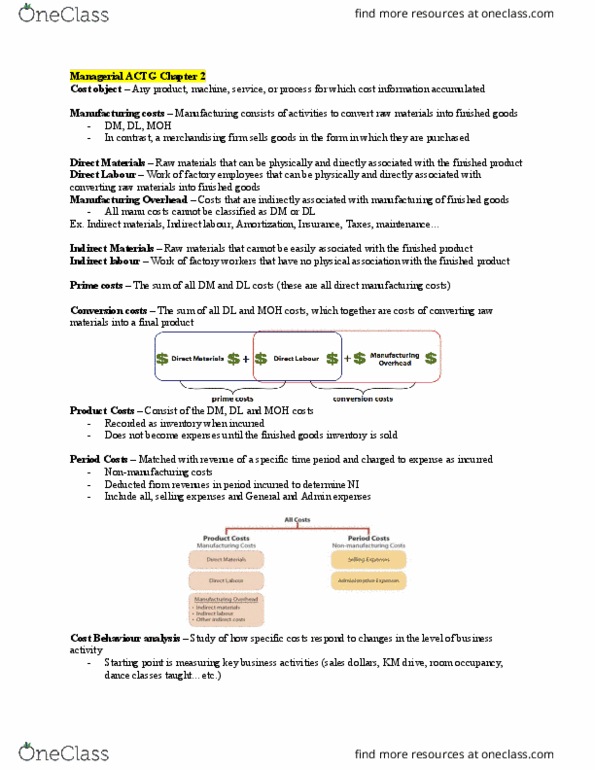

Inventory costing methods: absorption costing, all manufacturing costs are charged to (absorbed by) the product, variable costing, only direct materials, direct labour, and variable manufacturing overhead costs are considered product costs. Product cost manufacturing overhead period cost. Fixed manufacturing overhead (,000 / 30,000 units produced) Cost of goods manufactured (30,000 units x ) Cost of goods sold (20,000 units x ) There is one primary difference between variable and absorption costing: under variable costing, the fixed manufacturing overhead is charged as an expense in the current period. Variable selling and administrative expenses (2000 units x ) In this case, there is no increase in ending inventory, so fixed overhead costs of the current period are not deferred to future periods through the ending inventory. Fix-it selling price: fix-it selling price: per unit. Units: produced 30,000; sold 20,000; beginning inventory 0. Variable unit costs: manufacturing (direct materials , direct labour , variable overhead )