FINA 385 Chapter 18: Bodie_7e_18 .doc

Get access

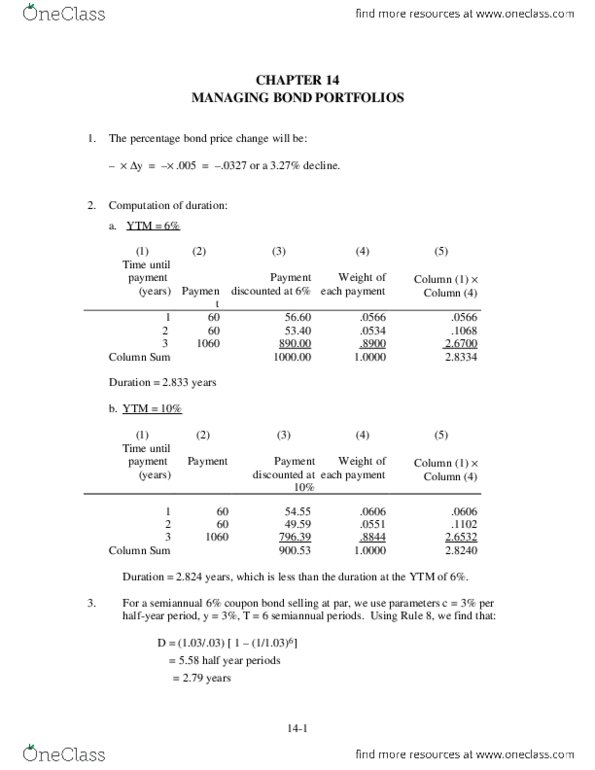

Related Documents

Related Questions

Consider the following option portfolio: You write a January 2012 expiration call option on IBM with exercise price $168, and the price of the call option is $8.93. You also write a January expiration IBM put option with exercise price $163, the price of the put option is $10.85.

Instructions: for parts a, b, and c, enter your answer as a decimal rounded to the nearest cent.

a. What will be the profit/loss on this position if IBM is selling at $157 on the option expiration date? $

b. What will be the profit/loss on this position if IBM is selling at $172 on the option expiration date? $

c. At what two stock prices will you just break even on your investment (i.e., zero net profit)?

For the put, this requires that: $

For the call this requires that: $

d. What kind of âbetâ is this investor making; that is, what must this investor believe about IBMâs stock price in order to justify the position?

| betting that the IBM stock price will go up. | |

| betting that the IBM stock price will go down. | |

| betting that the IBM stock price will have low volatility. | |

| betting that the IBM stock price will have high volatility. |