COMMERCE 1AA3 Chapter Notes - Chapter 12&4: Accrual, Income Statement, Financial Statement

28 Oct 2016

School

Department

Course

Professor

Document Summary

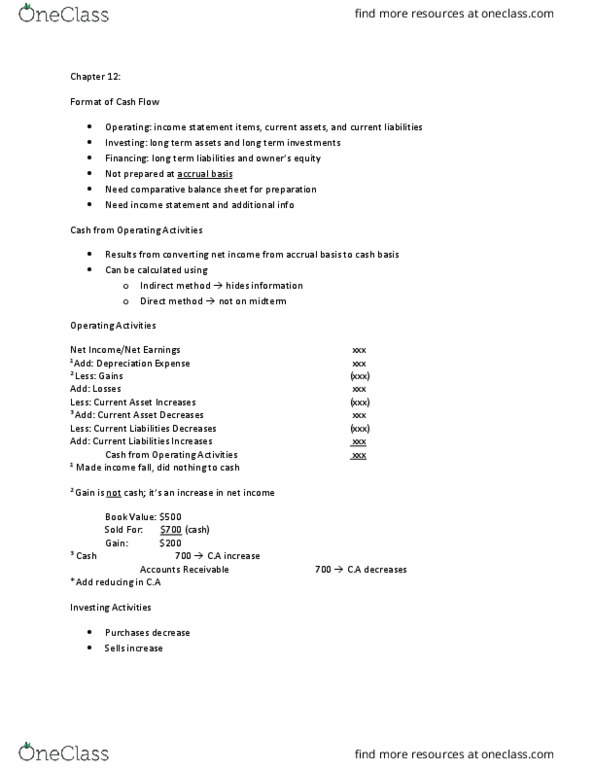

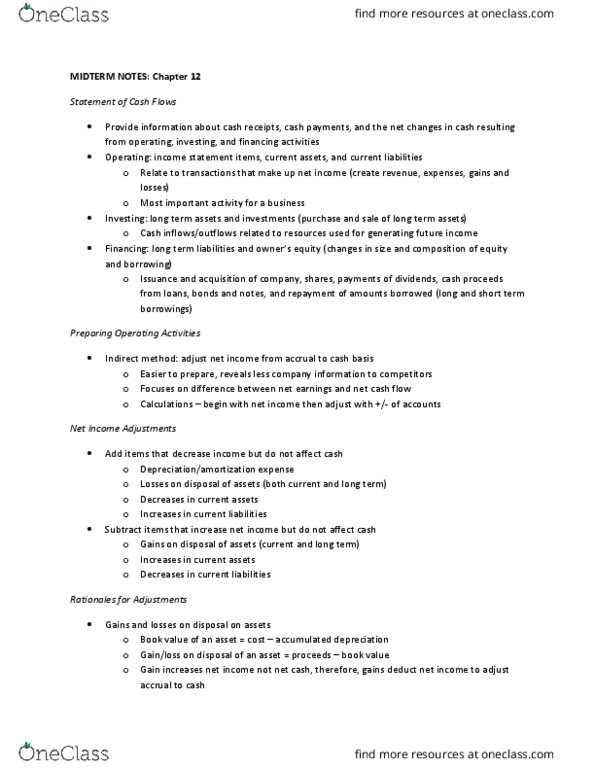

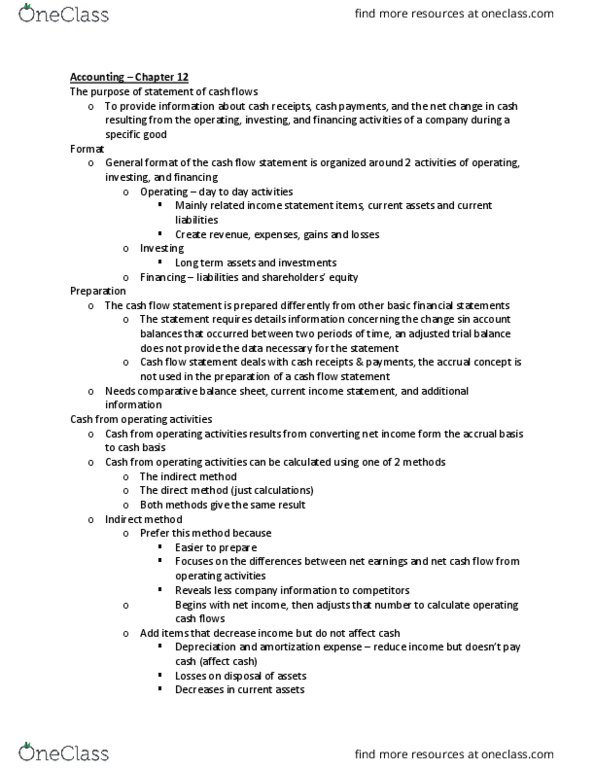

Different from other financial statements: not accrual basis. Sources: comparative balance sheet (previous and current year, current income statement, additional info. Results from converting net income from accrual to cash basis. Indirect: direct, net income, add depreciation, less gains, add losses, less increase of ca, add decrease of ca, less decrease of cl, add increase cl. Investing: add sales of lt assets, less purchases of lt assets, add sale of investments, less purchase of investments, add collections of notes receivable, less loans to others. Financing: add issuance of shares, less repurchase of shares, add borrowing, less payment of notes and bonds payable, less payment of dividends. Direct method: cash collections from customers, cash payments to suppliers, cash payments for operating expenses, cash payments for interest and income taxes. Note payable or stock to pay for lt assets. Primary way fraud and errors are prevented/detected/corrected. Management and board of directors implement plan of organization and system of procedures.