COMMERCE 2AB3 Chapter 6: Chapter Six — Decision-Making: Cost-Volume-Profit

10 Feb 2017

School

Department

Course

Professor

Document Summary

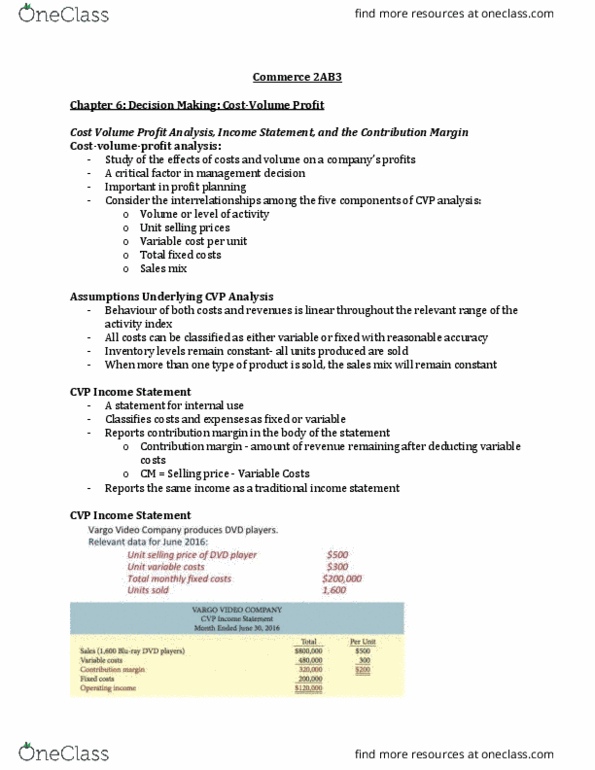

Break-even point: the level of activity at which total revenues equal total costs. Contribution margin: the amount of revenue remaining after deducting variable costs. Contribution margin per unit: the amount of revenue remaining per unit after deducting variable costs; calculated as the unit selling price minus the unit variable cost. Contribution margin ratio: the percentage of each dollar of sales that is available to contribute to operating income; calculated as the contribution margin per unit divided by the selling price. Cost structure: the proportion of xed costs versus variable costs that a company incurs. Cost-volume-pro t analysis: the study of the effects of changes in costs and volumes on a company"s pro ts. Cost-volume-pro t graph: a graph showing the relationship between costs, volumes, and pro ts. Cost-volume-pro t income statement: a statement for internal use that classi es costs and expense as xed or variable, and reports contribution margin in the body of the statement.