ACC 100 Chapter Notes - Chapter 3: Accounts Payable, Retained Earnings, Godaddy

24 Feb 2021

School

Department

Course

Professor

Document Summary

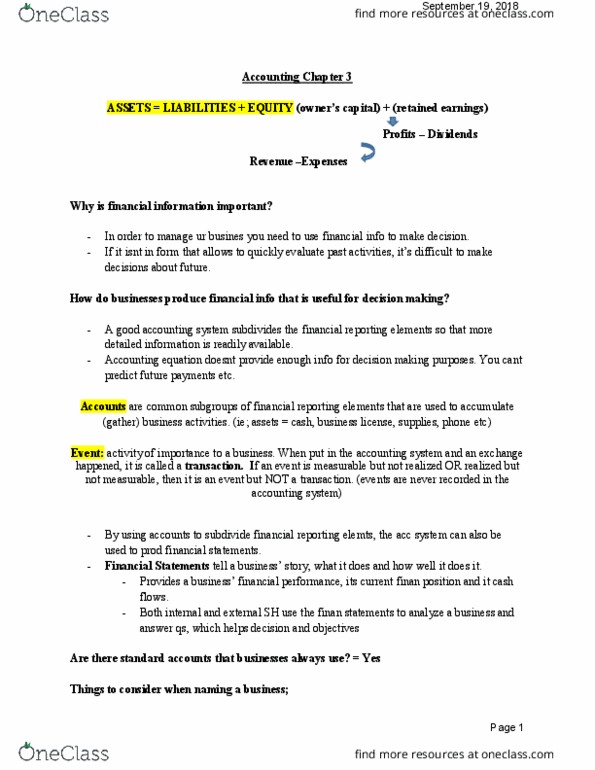

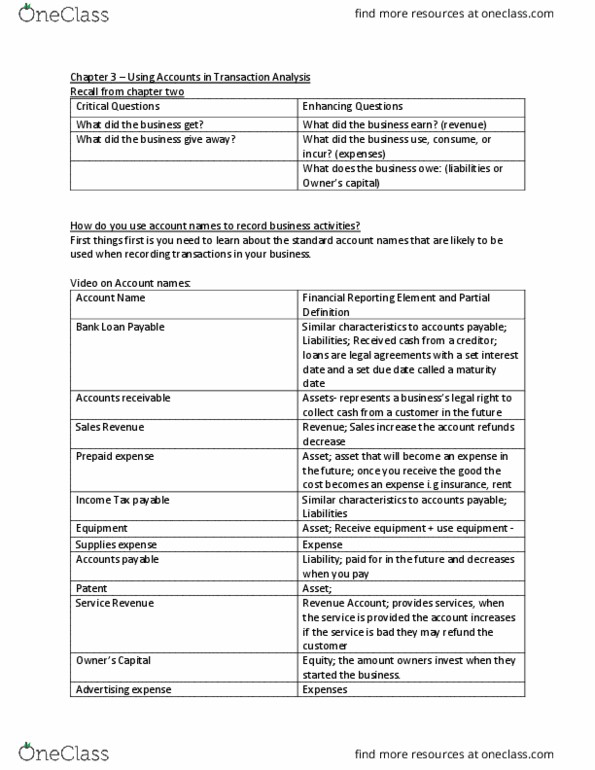

Using account names when recording transactions: summarize data in accounts, accounts financial reporting elements used to group information, ex. assets can be divided into cash and office supplies. Different accounts: asset, are always, owned or a legal right, have future benefit, due to a past transaction. Increase: : decrease: , assets accounts, cash, owned, has future benefit, due to past transaction, receive cash: , give away cash: , accounts receivable. Intangible assets: receive in the past, use in the future, legal right, receive: , use up: , examples, patents, licenses, copyrights, liabilities, are always, owed, settles with cash, goods, or services, due to a past transaction. Impact depends: basic vs. expanded accounting equation, examples, advertising, salary/wages, rent. Event: transaction = recorded, measurable, $ amount known, and, realized, exchange already occurred, event = not recorded, measurable, $ amount known, or, realized, exchange already occurred. The owner contributes 500 cash to start the business.