BUS 321 Chapter Notes - Chapter 16: Financial Instrument, Underlying, Financial Asset

6 Feb 2018

School

Department

Course

Professor

Document Summary

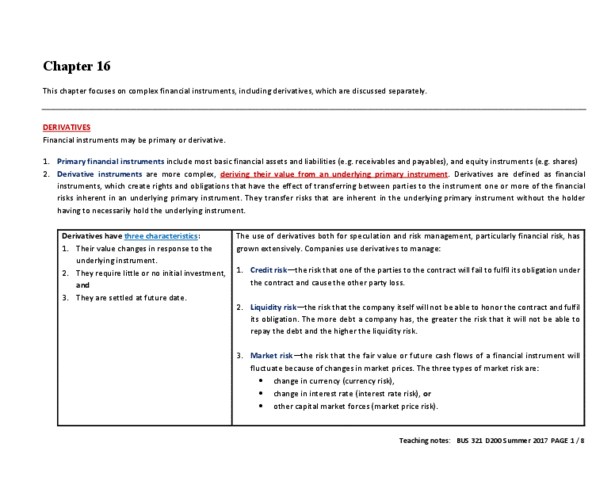

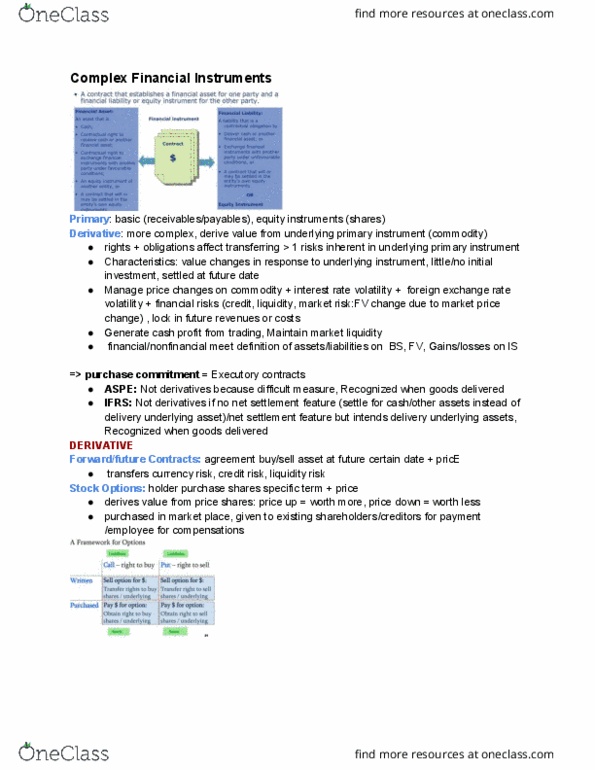

Financial instruments = contracts that create both a financial asset for one party and a financial liability or equity instrument for the other party. Primary financial instrument includes basic financial assets and financial liabilities and equity instruments. Derivative instrument = derive their value from an underlying asset; trade on exchange and over the counter market. Accounting standard define derivatives as financial instruments that create rights and obligations that have the effect of transferring, between parties to the instrument, one or more of the financial risks that are inherent in an underlying primary instrument . Derivatives have three characteristics: (1) their value changes in response to the underlying instruments (2) they require little or no initial investment (3) they are settled at future date. Derivatives are measured at fair value with gains and losses booked through net income. There are many layers of costs relating to the use of derivatives direct cost, indirect costs and other cost (opportunity cost)